Best answer: APR shows the annual cost of borrowing, while APY shows the annual yield on money held in an interest-bearing deposit account.

APR vs APY: Understanding the Key Differences

APR and APY both express a rate on an annual basis, but they answer different questions. APR helps you compare what you’ll pay to borrow; APY helps you compare what you may earn on deposits. This page is for borrowers…

7 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

Who it’s for: Borrowers comparing a loan or credit card and savers comparing deposit accounts.

Recommended next step: Compare APR with APR when borrowing or APY with APY when saving, then review the fees and conditions behind each rate.

APR and APY both express a rate on an annual basis, but they answer different questions. APR helps you compare what you’ll pay to borrow; APY helps you compare what you may earn on deposits. This page is for borrowers reviewing a loan or credit card and savers choosing an interest-bearing account. The recommended next step is simple: if you’re borrowing, compare APRs across similar offers; if you’re saving, compare APYs across similar accounts. Then review the fees, term, balance rules, and penalties behind the percentage before deciding.

Who this comparison is for and what to do next

This APR vs APY comparison is for anyone deciding between borrowing offers or deposit accounts. Choose the side that matches your goal:

- Borrowing money: compare APRs across similar loans or credit cards, then check the term, fees, payments, and total amount you’ll repay.

- Saving money: compare APYs across similar deposit accounts, then check balance requirements, fees, rate changes, and withdrawal penalties.

APR and APY are not interchangeable scores. Use APR to assess borrowing costs and APY to assess deposit earnings.

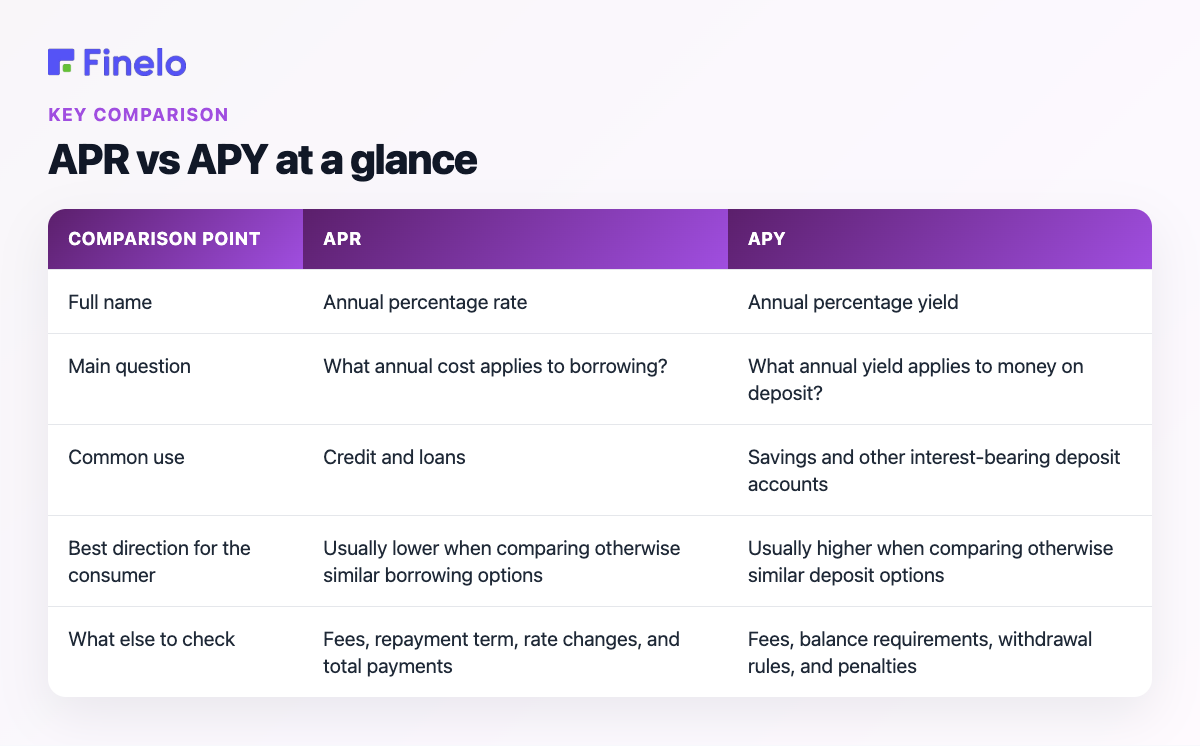

APR vs APY at a glance

| Comparison point | APR | APY |

|---|---|---|

| Full name | Annual percentage rate | Annual percentage yield |

| Main question | What annual cost applies to borrowing? | What annual yield applies to money on deposit? |

