Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand and jobs become harder to find. That combination can squeeze household budgets, weaken business activity, and leave policymakers with difficult trade-offs. Fidelity’s definition of stagflation highlights the same three-part pattern: inflation, stagnant growth, and unemployment.

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

8 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

Understanding stagflation is useful for anyone trying to interpret economic news or make calmer financial decisions. It is not a prediction that a crisis is coming. It is a framework for recognizing what makes this environment different from ordinary inflation or a typical economic slowdown.

How stagflation works

The three elements of stagflation reinforce one another:

- Inflation raises the cost of goods and services.

- Stagnant growth means businesses and the economy are producing little additional value.

- High unemployment reduces income security and can weaken consumer demand.

Consider a simplified example. A sharp increase in a widely used input, such as energy or transportation, raises costs for many businesses. Companies may respond by increasing prices, reducing production, delaying expansion, or limiting hiring. Consumers then face more expensive essentials at the same time that wage growth and job opportunities may be weak.

That is what makes stagflation especially painful. In a strong economy, households may be better able to absorb rising prices because employment and incomes are improving. During a conventional slowdown, inflationary pressure may ease as demand falls. Stagflation combines the difficult sides of both conditions.

Stagflation compared with inflation and recession

These terms overlap, but they are not interchangeable.

| Economic condition | Prices | Growth | Employment |

|---|---|---|---|

| Inflation | Rising | May be strong or weak | May be strong or weak |

| Recession or downturn | Often under less upward pressure | Contracting or weak | Usually weakening |

| Stagflation | Rising significantly | Stagnant or weak | High unemployment or a weakening labor market |

Inflation alone does not equal stagflation. Prices can rise while the economy is growing and employment remains healthy. Likewise, weak growth alone is not stagflation if inflation is low. The label becomes relevant when persistent price pressure and economic stagnation appear together.

What causes stagflation?

There is no single cause that explains every possible episode. Stagflation can emerge when a major disruption reduces the economy’s capacity to supply goods and services, when costs rise across many industries, or when policy choices aggravate an already difficult imbalance.

Supply shocks

A supply shock makes an important product or input more expensive or less available. If many industries depend on that input, the disruption can spread through the economy.

Imagine that fuel and freight costs rise abruptly. A food producer pays more to operate machinery, package goods, and deliver products to stores. Retailers then face higher wholesale and transportation costs. Prices may rise even if consumers are not buying more. Meanwhile, companies may cut output or hiring because producing each unit has become less profitable.

Supply shocks differ from demand-driven inflation. When demand is the main force, prices rise because buyers are competing for available goods and services. With a negative supply shock, prices can rise even as production and demand weaken.

Broad increases in business costs

Stagflation risk can also grow when businesses face several cost pressures at once. More expensive materials, financing, labor, logistics, or regulatory compliance can limit production and investment. Businesses may pass some costs to customers, absorb them through lower margins, or reduce activity.

For example, a manufacturer that cannot obtain affordable components may raise prices while shelving a planned expansion. The result is less growth alongside continued inflation.

Policy mistakes and delayed responses

Economic policy involves timing and trade-offs. Measures that support demand may help employment and growth, but they can also add price pressure when supply is constrained. Policies designed to suppress inflation may weaken borrowing, spending, and hiring.

The risk does not come from one policy tool in isolation. It comes from a mismatch between the problem and the response. If authorities treat a supply shortage as though it were only a demand problem, the intervention may fail to repair the underlying constraint.

Expectations and feedback loops

Inflation expectations can affect behavior. Workers may seek higher pay to keep up with living costs, businesses may raise prices in anticipation of future expenses, and consumers may change when or what they buy. These reactions can make inflation harder to reduce.

At the same time, uncertainty may discourage investment and hiring. A business that cannot estimate future costs or customer demand may postpone expansion. That hesitation can deepen stagnation even if it is a rational decision for the individual company.

Effects on the economy and personal finances

Stagflation can influence policymakers, businesses, investors, and households, which is one reason the condition attracts attention even though it does not occur often in the US economy, according to Fidelity’s overview.

Household purchasing power

When prices rise faster than income, the same paycheck buys less. Essentials such as food, housing, transportation, and utilities may take a larger share of the budget. A household that previously had room for saving or discretionary purchases may need to redirect money toward basic expenses.

