2026 has been the year of the IPO — including the largest one in history, the SpaceX debut in June — and if the news left you wondering what actually happens when a company "goes public," this guide walks through the whole machine.

What Is an IPO? How Companies Go Public, Explained

An IPO is the first time a private company sells shares to the public. Here's why companies do it, how the process works step by step, and what the record-breaking SpaceX IPO of June 2026 taught about pricing, underwriting, and post-listing volatility.

11 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

In short: an IPO (initial public offering) is the first time a private company sells its shares to the general public and lists them on a stock exchange. The company raises money by selling new shares, early investors and employees gain a way to eventually sell theirs, and from that day on, anyone with a brokerage account can buy or sell the stock at a market price.

Understanding what an IPO is — and what the offer price, the underwriters, and the lock-up period actually do — turns some of the most exciting market news into something you can read critically instead of just watching numbers fly.

Educational note: This page is for learning purposes only and is not financial advice. Newly listed stocks can be exceptionally volatile, and past offerings do not predict future outcomes.

Who this is for

This explainer is for beginner investors who kept seeing IPO stories in 2026 — record raises, first-day surges, dramatic pullbacks — and want to understand the mechanics behind them. If you can follow a regular stock quote but aren't sure what "priced at $135," "lead underwriter," or "lock-up expiry" mean, this page is the missing vocabulary. No finance background needed.

Key benefits

The first benefit of understanding IPOs is reading market news accurately. Reports about an offering mix three different numbers — how much the company raised, what the pricing valued it at, and what the market capitalization became once trading started — and confusing them leads to wildly wrong conclusions. After this article, you'll keep them straight.

The second benefit is a realistic picture of risk. IPO coverage naturally spotlights debut-day surges; the weeks after, when early volatility cuts both ways, get less attention. Knowing the full lifecycle — including lock-up expirations months later — is what separates understanding from hype.

| If your goal is… | Focus on… | Practical next step |

|---|---|---|

| Understand what an IPO is | The definition and the why | Read the first three sections |

| Decode an IPO news story | Raise vs valuation vs market cap | Use the disambiguation table below |

| Understand who runs the process | Underwriting and pricing | See the underwriter section and fee example |

| See how it plays out in practice | The June 2026 case study | Follow the dated walk-through |

| Practice without risking money | Post-listing volatility | Track a new listing in a trading simulator |

Why do companies go public?

A private company's shares are hard to buy and hard to sell — ownership sits with founders, employees, and private investors. Going public changes that, and companies typically do it for a few reasons:

- Raising capital. Selling new shares brings in cash for expansion, research, debt repayment, or — in 2026's most prominent case — enormous infrastructure investment.

- Liquidity for early holders. Employees and early investors gain a public market where, after restrictions lapse, they can sell shares they may have held for a decade or more.

- Acquisition currency and profile. Public stock can be used to acquire other companies, and a listing raises a company's visibility with customers and partners.

The trade-offs are real, too: public companies must file detailed financial disclosures, answer to a broad shareholder base, and live with a stock price that reacts to every piece of news. That's why some large companies stay private for many years — and why a decision to finally list is itself news.

The IPO process, step by step

1. Filing. The company registers with the SEC, publishing a prospectus (the S-1) that discloses its financials, risks, and plans. This is the first time outsiders see audited numbers. In the 2026 record offering, a confidential draft preceded a public S-1 filed on May 20.

2. Roadshow. Company management and its banks present to institutional investors, gauging demand. Traditionally this is when a price range gets tested and refined.

3. Pricing. The night before trading, the offer price is set and initial buyers get their allocations at that price. This is the only price the company receives — everything after is investors trading with each other.

4. Listing day. The stock opens on an exchange under its ticker. The opening price is set by matching buy and sell orders — it can land above or below the offer price, sometimes dramatically.

5. Lock-up period. For a period after the debut — commonly around 180 days — insiders and early investors are typically restricted from selling. When lock-ups expire, the supply of tradable shares can rise sharply, which is why the date is watched.

