Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day operations.

Working Capital: What It Tells Investors About Liquidity

Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day…

8 min read

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Want to learn more?

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

A positive figure usually provides more room to pay suppliers, cover payroll, replace inventory, and handle timing gaps between spending and receiving cash. A negative figure calls for closer examination, but it is not automatically proof that a business is failing. The meaning depends on the business model, how quickly assets turn into cash, when bills fall due, and how the measure changes over several reporting periods.

What counts as working capital?

Working capital brings together two balance-sheet categories:

- Current assets: resources expected to be used, sold, collected, or converted into cash in the short term. Common examples include cash, accounts receivable, inventory, and prepaid operating costs.

- Current liabilities: obligations expected to be settled in the short term. Common examples include accounts payable, accrued expenses, short-term borrowings, taxes due, and the current portion of longer-term obligations.

Not every current asset is equally useful for paying bills. Cash is immediately available, while receivables must be collected and inventory must usually be sold first. A company can therefore report positive working capital and still feel cash pressure if much of that value is tied up in slow-moving inventory or overdue customer invoices.

The same distinction applies to liabilities. A bill due tomorrow creates a different constraint from one due several months later. That is why the summary figure should be read alongside the timing and quality of its components.

How to calculate working capital

The standard formula is:

Working capital = current assets − current liabilities

This definition is also shown in a company filing available through the U.S. Securities and Exchange Commission, which states that working capital is total current assets less total current liabilities.

