Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive is a price change, while inflation describes a wider movement across an economy. The U.S. Bureau of Labor Statistics defines inflation as an overall upward price movement and notes that different indexes measure different aspects of it.

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

5 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

Understanding inflation helps households interpret changes in everyday costs, compare income growth with rising prices, and make calmer financial decisions. It also helps businesses plan their prices, wages, inventory, and borrowing.

How Inflation Works and How It Is Measured

Inflation is usually expressed as a rate of change over a period. A price index starts with a group of goods and services, tracks how their combined price changes, and converts that movement into an inflation rate. Because no single basket captures every part of the economy, the BLS uses various indexes to measure different aspects of inflation.

Imagine a simplified basket containing groceries, rent, transportation, and personal services. If its total cost rises from one period to the next, the index rises. The size of that change indicates the inflation rate for that basket. Your personal experience may still feel different because your spending mix is unlikely to match the index exactly. A commuter, a renter, and a retiree can face different pressures even while living under the same reported inflation rate.

It is also useful to separate the price level from the inflation rate. If inflation slows, prices are generally rising more slowly; that does not necessarily mean they have returned to earlier levels. Falling prices across the economy would be a different condition.

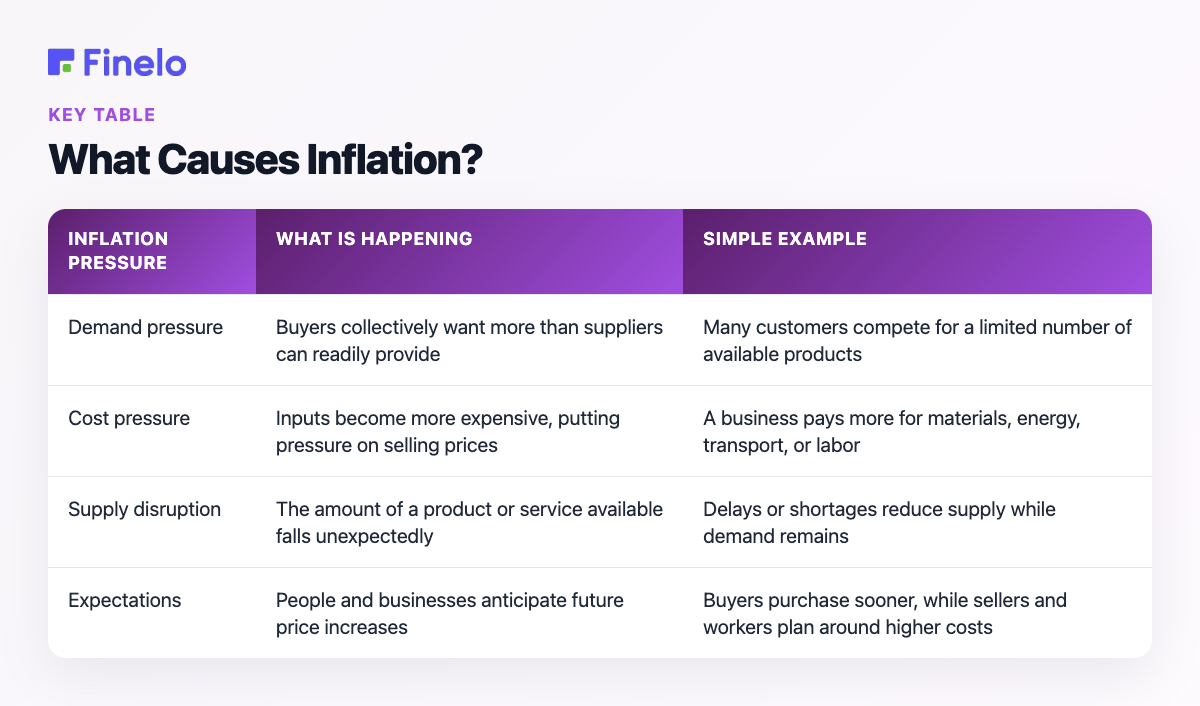

What Causes Inflation?

Inflation rarely has only one cause. It can emerge when spending grows faster than the economy’s ability to supply goods and services, when businesses face higher production costs, or when expectations begin influencing wages and prices.

| Inflation pressure | What is happening | Simple example |

|---|---|---|

| Demand pressure | Buyers collectively want more than suppliers can readily provide | Many customers compete for a limited number of available products |

| Cost pressure | Inputs become more expensive, putting pressure on selling prices | A business pays more for materials, energy, transport, or labor |

| Supply disruption | The amount of a product or service available falls unexpectedly | Delays or shortages reduce supply while demand remains |

| Expectations | People and businesses anticipate future price increases | Buyers purchase sooner, while sellers and workers plan around higher costs |

These forces can overlap. A supply problem may raise costs, while strong demand makes it easier for businesses to pass those costs on. Expectations can then prolong the process if households, workers, and companies assume rapid increases will continue.