Underwriting: who runs an IPO

Underwriters are the investment banks that manage the offering — they help prepare the filings, run the roadshow, build the order book, set the price, allocate shares, and support early trading. Large IPOs use a syndicate of several banks with one "lead" bookrunner.

Underwriting is a business, and 2026 provided an unusually clear illustration. The record June offering paid its syndicate fees reported at under 0.75% of the deal — roughly $500 million — versus the 4–7% typical for ordinary IPOs; the deal's sheer size meant even a cut-rate percentage was an enormous fee pool.

| Fee type | Typical share of deal | 2026 record offering |

|---|---|---|

| Syndicate underwriting fee | About 4–7% | Under 0.75% (~$500 million) |

| What you get for it | Filing support, roadshow, pricing, allocation | Same roles — at mega-deal scale |

A month later, when Q2 bank earnings arrived, the lead underwriter reported investment banking fees up 55% year over year, a jump news coverage attributed in part to that single offering. For a beginner, the takeaway is simple: the banks around an IPO are paid participants with a defined role, not neutral observers.

One more underwriting mechanic worth knowing: the overallotment (or "greenshoe") option. Underwriters typically receive the right to buy an additional block of shares at the offer price if demand is strong. In the 2026 case, the base offering was 555.6 million shares at $135 — about $75 billion — and the underwriters' option covered a further 83.33 million shares, which strong demand led them to exercise, lifting the total raise to roughly $86 billion.

How are IPOs priced?

In the standard process, pricing emerges from bookbuilding: the banks collect indications of interest during the roadshow, publish and sometimes revise a price range, and set the final offer price where demand supports it.

The June 2026 offering was a teachable exception: the company set a fixed price of $135 per share before the roadshow even began, skipping the customary price-range discovery — a take-it-or-leave-it approach that only a company with overwhelming demand could attempt. At that price, the offering implied a valuation of about $1.77 trillion — the largest IPO pricing in history.