The effect is not equal for everyone. Households that spend a high proportion of income on necessities generally have less flexibility. Someone with unstable employment may also face the combined pressure of higher expenses and uncertain earnings.

Employment and wages

Weak growth can make employers cautious about hiring, pay increases, and expansion. Some businesses may reduce hours or staffing to control costs. Workers can therefore face a difficult combination: their living expenses rise while their bargaining power or job security weakens.

For example, an employee may receive a modest nominal pay increase but still lose purchasing power if everyday costs rise faster. The number on the paycheck is higher, yet the household’s practical standard of living declines.

Borrowing and debt

Efforts to control inflation can make borrowing more expensive. Variable-rate debt may become harder to manage, while new loans can require larger payments. Higher financing costs may also discourage businesses from investing in equipment, property, or additional employees.

For individuals, the important question is not simply whether rates are “high.” It is whether required debt payments leave enough room for essentials, emergency savings, and other priorities.

Saving and investing

Inflation reduces the future purchasing power of money that does not grow at a comparable pace. Yet weak growth and uncertainty can also create market volatility, so there is no single asset or strategy that is guaranteed to protect a portfolio.

Fidelity notes that investors have historically explored certain assets and strategies during stagflation, but historical behavior is not a promise of future results. Any investment decision still needs to fit the investor’s goals, time horizon, costs, and capacity for loss.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Why stagflation is difficult for policymakers

The usual responses to inflation and economic weakness can pull in opposite directions.

To restrain inflation, policymakers may try to cool borrowing and spending. That can reduce price pressure, but it may also slow business activity and weaken employment. To stimulate growth, policymakers may support demand or make borrowing easier. That may help output and jobs, but it can also sustain inflation if the economy still cannot supply enough goods and services.

Here is the core dilemma:

| Policy priority | Possible response | Main trade-off |

|---|---|---|

| Reduce inflation | Restrain demand and credit | Growth and employment may weaken |

| Support growth | Encourage spending and investment | Inflation may remain elevated |

| Repair supply constraints | Improve productive capacity and availability | Changes may take time to affect prices |

| Restore confidence | Communicate a consistent direction | Credibility can be difficult to rebuild |

There is rarely a quick, painless solution. The appropriate response depends on what caused the imbalance, how persistent it is, and whether inflation expectations are becoming embedded in everyday decisions.

How to prepare your finances

No household can control the wider economy, and no checklist can eliminate financial risk. A practical response is to improve flexibility rather than make a dramatic bet on one economic forecast.

1. Stress-test the monthly budget

Review how the budget would change if essentials became more expensive or income temporarily fell. Separate expenses into:

- essentials that must be paid;

- flexible costs that can be reduced;

- irregular bills that should be planned for;

- debt payments and their interest-rate terms.

The goal is to identify pressure points before they become emergencies.

2. Build an appropriate cash buffer

Emergency savings can reduce the need to borrow or sell investments after an income disruption. The suitable amount differs by household, especially when employment stability, dependents, insurance coverage, and fixed expenses vary.

3. Review expensive and variable-rate debt

List balances, rates, minimum payments, and whether the rate can change. Prioritizing costly debt may improve resilience, but refinancing or repayment choices should be evaluated carefully for fees, terms, and effects on liquidity.

4. Protect earning capacity

During weak growth, financial resilience is partly about income. Maintaining relevant skills, professional relationships, and an updated record of experience may help if the labor market becomes less favorable. A second source of income can add flexibility, but it should be assessed realistically for time, expenses, taxes, and reliability.

