Arbitrage in finance means trying to benefit from a price difference for the same or closely related asset in two places. A trader typically buys where the asset is cheaper and sells where it is more expensive, ideally at nearly the same time. Investor.gov defines arbitrage as taking advantage of “a price differential between two or more markets” and explains how this mechanism can help an exchange-traded fund’s market price move back toward its underlying value (Investor.gov).

What is Arbitrage in Finance?

Arbitrage in finance means trying to benefit from a price difference for the same or closely related asset in two places. A trader typically buys where the asset is cheaper and sells where it is more expensive, ideally…

7 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

The idea sounds simple, but a visible price gap is not automatically a profit. Fees, bid-ask spreads, taxes, timing, liquidity, and execution risk can consume the difference. For individual investors, arbitrage is therefore best understood first as a market mechanism and risk-management problem—not as easy or guaranteed money.

How arbitrage works

An arbitrage opportunity begins when two prices that should be equal or closely connected temporarily diverge. The trader constructs offsetting positions intended to capture that gap while limiting exposure to the asset’s general direction.

Consider a simplified, hypothetical example:

- An asset can be bought in Market A for $100.

- At the same moment, it can be sold in Market B for $100.40.

- The quoted spread is $0.40 per unit.

- Total trading, transfer, financing, and other execution costs are $0.28 per unit.

- The estimated remainder is $0.12 per unit before taxes and unexpected slippage.

That final line—not the quoted spread—is what matters. If the sale executes at only $100.20, costs rise, or the asset cannot be transferred or delivered as expected, the trade may produce no gain or a loss.

Why price differences appear

Price gaps can arise when markets process information at different speeds, trade at different levels of liquidity, use different currencies, or impose different access and settlement conditions. A related asset may also deviate from the value it is expected to track.

ETF arbitrage is a useful real-world mechanism. Investor.gov notes that an ETF’s market price can differ from its end-of-day net asset value and describes how authorized participants may trade with the ETF at net asset value as well as in the market. The expected effect is to bring the ETF’s market price back toward its net asset value (Investor.gov).

This illustrates a broader point: arbitrage activity can help close inconsistencies rather than leave them available indefinitely.