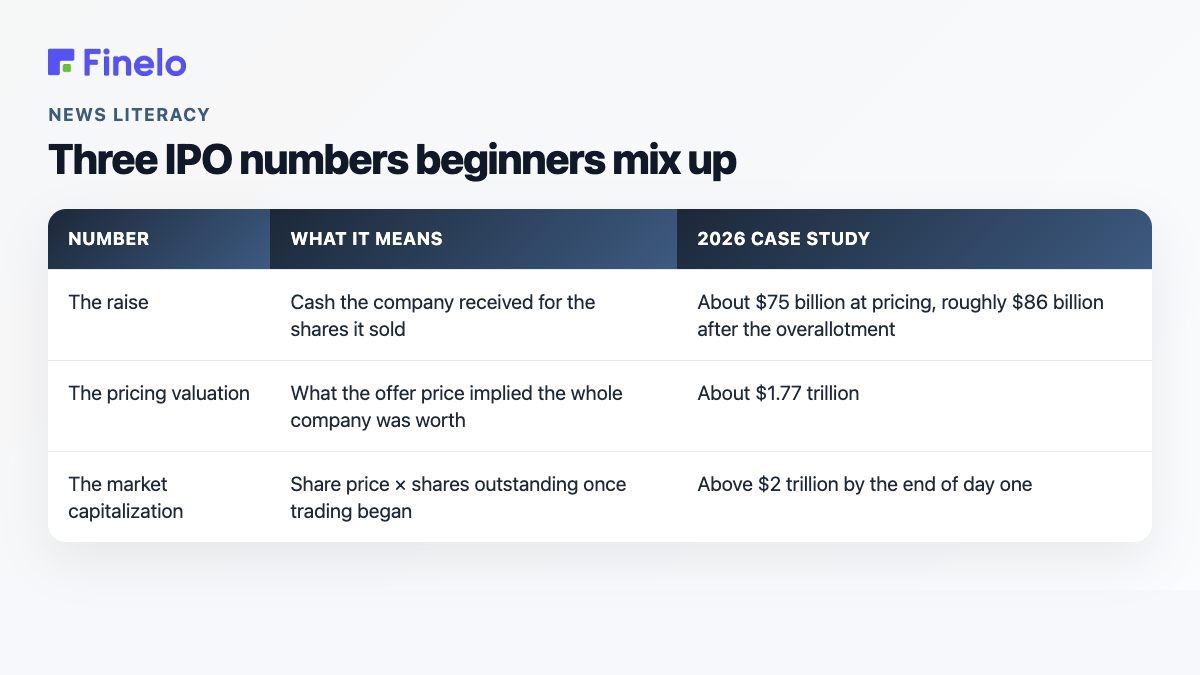

Here is where beginners should slow down, because three different numbers now exist:

| Number | What it means | 2026 case study |

|---|---|---|

| The raise | Cash the company received for the shares it sold | About $75 billion at pricing, roughly $86 billion after the overallotment |

| The pricing valuation | What the offer price implied the whole company was worth | About $1.77 trillion |

| The market capitalization | Share price × shares outstanding once trading began | Above $2 trillion by the end of day one |

News reports flip between these constantly. Keeping them separate is half of IPO literacy.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Case study: the SpaceX IPO, June 2026

The largest IPO in history compressed the entire lifecycle into one dramatic month — all figures below are historical, not predictive.

SpaceX priced at $135 on June 11 and debuted on the Nasdaq on June 12 under the ticker SPCX. The stock opened at $150 — about 11% above the offer price — and closed its first day roughly 19% up, pushing its market capitalization past $2 trillion.

The following weeks showed the other half of the story. The shares kept climbing at first, reaching an intraday peak of $225.64 on June 16 — then fell in consecutive sessions to around $153 by late June. By mid-July the stock had given back roughly 38% from that peak and was trading close to the original $135 offer price. A month after the debut, investors who received shares at the offer price were sitting on a paper gain of under 1% — while anyone who bought near the peak was deep underwater. Same company, radically different outcomes, decided almost entirely by entry point.

Notice how much of the process the case demonstrates: the S-1 disclosure, the skipped price range, the syndicate and its fees, the exercised overallotment, the first-day pop, and the volatility that followed. One offering, the whole textbook.

After the IPO: what typically happens next

The first-day pop — or drop. When an offer price is set below what public traders will pay, the stock "pops." Historically, pops have been common in hot markets — and so have debut-day declines in cold ones. A pop is a pricing outcome, not a reward for buying; by the time a stock is popping, retail buyers are paying the popped price.

Early volatility. Newly listed stocks have short trading histories, small floats, and intense attention — swings in both directions have often been far larger than for established stocks, as the 2026 case showed within a single week.

Lock-up expiry. Months after the debut, insider selling restrictions lapse. The tradable share supply can jump, and the date is often marked on investor calendars.

Debt markets keep score too. Going public typically broadens a company's access to capital markets overall — including bonds. In the 2026 case, the company issued about $25 billion of bonds around its listing, and within a month bond investors had repriced them: the extra yield demanded over comparable US Treasuries widened from about 1.75 to about 2.3 percentage points. The lesson for beginners: a public company is scored by two markets at once — stock investors price potential upside, while bond investors price repayment risk — and the two verdicts do not always move together.

Index inclusion. Major indexes have rules for adding new listings; inclusion can matter because index funds then buy the stock automatically. The 2026 case drew attention here too — the exchange changed its rules to admit very large new listings to its flagship index just 15 trading days after an IPO.

IPO vs direct listing

An IPO is not the only path to going public.

| IPO | Direct listing | |

|---|---|---|

| New shares sold? | Yes — company raises cash | Typically no — existing holders sell |

| Underwriters | Full syndicate, sets price, allocates | Advisory role only; no allocation |

| Offer price | Set the night before trading | No offer price; opening auction discovers price |

| Lock-up | Customary (~180 days) | Often none |

| Typical users | Companies needing capital | Well-known companies with cash, wanting liquidity |

A third route — merging with a SPAC (special-purpose acquisition company) — had its boom years earlier in the decade; it's worth recognizing the term, though the mechanics differ substantially.