Money and credit conditions can also influence demand. Easier access to spending power may support more purchases, while tighter conditions can cool them. The effect is not instant: households and businesses need time to change borrowing, hiring, pricing, and investment decisions.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

How Inflation Affects Purchasing Power and Behavior

The clearest personal effect of inflation is reduced purchasing power. If income stays unchanged while a broad range of prices rises, a budget covers fewer goods and services. People may respond by switching brands, postponing optional purchases, reducing quantities, or directing more income toward essentials.

Inflation does not affect everyone equally. The impact depends on what a person buys, how quickly their income adjusts, how much cash they hold, and whether their debts or payments have fixed or changing terms. Businesses face similar differences: a company that can adjust prices may cope differently from one locked into long contracts or exposed to volatile input costs.

Inflation can also change behavior before a purchase occurs. When people expect prices to rise, they may buy sooner or stock up. When uncertainty is high, they may become more cautious, compare prices more often, or delay long-term commitments. These reactions matter because collective behavior can reinforce demand, shortages, or uncertainty.

For savers, the important distinction is between a balance’s stated growth and its purchasing power. A larger number in an account does not automatically mean a person can buy more with it. For borrowers, inflation can interact with interest rates and repayment terms, so the full contract matters more than a general rule.

Learning From Historical Inflation

Historical inflation episodes are best understood as chains of events rather than isolated numbers. Severe cases—including periods commonly described as hyperinflation—have involved a breakdown in the usefulness of money for routine pricing and planning. But the triggers, policy responses, and consequences vary, so comparisons require consistent data and context.

When reviewing any country or decade, ask:

- Was the pressure driven mainly by demand, costs, disrupted supply, policy choices, lost confidence, or several factors together?

- Which price index and time period are being used?

- Did wages and household income adjust at the same pace as prices?

- Were shortages or currency changes part of the episode?

- Which actions slowed inflation, and what tradeoffs followed?

This framework is more informative than comparing published rates alone. A country table can look precise while being misleading if the figures use different indexes, dates, or methods. Use a single official dataset before making direct international or decade-long comparisons.

How Individuals Can Respond to Inflation

No single asset, purchase, or tactic provides guaranteed protection from inflation. A practical response starts with the household decisions you can control:

- Recalculate essential monthly spending using current bills rather than old estimates.

- Separate recurring needs from flexible or postponable purchases.

- Compare income growth and savings growth with changes in your actual cost of living.

- Review interest rates, fees, maturity dates, and access restrictions before changing savings or borrowing products.

- Avoid panic buying solely because prices might rise.

- Keep investment decisions diversified, risk-aware, and aligned with your time horizon rather than relying on a single inflation forecast.

A simple decision framework is to identify the pressure first. If essentials are squeezing cash flow, focus on the budget and emergency reserves. If idle cash is losing purchasing power over a long horizon, learn how risk, return, liquidity, and diversification interact before choosing investments. If debt payments are the concern, review the exact loan terms. If the issue is uncertainty, gather current official data before acting.

This article is educational, not personalized financial advice. Costs, risks, taxes, and suitability depend on individual circumstances. Readers who want to build their financial vocabulary can continue learning through Finelo’s financial education platform.

Frequently asked questions

What is the simplest definition of inflation?

Inflation is a broad rise in prices over time that reduces what a unit of money can buy. It refers to an economy-wide movement, not merely a higher price for one item.

What is the difference between inflation and the cost of living?

Inflation measures broad price change through an index. Cost of living is more personal: it reflects what a particular household needs to spend to maintain its usual standard of living.

Does lower inflation mean prices are falling?

Not necessarily. Lower inflation usually means prices are increasing more slowly. A widespread decline in prices is a separate condition.

What should I do after checking the inflation rate?

Compare the published figure with changes in your own essential expenses, income, savings, and debt costs. Then prioritize the specific area under pressure instead of making a broad financial move based on one number.

Financial LiteracyBeginnerEconomicsPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What is GDP? Understanding Gross Domestic Product

GDP, or gross domestic product, is the total value of goods and services produced within a country during a given period. In plain language, it is a broad scorecard for the size and direction of an economy. The Federal…

Finelo Team