| Common use | Credit and loans | Savings and other interest-bearing deposit accounts |

| Best direction for the consumer | Usually lower when comparing otherwise similar borrowing options | Usually higher when comparing otherwise similar deposit options |

| What else to check | Fees, repayment term, rate changes, and total payments | Fees, balance requirements, withdrawal rules, and penalties |

APR is the required format for advertised credit rates under federal rules, and the abbreviation “APR” may be used for annual percentage rate disclosures (Consumer Financial Protection Bureau). For loans, APR can include the interest rate plus additional fees charged with the loan (CFPB). APY is a standardized way to disclose interest earned so consumers can compare deposit accounts across banks (FDIC).

The two rates are therefore not rivals competing to describe the same transaction. They are different comparison tools for different sides of personal finance.

What is APR?

APR stands for annual percentage rate. It puts the cost of credit into an annual percentage format, making it easier to compare borrowing offers presented on the same basis. The CFPB explains that a loan’s APR measures its interest rate plus additional fees charged with the loan (CFPB). Federal advertising rules also require advertised credit rates to be stated as an annual percentage rate (CFPB).

For a borrower, APR is a starting point for comparing options such as loans or credit cards. A lower APR will generally look more attractive than a higher APR when every other part of the offers is genuinely the same. The APR can include interest and certain loan fees, but you should still read the complete disclosure to understand what you’ll pay. In practice, offers may differ in several ways, so the comparison also needs to consider:

- How long the borrowing period lasts

- Whether the rate can change

- What fees or charges apply

- The size and timing of required payments

- The total amount paid under the agreement

APR is most useful when comparing like with like. A rate attached to one kind of credit may not tell the whole story when placed beside a product with a different term, repayment structure, or set of conditions.

How is APR calculated?

The exact calculation depends on the credit product and its required disclosures. For a quick learning exercise, you can annualize a simple periodic rate by multiplying it by the number of equal periods in a year. For example, a hypothetical monthly rate of 1% corresponds to a simple annualized rate of 12%:

1% × 12 months = 12%

That illustration is not a substitute for the disclosed APR. Real offers can have product-specific rules and charges, so use the lender’s official disclosure when comparing actual credit.

What is APY?

APY stands for annual percentage yield. It is used to compare the rate of interest earned on deposit accounts. The FDIC describes APY as a common disclosure method intended to help consumers compare accounts between banks, while also warning that APY does not compare early-withdrawal penalties (FDIC).

APY helps compare the amount of interest an account can earn on an annual basis. It is especially helpful because the timing of interest matters. When earned interest remains in an account and later earns additional interest, the balance can grow through compounding. More frequent compounding can produce a different annual result from simple interest, even when the stated periodic rate initially looks similar.

This means savers should compare APY with APY—not APY with an unadjusted interest rate. They should also check the account conditions behind the advertised number, including:

- Minimum balances

- Monthly or maintenance fees

- Whether the rate can change

- Withdrawal restrictions

- Penalties that APY does not capture

How is APY calculated?

A common conceptual form is:

APY = (1 + periodic rate) ^ number of periods − 1

Suppose, purely as an illustration, an account has a hypothetical monthly rate of 1%. Applying monthly compounding gives:

(1.01 ^ 12) − 1 ≈ 12.68%

The example shows why a compounded annual yield can differ from a simple 1% × 12 = 12% annualization. It does not represent a current account offer. For a real comparison, use the APY stated in the institution’s disclosure.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

