Dividends are taxed based mainly on their classification and the account in which they are held. In a taxable account, ordinary dividends are included in ordinary income, while qualified dividends are eligible for lower capital-gain tax rates. The payer reports the amounts on Form 1099-DIV, according to the IRS. Reinvesting the money usually does not make the dividend disappear for tax purposes, while earnings inside a traditional IRA generally are not taxed until distributed.

How Are Dividends Taxed?

Dividends are taxed based mainly on their classification and the account in which they are held. In a taxable account, ordinary dividends are included in ordinary income, while qualified dividends are eligible for…

7 min read

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Want to learn more?

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

The exact income tax you pay depends on the reported category and your broader tax situation. The practical first step is therefore to identify the dividend type, account type, and relevant tax form—not to apply one general rate to every payment.

Introduction to Dividend Taxation

Companies can pay part of their earnings and profits to shareholders as dividends. For investors, the cash payment is only one part of the picture: the tax classification determines how the income enters the federal return.

This guide is designed for investors reviewing brokerage tax forms, comparing taxable and retirement accounts, or trying to understand why two dividends may not receive identical treatment. It focuses on U.S. federal rules. State treatment may differ, so state-specific questions require current guidance for the relevant jurisdiction.

The basic workflow is:

- Identify the account that received the dividend.

- Review how the payer classified the distribution.

- Check whether holding-period requirements affect qualified treatment.

- Report the amounts using the current filing-year forms.

- Keep records of reinvestments and new share purchases.

This Finelo guide bases its tax explanations on current, directly linked IRS and Investor.gov materials. That evidence-first approach lets readers distinguish official federal rules from general educational context.

Key Takeaways

- Ordinary dividends are included in ordinary income; qualified dividends can receive lower capital-gain rates.

- Form 1099-DIV reports total ordinary dividends and the portion classified as qualified.

- Holding stock for too few days within the relevant window can prevent qualified-dividend treatment.

- Reinvested dividends in a taxable account can still be reportable income.

- Traditional IRA earnings generally are taxed when distributed, rather than as each dividend is paid inside the account.

- Foreign dividends, foreign tax, and Net Investment Income Tax can require additional review.