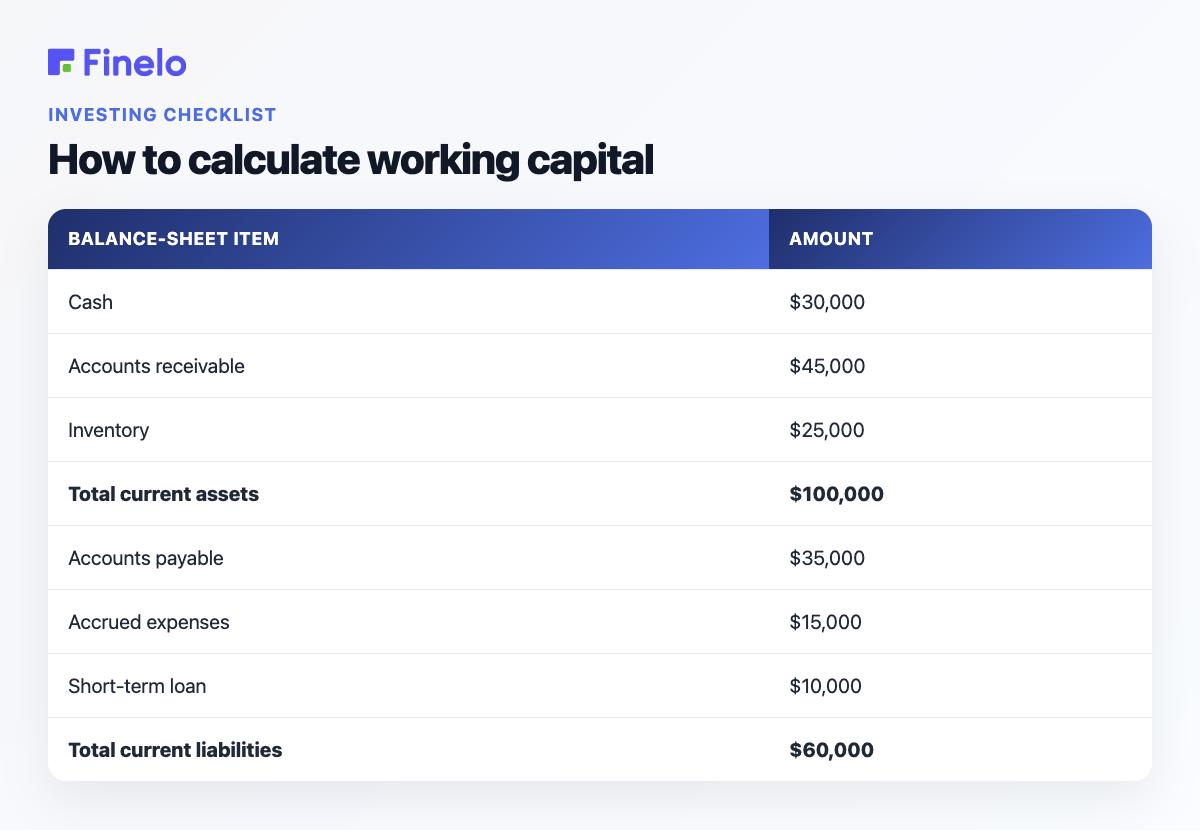

Suppose a business reports:

| Balance-sheet item | Amount |

|---|---|

| Cash | $30,000 |

| Accounts receivable | $45,000 |

| Inventory | $25,000 |

| Total current assets | $100,000 |

| Accounts payable | $35,000 |

| Accrued expenses | $15,000 |

| Short-term loan | $10,000 |

| Total current liabilities | $60,000 |

Its working capital is:

$100,000 − $60,000 = $40,000

This means current assets exceed current liabilities by $40,000 at that point in time. It does not mean the company has $40,000 sitting in a bank account. Some of the amount may be inventory or money customers have not yet paid.

Working capital calculator

Use this simple calculation with figures from the same reporting date:

- Add all current assets: $_____

- Add all current liabilities: $_____

- Subtract liabilities from assets: $_____

- Review what makes up the result, especially cash, receivables, inventory, and bills due soon.

Using figures from different dates can create a misleading result. It is also useful to repeat the calculation over several reporting periods rather than relying on one snapshot.

Working capital versus the current ratio

Working capital is a dollar amount. The current ratio expresses a similar relationship as a multiple:

Current ratio = current assets ÷ current liabilities

Using the example above, the current ratio is:

$100,000 ÷ $60,000 = 1.67

The two measures answer different questions. Working capital shows the absolute surplus or shortfall. The current ratio makes it easier to compare periods or businesses of different sizes, although differences in business models still matter.

Neither measure should be interpreted alone. A large company may need a much larger dollar cushion than a small company. A high ratio can also reflect excess inventory or uncollected invoices rather than abundant usable cash.

Why Working Capital Matters to Investors

Profit and liquidity are related, but they are not the same. A sale may create revenue before the customer pays. Inventory may require cash before it produces a sale. Meanwhile, wages, rent, taxes, and supplier invoices continue to come due.

Working capital helps reveal how comfortably a business can navigate those timing differences. Effective management can support several practical goals:

- paying short-term obligations when due;

- avoiding unnecessary disruption to purchasing or production;

- maintaining enough inventory without trapping excessive cash;

- setting customer payment terms that fit the company’s own obligations;

- planning for seasonal peaks, slower periods, or unexpected costs; and

- deciding whether growth can be funded internally or may require financing.

Growth can actually increase working capital pressure. A company may need to buy more materials, carry more stock, or hire staff before it collects cash from new sales. Revenue growth is therefore not a substitute for cash generation. For investors, a widening gap between profit and operating cash flow may be a reason to inspect receivables, inventory, and payables more closely.