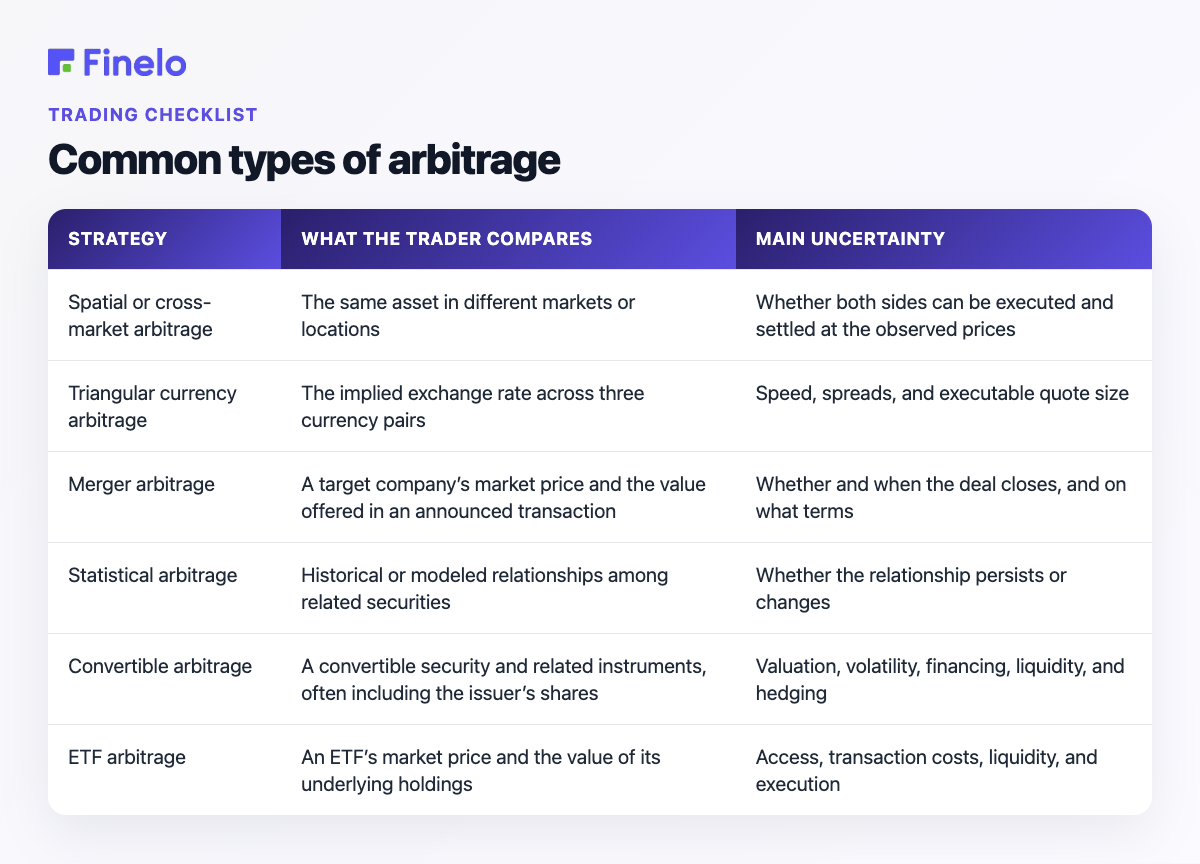

Common types of arbitrage

The word “arbitrage” covers several strategies. They differ in what is being compared and, crucially, in how much uncertainty remains.

| Strategy | What the trader compares | Main uncertainty |

|---|---|---|

| Spatial or cross-market arbitrage | The same asset in different markets or locations | Whether both sides can be executed and settled at the observed prices |

| Triangular currency arbitrage | The implied exchange rate across three currency pairs | Speed, spreads, and executable quote size |

| Merger arbitrage | A target company’s market price and the value offered in an announced transaction | Whether and when the deal closes, and on what terms |

| Statistical arbitrage | Historical or modeled relationships among related securities | Whether the relationship persists or changes |

| Convertible arbitrage | A convertible security and related instruments, often including the issuer’s shares | Valuation, volatility, financing, liquidity, and hedging |

| ETF arbitrage | An ETF’s market price and the value of its underlying holdings | Access, transaction costs, liquidity, and execution |

Pure arbitrage versus risk arbitrage

In theory, “pure” arbitrage uses offsetting transactions to lock in a price difference without depending on the market’s later direction. In practice, the lock may be imperfect because quotes can change, orders may fill only partly, or settlement may fail.

Risk arbitrage is less certain. Merger arbitrage, for example, depends on a corporate transaction reaching completion. Statistical arbitrage depends on a modeled relationship behaving as expected. These approaches may seek relative-value opportunities, but they still expose the trader to meaningful loss.

The costs and risks behind the spread

Before evaluating any opportunity, separate the visible price difference from the amount that might actually remain after execution.

Transaction costs

The relevant calculation is:

Estimated net result = price difference − all expected costs − allowance for execution uncertainty

Expected costs can include commissions, bid-ask spreads, exchange or platform charges, currency conversion, borrowing costs, transfer fees, and taxes. Some costs are charged directly; others appear through a worse execution price.

A small spread offers little room for error. Even when a calculation looks positive, the opportunity may be available for only a limited quantity. Multiplying the displayed spread by a large position can therefore exaggerate what is realistically executable.

Execution and timing risk

Arbitrage usually requires multiple connected transactions. If one side fills and the other does not, the trader can be left with an unhedged position. During that delay, the price can move in either direction.

Fast-changing quotes create another trap: a screen may show two favorable prices that were not genuinely available at the same instant or in the same size. The difference between a displayed quote and the completed trade is often called slippage.

Liquidity, settlement, and financing risk

An asset may be easy to buy but difficult to sell in sufficient size. Markets can also have different trading hours, settlement rules, account requirements, or transfer restrictions. A strategy that requires short selling or borrowed capital adds availability and financing uncertainty.

The safest-looking arbitrage can fail if the assets are not truly equivalent. Two securities may appear closely related while carrying different rights, tax treatment, credit exposure, redemption terms, or settlement conditions.

Model and event risk

Strategies based on historical relationships assume those relationships remain useful. A structural change can make the old pattern irrelevant. Event-driven strategies add legal, financing, shareholder, and timing uncertainty. Calling these trades “arbitrage” does not remove those risks.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

How technology affects arbitrage

Modern arbitrage is largely an information and execution challenge. Software can monitor many prices, normalize currencies and contract sizes, estimate costs, and send connected orders according to predefined rules. Automation can also enforce position limits and stop trading when data become stale.

