Financial Literacy guideUnderstanding the 50/30/20 Budget Rule

financial literacy7 min read

Understanding the 50/30/20 Budget Rule: Your Path to Financial Freedom

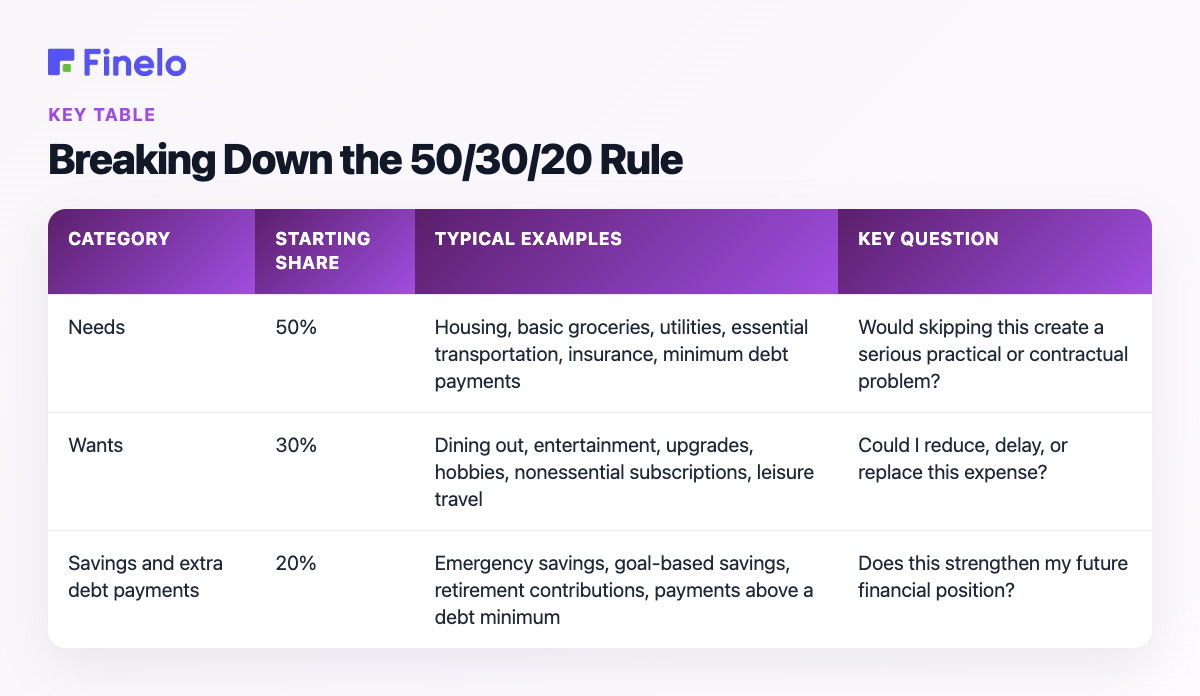

The 50/30/20 budget rule divides income into three broad categories: 50% for needs, 30% for wants, and 20% for savings. Charles Schwab describes the same core allocation. In practice, many people also use the 20%…

•7 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

The 50/30/20 budget rule divides income into three broad categories: 50% for needs, 30% for wants, and 20% for savings. Charles Schwab describes the same core allocation. In practice, many people also use the 20% category for payments above required debt minimums. The rule is a starting framework, not a rigid test of financial success. Its value is that it turns a long list of transactions into three understandable priorities.

Explore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

For example, with $3,000 in monthly take-home pay, the starting targets would be $1,500 for needs, $900 for wants, and $600 for savings or extra debt payments. Your actual percentages may need to change with housing costs, irregular income, debt obligations, or short-term goals.

Breaking Down the 50/30/20 Rule

The rule applies to income after taxes and payroll deductions—the amount available to budget. Multiply that figure by 0.50, 0.30, and 0.20 to calculate the three targets.

The hardest category decision is often not mathematical. It is deciding whether an expense is essential.

A basic phone plan needed for work may be a need; a premium device upgrade may be a want. Transportation to work may be essential, while the difference between a practical option and a more expensive preference belongs under wants. Groceries are generally a need, but convenience purchases and frequent takeout may fit better under wants.

When an expense includes both elements, split it if that produces a more useful picture. If splitting every transaction becomes exhausting, classify it according to its main purpose and stay consistent from month to month.

Savings and debt payments

The 20% category can serve several goals. It may include building an emergency cushion, saving for a planned expense, contributing toward retirement, or paying more than the required minimum on debt.

Minimum required debt payments generally belong with needs because they are current obligations. Any amount paid above the minimum can be treated as part of the 20% category. This distinction prevents the same payment from being counted twice.

