The short answer in the HSA vs FSA decision is that eligibility comes first, then expected health expenses and the specific rules of the accounts available to you. An HSA is only an option when you satisfy federal eligibility requirements, including qualifying health coverage. An FSA is generally considered through an employer benefits program. If both are available, neither is automatically better: the right fit depends on your financial situation, your family’s health needs, and the details in your plan documents.

HSA vs FSA: A Detailed Comparison

The short answer in the HSA vs FSA decision is that eligibility comes first, then expected health expenses and the specific rules of the accounts available to you. An HSA is only an option when you satisfy federal…

7 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

This comparison is for employees, families, and individual taxpayers reviewing benefit choices. It focuses on verified account features and a practical way to decide without assuming that every employer plan works the same way.

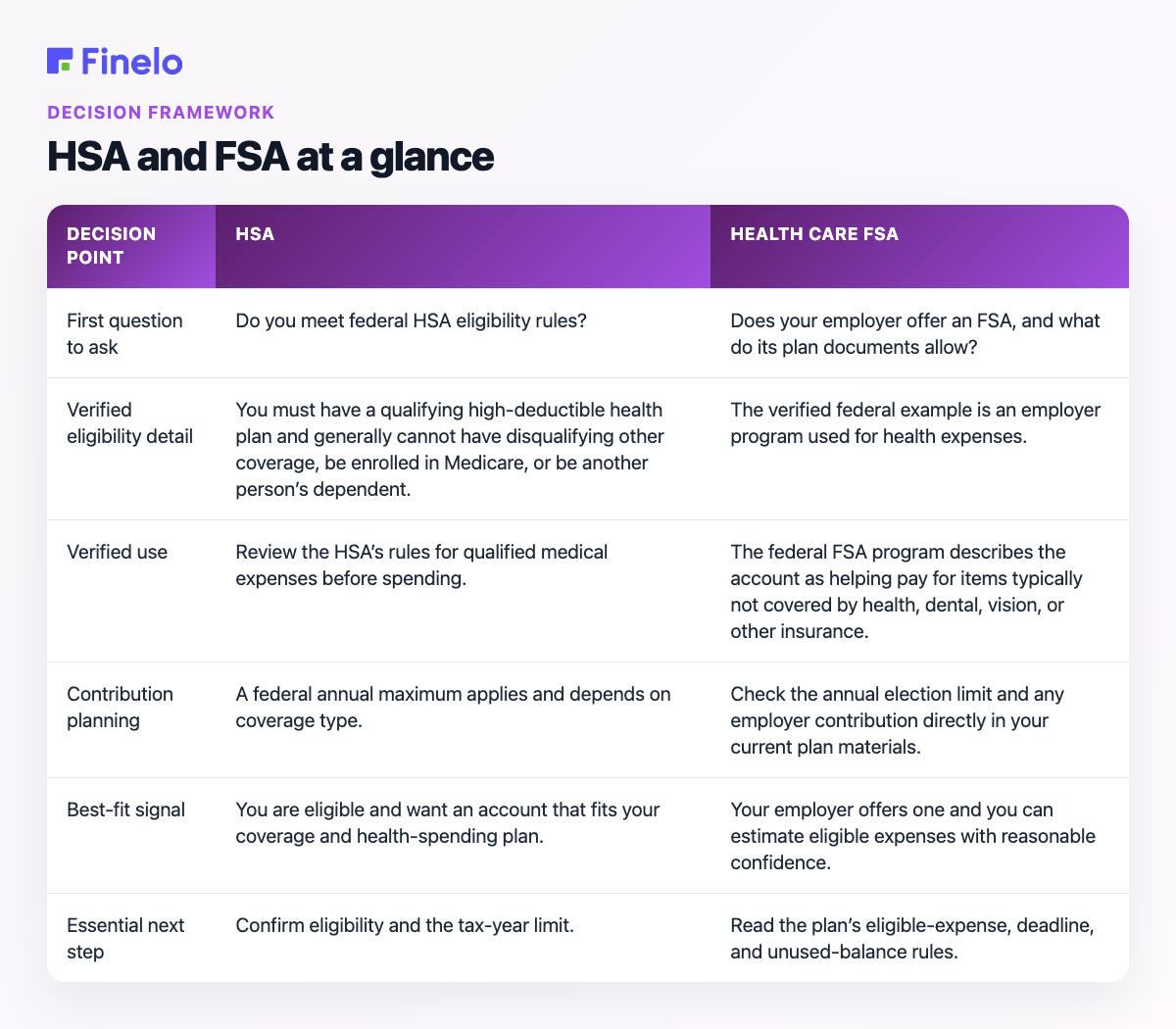

HSA and FSA at a glance

Both accounts are associated with health spending, but they reach you through different eligibility paths. That difference should shape the order in which you compare them.

| Decision point | HSA | Health care FSA |

|---|---|---|

| First question to ask | Do you meet federal HSA eligibility rules? | Does your employer offer an FSA, and what do its plan documents allow? |

| Verified eligibility detail | You must have a qualifying high-deductible health plan and generally cannot have disqualifying other coverage, be enrolled in Medicare, or be another person’s dependent. | The verified federal example is an employer program used for health expenses. |

| Verified use | Review the HSA’s rules for qualified medical expenses before spending. | The federal FSA program describes the account as helping pay for items typically not covered by health, dental, vision, or other insurance. |

| Contribution planning | A federal annual maximum applies and depends on coverage type. | Check the annual election limit and any employer contribution directly in your current plan materials. |

| Best-fit signal | You are eligible and want an account that fits your coverage and health-spending plan. | Your employer offers one and you can estimate eligible expenses with reasonable confidence. |

| Essential next step | Confirm eligibility and the tax-year limit. | Read the plan’s eligible-expense, deadline, and unused-balance rules. |

The table is a starting point, not a substitute for current plan documents. Employer FSA terms can matter as much as the account category itself.

What is an HSA?

A Health Savings Account is a tax-advantaged health account subject to federal eligibility rules. The most important fact is that wanting an HSA does not make someone eligible for one.