Technology does not guarantee an edge. A system is only as dependable as its market data, assumptions, connectivity, and controls. Common failure points include delayed feeds, mismatched timestamps, coding errors, incomplete fills, and a cost model that does not reflect actual trading conditions.

Algorithms also change the competitive environment. When many participants detect the same discrepancy, their buying and selling can narrow it. That makes careful execution at least as important as identifying the difference.

A practical framework for evaluating an opportunity

Beginners can study arbitrage without immediately placing a trade. Use this checklist to test whether an apparent opportunity is economically meaningful:

- Define the relationship. Are the two instruments identical, contractually linked, or merely correlated?

- Confirm executable prices. Check the bid for what you would sell and the ask for what you would buy—not only last-traded prices.

- Match timing and quantity. Verify that both quotes were available at the same time and for the required size.

- List every cost. Include trading, financing, currency, transfer, borrowing, settlement, and tax considerations.

- Map the failure cases. Ask what happens if one order fails, a transfer is delayed, or the relationship widens.

- Check rules and access. Confirm that the transaction, account type, instruments, and markets are available and permitted for you.

- Set a minimum margin of safety. A theoretical remainder that disappears after a small price change is not robust.

- Practice the full workflow. Paper calculations or simulations can reveal missing costs and assumptions without putting capital at risk.

This framework is more valuable than searching for a particular “best” asset class. Opportunities depend on accessible markets, reliable data, costs, speed, liquidity, and the trader’s ability to manage both legs.

Ethics and market impact

Arbitrage is not inherently the same as market manipulation. At a basic level, it responds to inconsistent prices, and the resulting trades may help those prices move closer together. The ETF example described by Investor.gov shows this alignment function directly (Investor.gov).

However, the methods used still matter. Trading must follow the rules governing the relevant market, account, information, and instruments. A strategy should not be assumed lawful merely because it is labeled arbitrage. Anyone considering real transactions should review current broker terms and applicable requirements, and seek qualified professional guidance where necessary.

Key takeaways and next steps

Arbitrage is the attempt to capture a price inconsistency through linked buying and selling. Its economic value comes from the net spread after costs—not the raw difference shown on a screen. Pure arbitrage is an ideal; actual trades can involve execution, liquidity, settlement, financing, event, and model risk.

For a sensible next step, choose one hypothetical example and build a complete cost-and-risk worksheet. Record the two executable prices, time, available quantity, fees, funding assumptions, and what happens if only one side fills. That exercise develops the discipline needed to distinguish a real opportunity from an attractive-looking but incomplete calculation.

Finelo provides financial education for people building their investing knowledge. This article is educational and does not provide personalized financial advice or promise a trading result.

Frequently asked questions

Is arbitrage risk-free?

Arbitrage is sometimes described as risk-free in theory when offsetting transactions lock in a difference. Real execution can introduce costs, partial fills, changing prices, settlement problems, and other risks. Strategies such as merger or statistical arbitrage contain additional uncertainty by design.

Can an individual investor do arbitrage?

An individual may be able to observe or attempt certain relative-price trades, but access does not make them attractive. Professionals may have advantages in data, speed, financing, market access, and operational controls. Beginners should first model the entire transaction and its failure cases rather than focusing only on the displayed spread.

How do transaction costs affect arbitrage profit?

Costs reduce the spread directly. If an apparent difference is $0.40 per unit and total costs are $0.35, only $0.05 remains before taxes or unexpected slippage. If costs or execution prices worsen slightly, the expected gain can disappear.

Does arbitrage eliminate price differences?

Arbitrage trading can push connected prices closer together as participants buy the cheaper side and sell the more expensive side. It does not guarantee permanent equality: prices can diverge again as liquidity, information, costs, and market conditions change.

TradingBeginnerStrategiesMarkets

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Trading

What is Swing Trading? A Complete Guide

Swing trading is a short-term approach in which a trader holds a position for several days or weeks while trying to capture part of a price move. The goal is not to predict every fluctuation. It is to identify a…

Finelo Team

Trading

What is Slippage in Trading?

Slippage in trading is the gap between the price you expected when placing a trade and the price at which it is ultimately executed. The U.S. Securities and Exchange Commission describes price slippage as the…

Finelo Team

Trading

What is Quantitative Trading?

Quantitative trading, often called quant trading, is a method of making trading decisions with data, mathematical models, and predefined rules. A trader develops a hypothesis, translates it into measurable conditions…

Finelo Team