The central difference is what the plan defines. A defined benefit plan sets a retirement benefit in advance, while a defined contribution plan sets up an individual account funded by employee or employer contributions. The first emphasizes predictable benefits; the second makes the eventual amount depend on the account and places investment risk on the employee. Neither is automatically better for everyone. The more useful question is whether you value income predictability or account ownership and investment control—and what your employer actually offers.

Defined Benefit vs Defined Contribution Plans: Key Differences and Insights

The central difference is what the plan defines. A defined benefit plan sets a retirement benefit in advance, while a defined contribution plan sets up an individual account funded by employee or employer…

5 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

This comparison is for employees reviewing workplace benefits, people changing jobs, and beginners trying to understand how retirement plan design affects risk, flexibility, and future income.

How the two retirement plan types work

Defined benefit plan

A defined benefit plan promises a benefit determined by the plan rather than simply giving the participant an investment account balance. The IRS describes the benefit as fixed and pre-established. It also notes that these plans can be more complex and costly for employers to establish and maintain.

For an employee, the attraction is predictability: the plan defines the benefit to be paid under its rules. The tradeoff is that the employee generally has less direct control over how the money supporting that benefit is invested. The value of the plan also depends on details such as its benefit formula, eligibility rules, vesting terms, and available payment options. Those details must be checked in the employer’s plan documents.

Defined contribution plan

A defined contribution plan creates an individual retirement account for the participant. Contributions may come from the employee, the employer, or both. Unlike a defined benefit plan, it does not promise a specific payment at retirement, and Investor.gov says the employee bears the investment risks.

This structure gives the employee a visible account and usually requires more personal decision-making. The eventual retirement value is not fixed in advance. It can be affected by contribution choices, the investments available through the plan, investment results, and costs. That flexibility can be useful, but it also creates responsibility: saving too little, taking unsuitable risk, or overlooking fees may weaken the account’s ability to support retirement.