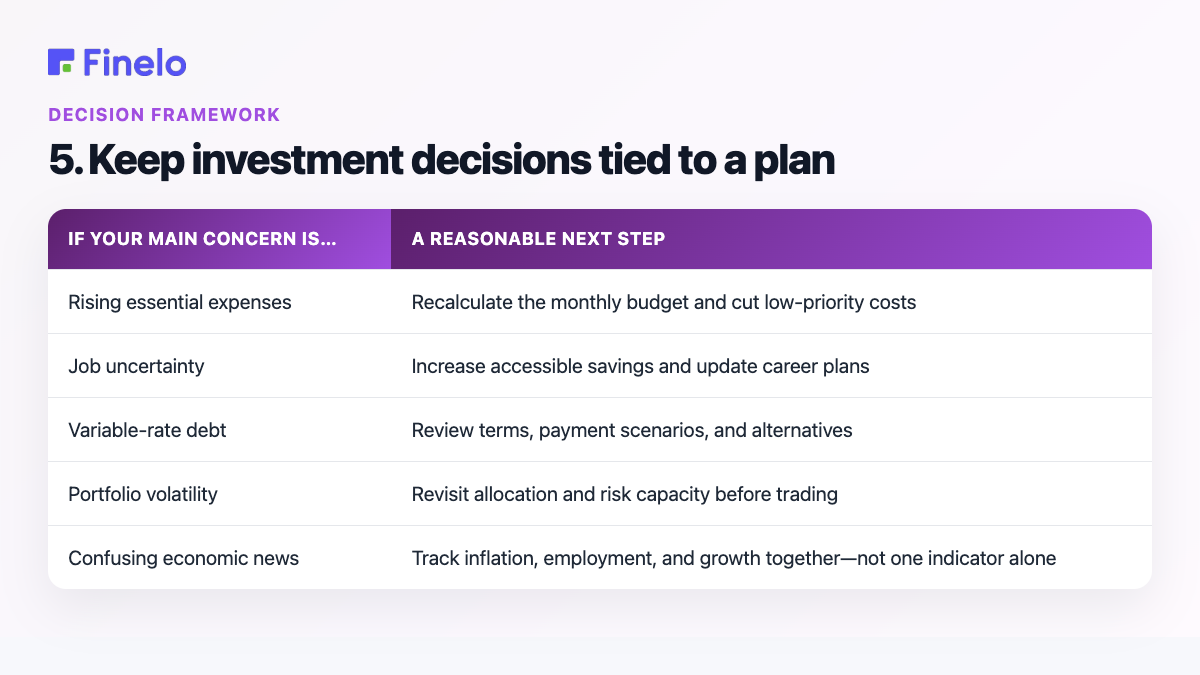

5. Keep investment decisions tied to a plan

Avoid rebuilding an entire portfolio around a frightening news report. Review diversification, risk tolerance, time horizon, and near-term cash needs. An asset that performed well in one inflationary period may behave differently in another.

| If your main concern is… | A reasonable next step |

|---|---|

| Rising essential expenses | Recalculate the monthly budget and cut low-priority costs |

| Job uncertainty | Increase accessible savings and update career plans |

| Variable-rate debt | Review terms, payment scenarios, and alternatives |

| Portfolio volatility | Revisit allocation and risk capacity before trading |

| Confusing economic news | Track inflation, employment, and growth together—not one indicator alone |

These are educational principles, not personalized financial advice. Verify costs, risks, tax effects, and suitability before changing debt or investments.

The bottom line

The best short answer to “What is stagflation?” is: high inflation, stagnant economic growth, and high unemployment happening at the same time. Its causes can include supply disruptions, widespread cost increases, policy errors, and feedback loops in expectations. Its effects can reach household budgets, jobs, borrowing, business investment, and financial markets.

The most useful response is not to predict the economy with certainty. Build room in your budget, understand your debts, protect your earning capacity, and keep investment choices aligned with a considered plan. If you want to strengthen your investing knowledge before making decisions, explore Finelo’s financial education resources.

Frequently asked questions

Is stagflation the same as a recession?

No. A recession describes a broad economic downturn. Stagflation specifically combines weak or stagnant growth with high inflation and high unemployment. An economy can experience a downturn without significant inflation, and it can experience inflation without stagnation.

What are the first signs of stagflation?

There is no single decisive signal. Analysts generally look for a sustained combination of elevated inflation, weak output or growth, and deterioration in employment. One disappointing report is not enough to establish the pattern.

Can interest-rate changes fix stagflation?

Interest-rate policy can influence inflation and demand, but it may not directly solve a supply constraint. Tighter conditions can reduce price pressure while also weakening growth; easier conditions can support activity while risking more inflation. That conflict is central to the stagflation problem.

What should individuals do first?

Start with factors you can control: understand essential spending, maintain accessible savings, review debt terms, and avoid impulsive investment decisions. Then monitor whether changes in prices, employment, or income materially affect your own plan.

Financial LiteracyBeginnerEconomicsPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team

Financial Literacy

What is GDP? Understanding Gross Domestic Product

GDP, or gross domestic product, is the total value of goods and services produced within a country during a given period. In plain language, it is a broad scorecard for the size and direction of an economy. The Federal…

Finelo Team