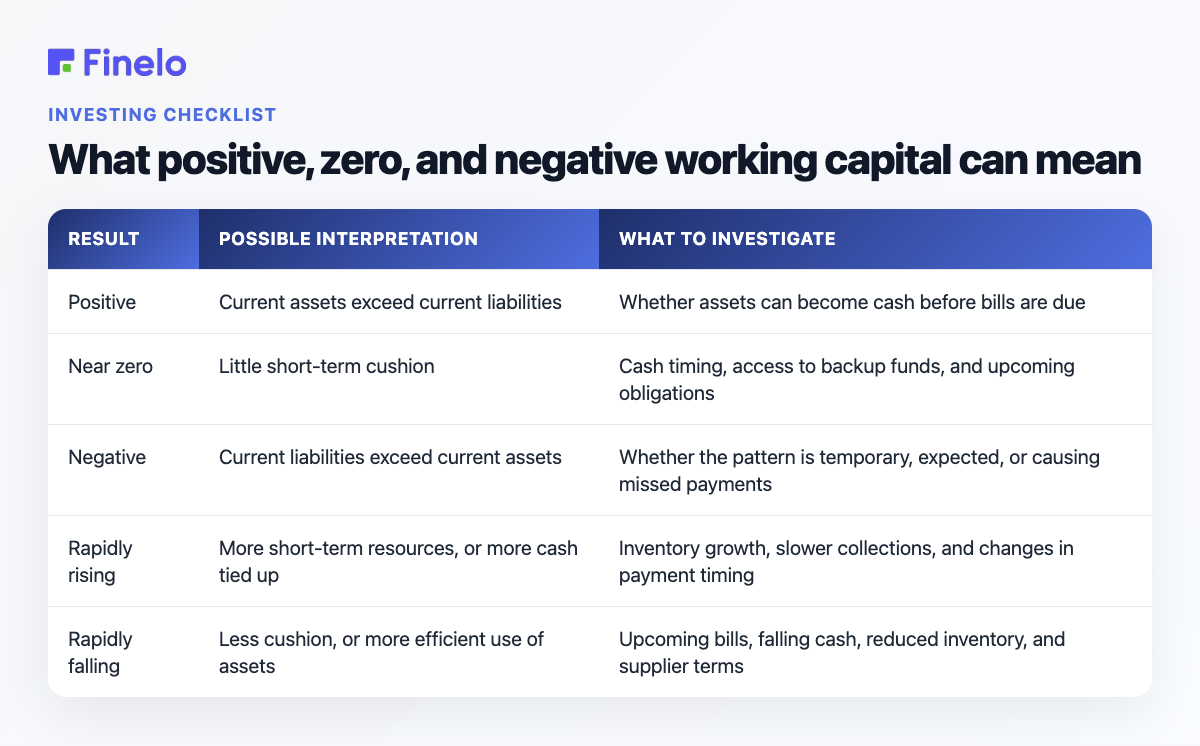

What positive, zero, and negative working capital can mean

The number is a starting point for analysis, not a pass-or-fail grade.

| Result | Possible interpretation | What to investigate |

|---|---|---|

| Positive | Current assets exceed current liabilities | Whether assets can become cash before bills are due |

| Near zero | Little short-term cushion | Cash timing, access to backup funds, and upcoming obligations |

| Negative | Current liabilities exceed current assets | Whether the pattern is temporary, expected, or causing missed payments |

| Rapidly rising | More short-term resources, or more cash tied up | Inventory growth, slower collections, and changes in payment timing |

| Rapidly falling | Less cushion, or more efficient use of assets | Upcoming bills, falling cash, reduced inventory, and supplier terms |

Negative working capital deserves attention, but context matters. Some businesses collect from customers quickly and pay suppliers later. Others must fund inventory or long projects well before receiving payment. The same number can therefore signal different levels of risk in different operating models.

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

The working capital cycle

The working capital cycle describes how money moves through day-to-day operations:

Cash → inventory or operating inputs → sale → receivable → cash

The longer cash remains tied up in that sequence, the more funding the business may need to support operations. Three timing questions are especially useful:

- How long does inventory remain unsold?

- How long do customers take to pay?

- How long does the business have to pay suppliers?

A company can shorten the cycle by improving one or more of these stages, but every change has tradeoffs. Holding less inventory may free cash but increase the chance of shortages. Tightening customer terms may improve collections but make the offer less attractive. Delaying supplier payments without agreement may protect cash temporarily while damaging important relationships.

Signs of poor working capital management

One weak month does not establish a pattern. Repeated operational symptoms are more informative:

- bills are regularly paid late;

- payroll or tax obligations create recurring cash emergencies;

- profitable sales are followed by cash shortages;

- customer invoices remain unpaid longer than expected;

- inventory accumulates without matching demand;

- frequent short-term borrowing is needed for routine expenses;

- suppliers reduce credit terms or require payment in advance;

- management cannot explain major changes in receivables, inventory, or payables; or

- the working capital calculation deteriorates across several periods.