A Practical 50/30/20 Budget Example

Consider a person with $4,000 in monthly take-home income. The guideline produces these targets:

Needs: $2,000

Wants: $1,200

Savings and extra debt payments: $800

Suppose the person records $2,250 in needs, $950 in wants, and $800 in savings and extra debt payments. The total still equals $4,000, but needs are 56.25% rather than 50%.

That does not automatically mean the budget has failed. It identifies the pressure point. If the higher essential costs cannot be reduced immediately, the person could temporarily lower wants to preserve the savings target. If even that is unrealistic, the percentages can become a longer-term direction rather than a monthly requirement.

The useful question is not “Did every category land perfectly?” It is “What does this difference tell me about my choices and constraints?”

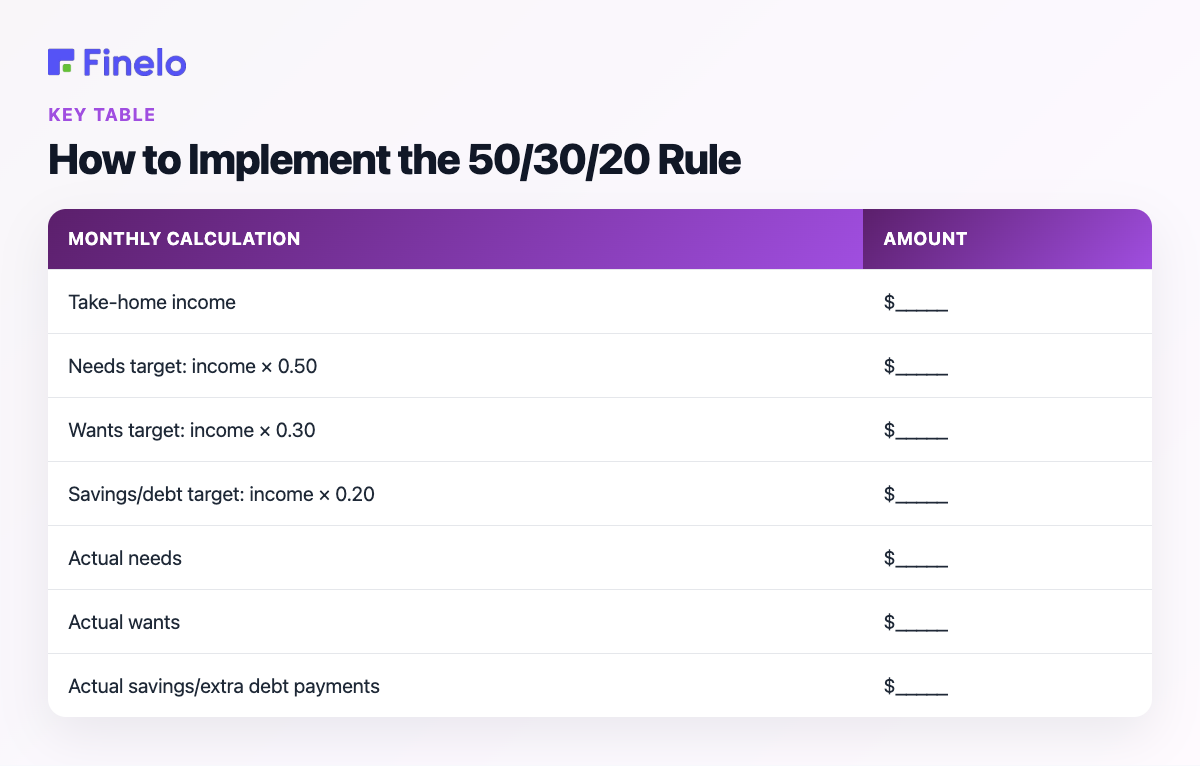

Calculate average monthly take-home income. For variable income, use a cautious working figure based on lower-earning months or a recent multi-month average.

Review recent bank, card, and cash spending. Include less frequent bills by converting them into monthly amounts.

Assign each expense to needs, wants, or savings and extra debt payments.

Add each category and divide it by take-home income.

Compare the result with 50%, 30%, and 20%.

Choose one realistic adjustment for the next month.

Use this basic worksheet:

Monthly calculation

Amount

Take-home income

$_____

Needs target: income × 0.50

$_____

Wants target: income × 0.30

$_____

Savings/debt target: income × 0.20

$_____

Actual needs

$_____

Actual wants

$_____

Actual savings/extra debt payments

$_____

Reference table from this guide — How to Implement the 50/30/20 Rule.

Reviewing actual spending matters because small recurring purchases can be easy to underestimate. At the end of the month, compare totals, note unusual expenses, and decide whether the next budget needs a spending change or a more realistic target.