According to the IRS Instructions for Form 8889, you must be covered by a high-deductible health plan and have no other health coverage except certain permitted coverage. The IRS also says that an eligible person cannot be enrolled in Medicare or claimed as another person’s dependent. Anyone comparing accounts should verify these conditions before considering contribution amounts or other features.

Contribution limits are tied to the tax year and coverage type. For 2025, the same IRS instructions list a maximum contribution of $4,300 for self-only coverage and $8,550 for family coverage. Those figures are specifically for 2025; do not reuse them for another year without checking the current IRS guidance.

A practical HSA review therefore begins with three questions:

- Is your health plan HSA-eligible?

- Do Medicare enrollment, dependent status, or other health coverage affect your eligibility?

- What is the current contribution limit for your coverage type and tax year?

If any answer is unclear, confirm it with your insurer, benefits administrator, or a qualified tax professional before contributing.

What is an FSA?

A health care Flexible Spending Account is commonly offered as an employee benefit for eligible health expenses. The exact program rules come from the employer’s plan, so an FSA comparison should be based on the documents for the account you can actually enroll in.

As a first-party example, the U.S. Office of Personnel Management’s FSAFEDS description says its health care and limited-expense FSAs help participants pay for items typically not covered by their health plan, dental and vision insurance, or other health coverage. This illustrates the account’s role, but it does not mean every private employer’s FSA has identical terms.

Before choosing an FSA election amount, find clear answers to these questions:

- Which medical, dental, vision, and other expenses are eligible?

- When must an expense be incurred and a claim submitted?

- What happens to an unused balance?

- Can you change your election during the year, and under what circumstances?

- Does the employer contribute?

- When is the elected amount available for reimbursement?

These details determine whether an FSA matches your spending pattern. A predictable expense is useful for planning only if it is eligible under your plan and falls within the plan’s required dates.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Key differences that should drive your decision

Eligibility versus availability

HSA eligibility is governed by federal conditions connected to health coverage and personal status. An FSA, by contrast, is evaluated as an employer benefit: you need to know whether it is offered and what its governing plan permits.