The cause matters. Falling working capital could reflect a sales slowdown, excessive purchasing, weak collections, debt coming due, or a planned investment. Diagnosis should come before action.

How to improve working capital

Improvement does not always mean maximizing the number. The goal is to maintain enough liquidity while using resources productively.

Collect receivables more deliberately

Issue accurate invoices promptly, make payment dates clear, monitor overdue accounts, and resolve disputes early. Before extending credit, consider whether the proposed terms fit the company’s own cash needs.

Manage inventory by demand

Separate fast-moving, slow-moving, seasonal, and obsolete stock. Purchasing decisions should reflect realistic demand and replenishment times. Discounting or discontinuing stagnant items may release cash, although it can reduce margins.

Coordinate supplier payments

Track due dates and use agreed payment terms fully. If timing is consistently difficult, discuss revised terms before invoices become overdue. The objective is a workable arrangement, not simply paying as late as possible.

Plan short-term cash needs

A rolling cash forecast can map expected receipts and payments by week or month. Compare forecast and actual figures, then investigate meaningful differences. Scenario planning can also show what happens if customers pay later, input costs rise, or sales slow.

Review financing carefully

Short-term financing can bridge a genuine timing gap, but borrowing costs and repayment terms can add pressure. Compare the duration of the financing with the duration of the need, and assess affordability under less favorable conditions. This is a business decision that may warrant advice from a qualified accounting or finance professional.

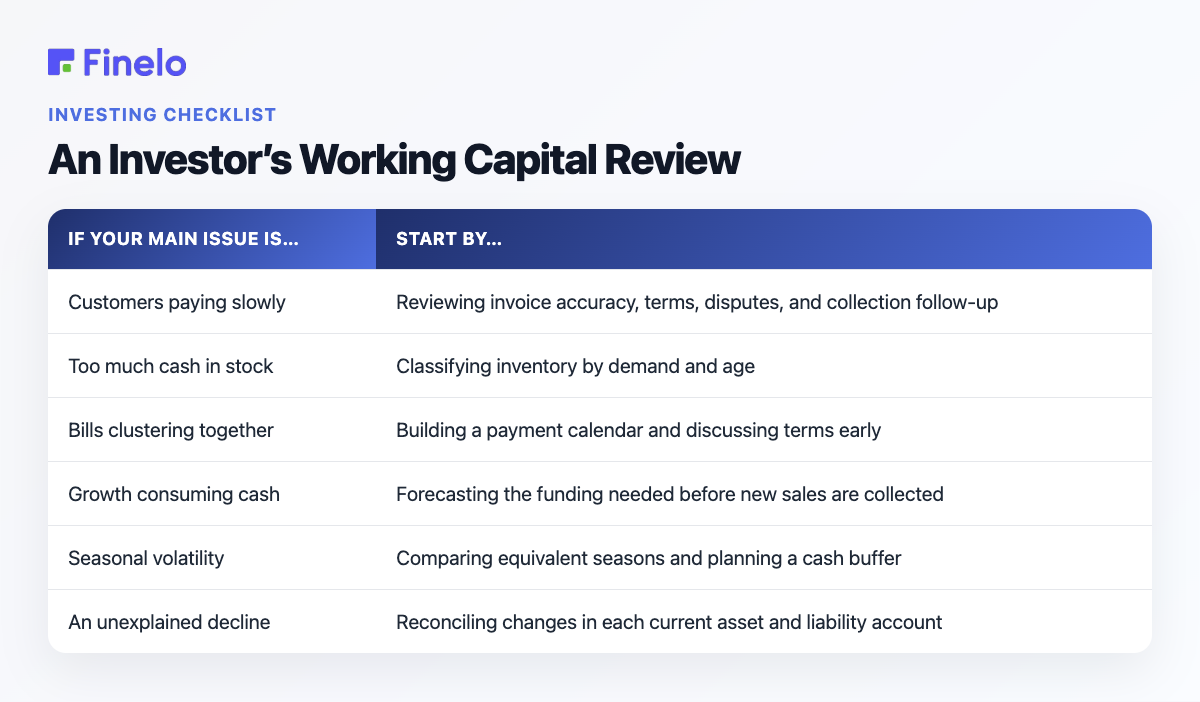

An Investor’s Working Capital Review

Use the following sequence when reviewing a company:

- Calculate: Find working capital using balance-sheet figures from one date.