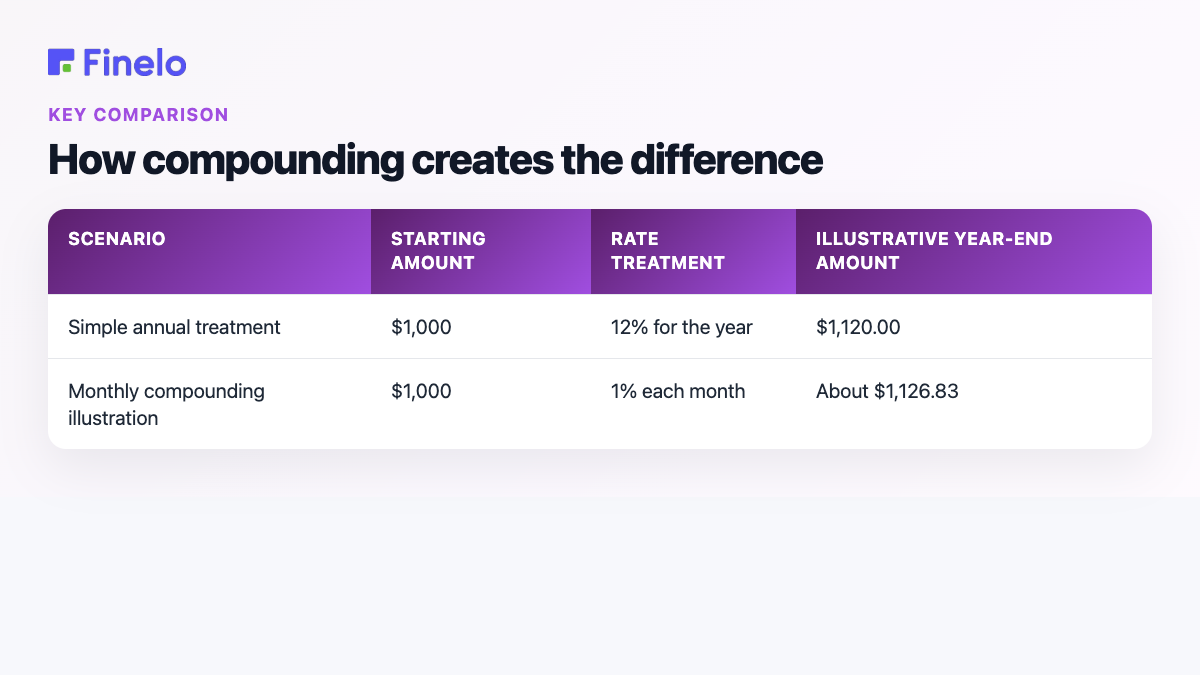

How compounding creates the difference

Compounding means previously earned interest becomes part of the balance used for later interest calculations. Its effect depends on the rate, how often compounding occurs, how long the money remains in the account, and whether money is added or withdrawn.

Consider two hypothetical one-year scenarios:

| Scenario | Starting amount | Rate treatment | Illustrative year-end amount |

|---|---|---|---|

| Simple annual treatment | $1,000 | 12% for the year | $1,120.00 |

| Monthly compounding illustration | $1,000 | 1% each month | About $1,126.83 |

The difference is about $6.83 in this simplified example. The purpose is not to suggest that a 12% deposit account is available; it is to isolate the mathematical effect of compounding. With real products, rates, fees, changing balances, and account rules can alter the result.