Common mistakes beginners make

Chasing the pop. Buying a stock because it surged on debut day means paying the surge. The 2026 case's slide from its June 16 peak is a reminder that early enthusiasm can retrace quickly.

Confusing the three numbers. "$86 billion," "$1.77 trillion," and "$2 trillion" described the same offering — raise, pricing valuation, and market cap. Mixing them up produces nonsense conclusions.

Ignoring the lock-up calendar. Evaluating a young stock without knowing when insider restrictions expire misses a known, scheduled change in share supply.

Treating the prospectus as fine print. The S-1 is where a company discloses, under legal obligation, exactly what could go wrong. It is the single most information-dense document a beginner can practice reading.

Practice reading IPOs — without risking money

New listings are the market's best live classroom in price discovery. Pick a recently listed stock, and for four weeks track it in a trading simulator with virtual funds: note the offer price, where it opened, how it traded against market news, and what the prospectus flagged as risks. The goal is not to catch the next debut — it's to watch how a price gets discovered when no trading history exists.

If you're new to practice accounts, start with What Is Paper Trading? A Beginner's Guide. For a broader market-literacy companion, see WTI vs Brent Crude — another 2026 news story turned into a lasting explainer.

Next steps

If you are learning what an IPO is, start as an observer, not a participant. Read one real S-1 summary, follow one new listing's first month, and keep the three numbers — raise, valuation, market cap — separate in your notes. That habit alone puts you ahead of most casual readers of market news.

For guided learning, visit Finelo or open the Finelo app. To evaluate user experiences and trust signals before signing up, read Finelo reviews. For product or account questions, use the official support resources at support.finelo.com.

This article is for educational purposes only and does not constitute financial advice, an investment recommendation, or a prediction of any stock's future performance. Newly listed stocks involve significant risk. Always do your own research.

Frequently asked questions

What does IPO stand for?

IPO stands for initial public offering — the first sale of a company's shares to the general public, accompanied by a listing on a stock exchange such as the Nasdaq or NYSE.

Why do companies go public?

Mainly to raise capital by selling new shares, to give early investors and employees a liquid market for their holdings, and to gain acquisition currency and public profile. The trade-off is mandatory disclosure, shareholder accountability, and constant market scrutiny.

How is an IPO priced?

Usually through bookbuilding: underwriters gauge institutional demand during a roadshow, publish a price range, and set the final offer price the night before trading. Exceptions exist — the record June 2026 offering set a fixed price before its roadshow, an unusual approach enabled by overwhelming demand.

What is an underwriter in an IPO?

An investment bank (usually a syndicate of several) that manages the offering: preparing filings, running the roadshow, building the order book, setting the price, and allocating shares. Underwriters earn fees for this — historically around 4–7% of typical deals, though very large offerings have negotiated far lower percentages.

What is the IPO lock-up period?

A window after the debut — commonly about 180 days — during which insiders and early investors are restricted from selling shares. When it expires, the supply of tradable shares can increase significantly, which is why the date is watched.

What happens to a stock after the IPO?

It trades like any listed stock, but with traits that have historically amplified volatility: a short track record, a limited float, and heavy attention. First-day pops and subsequent pullbacks have both been common; the June 2026 offering rose 19% on debut, peaked days later, and by mid-July had given back roughly 38% from that peak.

What is the difference between an IPO and a direct listing?

In an IPO the company sells new shares at an underwriter-set offer price and raises cash; in a direct listing existing holders sell shares through an opening auction with no offer price, no allocation, and typically no raise. Companies that need capital choose IPOs; well-funded companies seeking liquidity have sometimes chosen direct listings.

IPOStocksMarket BasicsBeginner

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.