- Compare: Review the result against prior months, quarters, or equivalent seasonal periods.

- Inspect: Break the movement into cash, receivables, inventory, payables, and debt due soon.

- Time: Map when major assets should become cash and when liabilities must be paid.

- Stress-test: Consider delayed customer payments, weaker sales, higher costs, or an unexpected expense.

- Act: Choose the narrowest response that addresses the cause.

- Monitor: Assign responsibility and review whether the action improved cash timing without creating a new operational problem.

| If your main issue is… | Start by… |

|---|---|

| Customers paying slowly | Reviewing invoice accuracy, terms, disputes, and collection follow-up |

| Too much cash in stock | Classifying inventory by demand and age |

| Bills clustering together | Building a payment calendar and discussing terms early |

| Growth consuming cash | Forecasting the funding needed before new sales are collected |

| Seasonal volatility | Comparing equivalent seasons and planning a cash buffer |

| An unexplained decline | Reconciling changes in each current asset and liability account |

Tools for Monitoring Working Capital

A complicated system is not required to begin. The essential tool is a consistent record of balances and timing. Depending on the size of the business, that may include:

- an accounting system with an up-to-date balance sheet;

- an aged receivables report;

- an aged payables report;

- an inventory report showing quantity, value, and age;

- a rolling cash-flow forecast;

- a payment calendar; and

- a simple dashboard tracking working capital and its main components over time.

Automation can reduce manual work, but reports are only useful when records are complete and categories are applied consistently. Someone should still review exceptions, investigate unusual movements, and connect the numbers to what is happening operationally.

Investor Takeaway and Next Steps

Start with the latest balance sheet, calculate working capital, and compare it with several relevant prior periods. Then identify which account caused the largest change and read management’s explanation in the filing. Compare revenue and profit growth with operating cash flow. Persistent growth in overdue receivables, slow inventory, or short-term debt can signal pressure even when reported earnings look healthy.

Finelo provides financial education for readers building their understanding of company analysis and investing. This article is educational, does not recommend a security, and does not replace accounting or personalized financial advice.

Frequently asked questions

Is working capital the same as cash flow?

No. Working capital is a balance-sheet calculation at a point in time. Cash flow describes money moving into and out of a business over a period. Changes in receivables, inventory, and payables can affect cash even when the business reports a profit.

How often should working capital be reviewed?

Review frequency should match the pace and volatility of the business. A stable business may include it in a regular monthly reporting cycle, while a seasonal, fast-growing, or cash-constrained company may need more frequent monitoring.

Is higher working capital always better?

No. More working capital can provide a larger cushion, but an unusually high amount may indicate idle cash, excess inventory, or slow customer collections. The quality and timing of the underlying assets matter.

Can a profitable company have working capital problems?

Yes. Profit can be recorded before cash is collected, while inventory and operating expenses may require earlier payment. A company can therefore appear profitable and still struggle to meet short-term obligations.

InvestingBeginnerFinancial StatementsMarkets

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Investing

What is Venture Capital?

Venture capital (VC) is money invested in young businesses in exchange for equity, or an ownership stake. It is generally aimed at startups and early-stage companies that need capital to develop a product, hire people…

Finelo Team

Investing

What Is the S&P 500? A Complete Overview

The S&P 500 is a stock market index designed to show how a broad group of leading large-cap U.S. companies is performing. Rather than checking hundreds of stocks individually, investors can look at the index for a…

Finelo Team

Investing

What is the Russell 2000? A Deep Dive into the Index

The Russell 2000 is a stock market index designed to track the small-cap segment of the US equity market. It contains approximately 2,000 of the smallest US companies selected by market capitalization and represents…

Finelo Team