This creates a simple sequence. First eliminate any account for which you are not eligible. Only then compare the remaining option or options.

Contribution decisions

For an HSA, check the current federal maximum and account for the type of qualifying coverage. The verified 2025 limits above demonstrate why the tax year must always be attached to a contribution figure.

For an FSA, use the current employer enrollment materials rather than a generic online number. Your election should reflect eligible expenses you can reasonably anticipate, with enough margin for uncertainty.

Spending rules

Do not assume that an expense eligible under one account is automatically handled the same way by another. Review the account’s eligible-expense rules and retain the documentation required by its administrator.

Deadlines and unused-balance treatment also deserve direct verification. These details can materially change the value of an FSA election, yet they may depend on the plan. Likewise, confirm HSA distribution rules from current official guidance before treating a withdrawal as qualified.

Tax questions

Both account types are discussed as tax-advantaged health benefits, but their tax mechanics should not be reduced to a slogan. Contributions, payroll treatment, deductions, reimbursements, and withdrawals can involve different rules.

The safe comparison is account-specific:

- For an HSA, use current IRS instructions for eligibility, contributions, reporting, and distributions.

- For an FSA, use the employer’s benefits and tax materials for payroll elections and reimbursements.

- If a transaction is unusual or the amount is significant, consider professional tax guidance.