Tools and Resources for Budgeting

The best budgeting tool is one you can maintain. Options include:

A spreadsheet with income, transaction, category, and monthly-total columns

A notes app with three running category totals

Your bank’s transaction export, categorized in batches

A budgeting app that supports custom categories and recurring transactions

Separate savings accounts or labeled savings goals for distinct priorities

Automation can reduce the number of decisions required. For example, a recurring transfer scheduled around payday can move part of the savings allocation before it blends into general spending. Check the timing and amount against your cash-flow needs to avoid creating a shortfall for bills.

Advantages of the 50/30/20 Rule

The main advantage of the 50/30/20 rule is clarity. Three categories are easier to review than dozens of narrow spending limits, and the percentages make the framework usable at different income levels. It also gives savings a planned place instead of leaving it to whatever remains at month-end.

The simplicity is also its main limitation. A three-category budget does not show whether one large cost—such as housing—is crowding out every other need. It may also be difficult to apply when income changes sharply, essential costs are unusually high, or debt repayment needs to take priority.

Use the rule when you want a quick overview and flexible boundaries. Consider a more detailed category-by-category or cash-flow budget when bill timing is the main problem, spending requires close control, or the broad categories conceal important details.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Personal circumstances matter more than matching the numbers exactly. Fidelity similarly describes percentage-based budgeting numbers as goals rather than hard rules. Keep the three-category structure if it helps, but adjust the shares deliberately.

Your situation

Possible next step

Essential costs exceed 50%

Separate fixed and adjustable needs, reduce wants where practical, and set a gradual target rather than forcing an immediate change

Income varies

Build the budget around a conservative income figure and decide in advance how higher-income months will be allocated

You cannot save 20% yet

Start with a sustainable amount, automate it if appropriate, and increase it when an expense ends or income rises

Debt is the main priority

Keep minimum payments under needs and direct some or all of the 20% category toward additional payments

A short-term goal is urgent

Temporarily reduce wants and label the redirected amount so the tradeoff remains visible

Your needs are well below 50%

Avoid treating the unused amount as automatically available for wants; consider assigning it to goals that matter to you

Reference table from this guide — How to Adjust the Percentages.

An adjusted budget should still add up to 100%. Writing down both the percentages and the reason for changing them makes the plan easier to evaluate later.

Common Mistakes to Avoid

Budgeting with gross income. Percentages based on money that never reaches your account can overstate what is available. Use take-home income consistently.

Calling every recurring expense a need. A subscription does not become essential simply because it renews automatically. Ask what would happen if you canceled or downgraded it.

Ignoring irregular expenses. Annual fees, repairs, gifts, and seasonal costs can disrupt a seemingly balanced month. Estimate their yearly total and set aside a monthly amount.

Counting transfers twice. Moving money from checking to savings is an allocation, not a new expense in addition to the savings category.

Changing too much at once. A budget is easier to maintain when the next action is specific—cancel one unused service, set one transfer, or cap one flexible category.

Treating the percentages as a verdict. The framework is meant to reveal tradeoffs. If the targets are unrealistic, adjust them and focus on steady improvement rather than hiding necessary expenses.

Conclusion and Next Steps

A percentage rule is only useful when you understand the decisions behind it. Finelo focuses on finance learning, making this guide part of a broader educational approach to understanding money concepts before acting on them.

This article is educational rather than personalized financial advice. Your income, obligations, local costs, benefits, taxes, and financial goals can change which budget structure is suitable. Check the terms and costs of any financial product independently, and seek qualified guidance when a decision requires advice tailored to your circumstances.

Your next step is straightforward: calculate one month of take-home income, categorize recent spending, and compare your actual percentages. Use the result as information—not judgment—and make one manageable change for the month ahead.

Frequently asked questions

What if an expense fits two categories?

Classify it by its primary purpose or split it into essential and optional portions. Consistency is more useful than pursuing a perfect label for every purchase.

How often should I review a 50/30/20 budget?

A monthly review works well for comparing income and expenses, but check more frequently when starting, when income varies, or when cash flow is tight. Revisit the percentages after a major change in income, housing, debt, or household responsibilities.

What should I do if I cannot save 20%?

Choose a smaller amount that does not prevent you from covering essential obligations. Then identify a trigger for increasing it, such as paying off a balance, ending a subscription, or receiving higher income. A sustainable starting point is more useful than a target abandoned after one month.

Is the 50/30/20 rule right for everyone?

No single budget structure fits every household. The rule is most useful for someone who wants a simple overview of spending priorities. If your income is highly variable, your required costs dominate the budget, or you need precise control over every dollar, a more detailed method may be a better fit.

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.