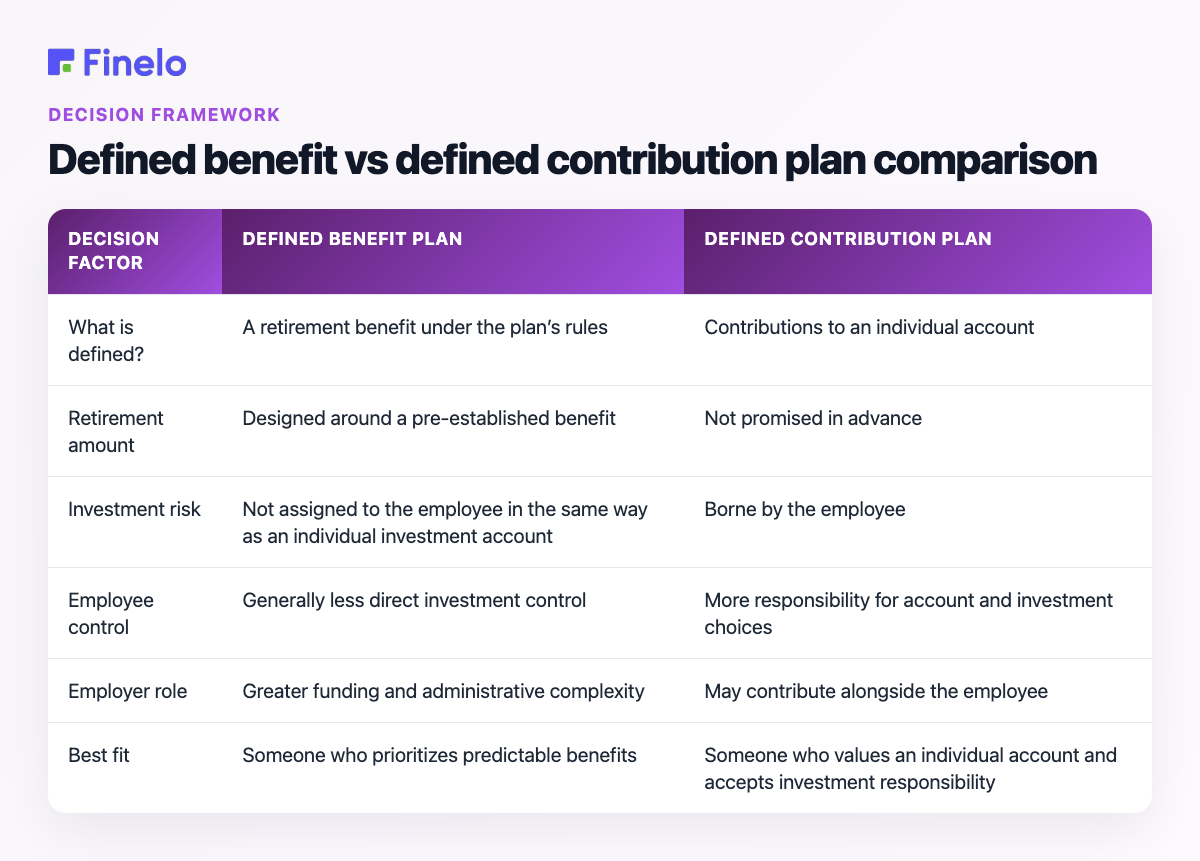

Defined benefit vs defined contribution plan comparison

| Decision factor | Defined benefit plan | Defined contribution plan |

|---|---|---|

| What is defined? | A retirement benefit under the plan’s rules | Contributions to an individual account |

| Retirement amount | Designed around a pre-established benefit | Not promised in advance |

| Investment risk | Not assigned to the employee in the same way as an individual investment account | Borne by the employee |

| Employee control | Generally less direct investment control | More responsibility for account and investment choices |

| Employer role | Greater funding and administrative complexity | May contribute alongside the employee |

| Best fit | Someone who prioritizes predictable benefits | Someone who values an individual account and accepts investment responsibility |

The table shows why “which plan is better?” has no universal answer. A defined benefit plan may be more appealing when predictable retirement income is the priority. A defined contribution plan may fit someone who values portability, visibility, and investment choice. But plan quality depends on the actual terms, not just the category name.

Advantages, limitations, and economic risk

The main advantage of a defined benefit plan is clarity about the benefit the plan is designed to provide. That can make retirement-income planning easier. Its limitations may include less investment control and rules that make the benefit less flexible when an employee leaves before retirement.

For employers, these plans require more complex administration, according to the IRS. Changes in investment conditions, interest rates, funding needs, or workforce structure can therefore affect the cost and difficulty of maintaining the promised benefits. Employees should not assume that every defined benefit plan has identical protections or payment choices.

The main advantage of a defined contribution plan is the individual account. Employees can see the balance and make choices within the plan’s available options. The limitation is uncertainty: the plan does not define the retirement payment, and the employee carries investment risk.

Inflation matters to both designs. A fixed future payment may buy less over time unless the plan’s terms provide an adjustment. A defined contribution account has no automatic protection either; its future purchasing power depends on contributions, investment outcomes, costs, withdrawals, and inflation. Review the actual plan rather than assuming either structure solves inflation risk.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

A practical example

Consider two employees with different priorities.

Maya expects to stay with one employer for many years and wants retirement planning built around a predictable benefit. A defined benefit plan could align with those priorities, provided she understands the benefit formula, vesting rules, and payment choices.

Daniel changes jobs more often and prefers to see and manage an individual retirement account. A defined contribution plan may better match his preference, but he must decide how much to contribute and how to use the investments available to him. His outcome is not predetermined.

These examples illustrate fit, not guaranteed results. Two plans in the same category can have materially different rules and value.