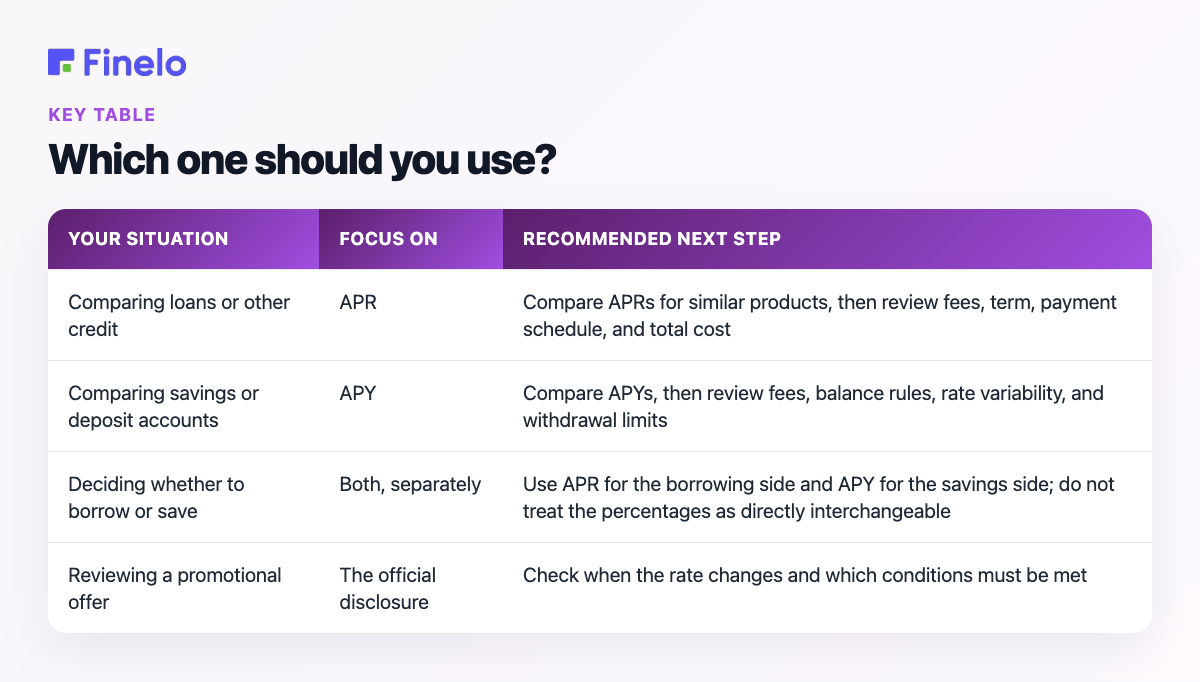

Which one should you use?

The better measure depends on what you are comparing.

| Your situation | Focus on | Recommended next step |

|---|---|---|

| Comparing loans or other credit | APR | Compare APRs for similar products, then review fees, term, payment schedule, and total cost |

| Comparing savings or deposit accounts | APY | Compare APYs, then review fees, balance rules, rate variability, and withdrawal limits |

| Deciding whether to borrow or save | Both, separately | Use APR for the borrowing side and APY for the savings side; do not treat the percentages as directly interchangeable |

| Reviewing a promotional offer | The official disclosure | Check when the rate changes and which conditions must be met |

“Lower APR” and “higher APY” are useful shortcuts, but they are not complete decisions. A loan with a lower APR may have a different term or payment structure. A deposit account with a higher APY may have fees or restrictions that reduce its usefulness for your needs. The FDIC specifically notes that APY does not compare early-withdrawal penalties (FDIC).

Practical examples

Comparing two borrowing offers

Imagine two hypothetical loans for the same amount and term. Offer A has the lower APR, but Offer B has a payment schedule that better fits the borrower’s cash flow. APR identifies the lower annual rate, but the borrower should still inspect all disclosed costs and obligations before choosing.

The lesson: use APR to narrow the field, then compare the complete terms.

Comparing two savings accounts

Imagine Account A advertises a higher APY than Account B. Account A also requires a minimum balance and charges a fee if the balance falls below it. A saver who cannot reliably maintain that balance may find that the apparently higher-yield account is not the better practical fit.

The lesson: use APY to compare earning rates, then test the account rules against how you will actually use the account.

The bottom line

APR helps you evaluate the annual rate attached to borrowing; APY helps you evaluate the annual yield on deposits. Start by comparing the correct measure across similar products, then read the full terms behind the number.

For a practical next step, write down whether you are borrowing or saving, collect the official disclosures for at least two comparable options, and place the APRs or APYs side by side with their fees and conditions. Finelo’s educational resources can help you continue building the financial vocabulary needed to review those tradeoffs, but the final choice should reflect your own goals, costs, and risk tolerance.

Frequently asked questions

Is APY always higher than APR?

No universal comparison is meaningful because APR and APY usually describe different products. APR concerns credit rates; APY concerns deposit yields. Even when the percentages are mathematically related, product terms and calculation conventions matter.

Why do banks show APY on savings accounts?

APY gives consumers a standardized annual measure for comparing interest earned on deposit accounts. The FDIC says this common disclosure method is intended to support comparisons between banks ([FDIC](https://www.fdic.gov/consumers/consumer/news/september2018.html)).

Should I calculate APR and APY myself?

Manual calculations are useful for understanding the concepts, but actual decisions should rely on official product disclosures. Use a calculator to explore scenarios, then verify the stated APR or APY and every relevant condition with the financial institution.

Can fees make a lower APR or higher APY less attractive?

Yes. A percentage is only one part of an offer. Compare applicable fees, term lengths, payment or balance requirements, rate changes, and penalties before deciding what fits your situation.

Financial LiteracyBeginnerInterest RatesPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team