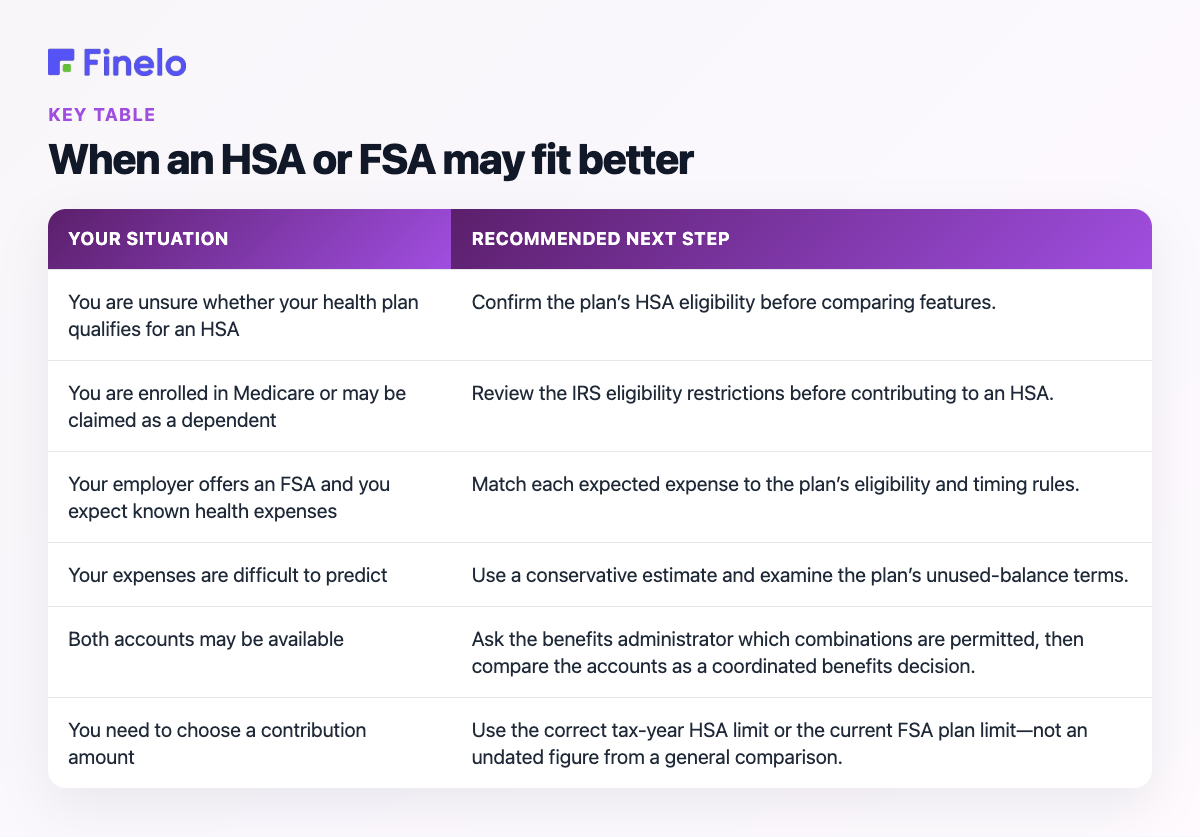

When an HSA or FSA may fit better

An HSA may deserve priority when you have confirmed eligibility and the account aligns with your current health coverage. It may also be the clearer choice when your employer does not offer a suitable health care FSA. Eligibility remains the gate: an attractive feature does not override the IRS requirements.

An FSA may be a practical fit when your employer offers one and you expect identifiable eligible expenses during the plan period. Examples might include a scheduled treatment, recurring prescriptions, or planned dental or vision care—but only after you confirm that the specific cost qualifies under your plan.

If both choices appear available, compare them with a simple worksheet:

| Your situation | Recommended next step |

|---|---|

| You are unsure whether your health plan qualifies for an HSA | Confirm the plan’s HSA eligibility before comparing features. |

| You are enrolled in Medicare or may be claimed as a dependent | Review the IRS eligibility restrictions before contributing to an HSA. |

| Your employer offers an FSA and you expect known health expenses | Match each expected expense to the plan’s eligibility and timing rules. |

| Your expenses are difficult to predict | Use a conservative estimate and examine the plan’s unused-balance terms. |

| Both accounts may be available | Ask the benefits administrator which combinations are permitted, then compare the accounts as a coordinated benefits decision. |

| You need to choose a contribution amount | Use the correct tax-year HSA limit or the current FSA plan limit—not an undated figure from a general comparison. |

Fidelity’s HSA-versus-FSA overview reaches a similarly personal conclusion: when someone is eligible for both, the choice depends on their financial circumstances and their family’s health. That is more useful than declaring a universal winner.

A final checklist before enrolling

Use this checklist during open enrollment or before making an HSA contribution:

- Confirm that you are eligible for the account.

- Obtain the current plan document or official administrator guidance.

- List expected expenses and verify each one is eligible.

- Check the applicable contribution or election limit for the correct year.

- Review deadlines, claim procedures, and unused-balance rules.

- Identify any employer funding.

- Ask whether holding or using both account types is permitted in your situation.

- Keep records needed for reimbursement or tax reporting.

This process turns “Which account is better?” into a more answerable question: “Which available account fits my verified eligibility, expenses, and plan rules?”

Bottom line

Choose an HSA only after confirming federal eligibility and the correct tax-year contribution limit. Choose an FSA after confirming that your employer offers it and that its eligible expenses, deadlines, and balance rules suit your expected spending. If both may be available, treat the decision as a coordinated benefits review rather than a contest with one automatic winner.

Finelo’s role here is educational: use this framework to organize your questions, then verify the final choice with current IRS guidance and your benefits administrator. This content is general information, not individualized tax or financial advice.

Frequently asked questions

Can I have both an HSA and an FSA?

Some benefit arrangements may involve an HSA alongside a particular type of FSA, but compatibility depends on the coverage and plan design. Do not assume a general-purpose health FSA can be combined with your HSA. Ask the benefits administrator and confirm the arrangement against current IRS eligibility guidance.

How do I know whether I am eligible for an HSA?

Start with your health coverage. The IRS says HSA contributions require coverage under a qualifying high-deductible health plan and generally no disqualifying other coverage. Medicare enrollment and being another person’s dependent also affect eligibility. Verify your exact status before contributing.

What happens if I do not use all of my FSA funds?

The answer depends on the plan’s current terms. Review its unused-balance, deadline, and reenrollment provisions before deciding how much to elect. Do not rely on another employer’s FSA rules.

Which is better for a family?

There is no universal winner. Compare HSA eligibility, the family’s expected eligible expenses, available employer benefits, contribution limits, and the administrative rules of the actual accounts. The better choice is the one that fits the family’s verified circumstances without relying on unsupported assumptions.

Financial LiteracyBeginnerPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team