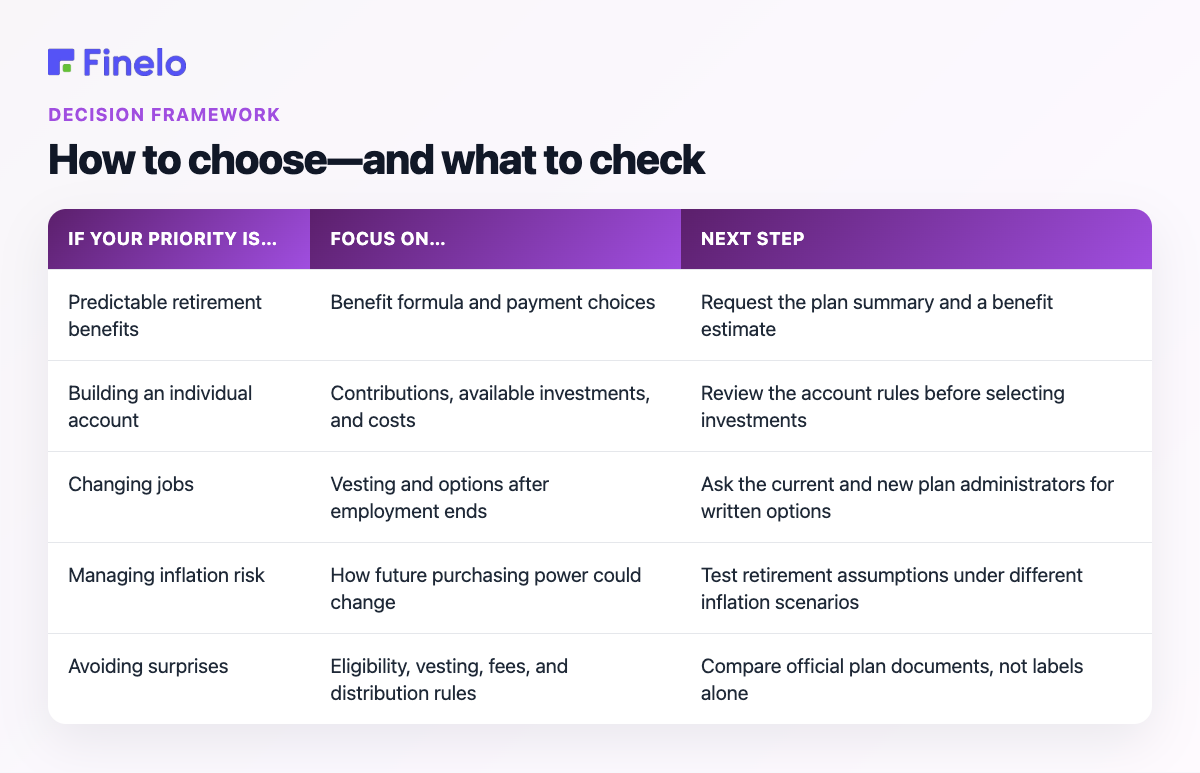

How to choose—and what to check

You may not be able to choose the plan type itself because it is commonly determined by the employer. You can still make a better benefits decision by comparing the terms that affect you.

| If your priority is… | Focus on… | Next step |

|---|---|---|

| Predictable retirement benefits | Benefit formula and payment choices | Request the plan summary and a benefit estimate |

| Building an individual account | Contributions, available investments, and costs | Review the account rules before selecting investments |

| Changing jobs | Vesting and options after employment ends | Ask the current and new plan administrators for written options |

| Managing inflation risk | How future purchasing power could change | Test retirement assumptions under different inflation scenarios |

| Avoiding surprises | Eligibility, vesting, fees, and distribution rules | Compare official plan documents, not labels alone |

When switching jobs, first identify whether you have a promised future benefit or an individual account. Then ask the plan administrator what can remain in the old plan, what—if anything—can move, what deadlines apply, and whether taxes or penalties could result from a distribution. Do not act on a generic rollover rule without checking your specific plan and obtaining appropriate tax guidance.

Your next step

Collect your plan summary, latest statement, and any benefit estimate. Mark which features are fixed, which depend on your choices, and which questions require an answer from the administrator. Finelo’s investment learning resources can help you build the vocabulary to evaluate financial choices, but retirement decisions should be based on your official plan documents and, when needed, qualified financial or tax advice.

Frequently asked questions

Which plan is better for retirement?

Neither plan type is inherently best. Defined benefit plans emphasize a pre-established benefit. Defined contribution plans emphasize an individual account and place investment risk on the employee. Compare the actual plan terms with your need for predictability, control, mobility, and risk tolerance.

What should I review before enrolling?

Check eligibility, vesting, employee and employer contributions, investment choices, costs, benefit calculations, distribution options, and what happens if you leave the employer. Use the formal plan materials as the authority.

Can I have both types of plans?

An employer’s benefits package may include more than one retirement arrangement, but availability and participation rules vary. Confirm what is offered and how the plans interact before making contribution or retirement decisions.

Financial LiteracyBeginnerPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team