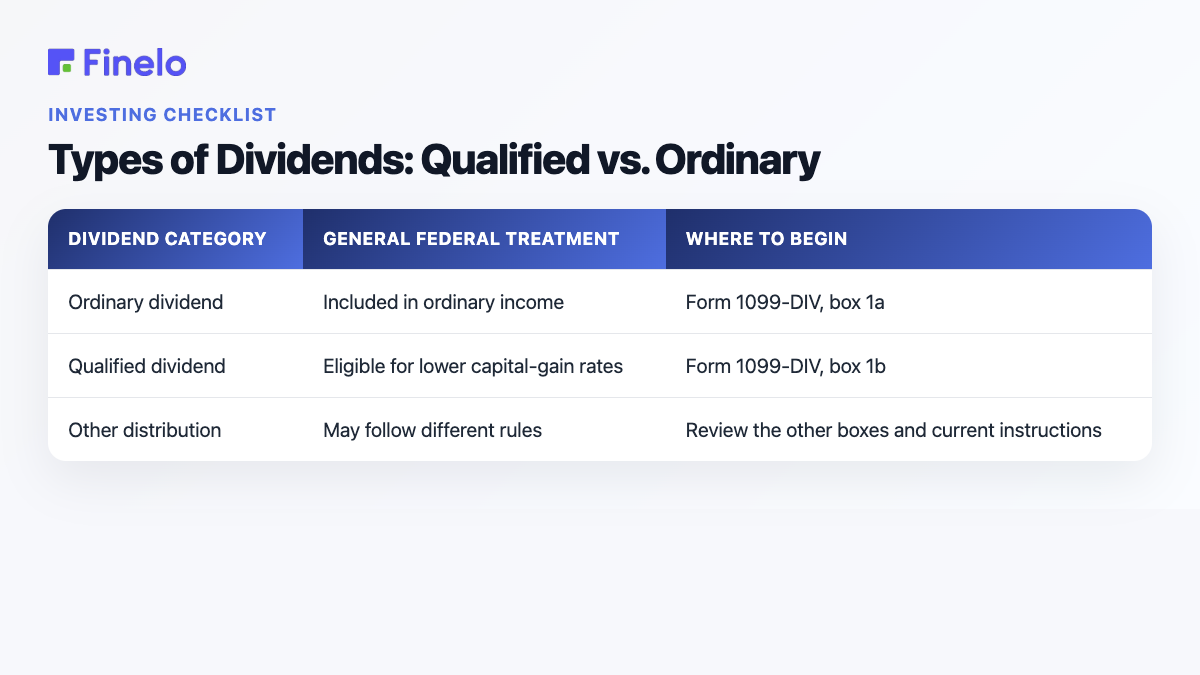

Types of Dividends: Qualified vs. Ordinary

The IRS distinguishes ordinary and qualified dividends. Ordinary dividends are included in ordinary income. Qualified dividends are ordinary dividends that qualify for lower capital-gain rates, and the payer identifies the qualified portion on Form 1099-DIV.

| Dividend category | General federal treatment | Where to begin |

|---|---|---|

| Ordinary dividend | Included in ordinary income | Form 1099-DIV, box 1a |

| Qualified dividend | Eligible for lower capital-gain rates | Form 1099-DIV, box 1b |

| Other distribution | May follow different rules | Review the other boxes and current instructions |

“Qualified” is a tax classification, not a general label for a good company or investment. A payment from a profitable company is not automatically qualified. Likewise, the fact that money appeared as cash in a brokerage account does not establish the correct category.

Foreign dividends require particular care. The IRS instructions state that qualified dividends can be paid by domestic corporations or qualified foreign corporations, subject to the listed exceptions. A foreign company’s payment should therefore not be assumed to qualify merely because it resembles a domestic stock dividend.

The same instructions say foreign tax paid on dividends and other stock distributions is entered in box 7 in U.S. dollars. Review that field and the related country information instead of netting foreign tax against the dividend on your own.

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Tax Rates for Dividends

Ordinary and qualified dividends can produce different federal income tax results. Ordinary dividends are included in ordinary income, while qualified dividends may receive the lower rates used for qualifying capital gains. That makes classification important before estimating what you may owe.

Holding period is one condition that can affect qualified status. The Form 1099-DIV instructions state that dividends on stock held for less than 61 days during the 121-day period beginning 60 days before the ex-dividend date are not qualified dividends.

The ex-dividend date also determines who receives the payment: Investor.gov explains that a buyer who purchases on or after that date does not receive the next dividend, while a buyer who purchases before it does. This is why trade dates matter when reviewing the holding-period window.

Here is a simplified decision example:

- An investor buys stock shortly before the ex-dividend date.

- The company pays a dividend, and the investor then sells the shares.

- If the investor held the stock for too few days within the required window, the dividend may fail the holding-period test.

- The investor should therefore check both Form 1099-DIV and the actual purchase and sale dates before treating the payment as qualified.

This dividend holding-period test should not be confused with the separate rules used to classify gains or losses when shares are sold. A dividend and a later stock sale are different tax events, even though both may involve capital-gain concepts.

Exact rates, thresholds, and the total tax due depend on the filing year and the taxpayer’s full return. Use current instructions rather than a rate table saved or printed for a prior year.

Some investors may also need to consider Net Investment Income Tax separately from the ordinary-versus-qualified calculation. The IRS includes dividends among the types of net investment income. Whether the additional tax applies depends on the taxpayer’s complete situation, so dividend rate estimates should not be treated as the final tax bill.

Tax Implications in Tax-Advantaged Accounts

Account location changes the timing analysis. The IRS says that amounts in a traditional IRA, including earnings, generally are not taxed until distributed. That means a dividend earned within a traditional IRA is not handled in the same way as a dividend paid into a regular taxable brokerage account.

This does not mean retirement-account money is never subject to tax. It means the account’s distribution rules generally determine when traditional IRA earnings enter the tax picture. Investors should distinguish between:

- a company paying a dividend inside the account;

- reinvesting or holding that money inside the account; and

- withdrawing or receiving a distribution from the account.

Other retirement accounts can have different contribution and distribution rules. Confirm the account type before applying any general statement about IRAs, employer plans, or tax-free withdrawals.

Reporting Dividends: What You Need to Know

Form 1099-DIV is the central reporting document for many investors. The payer identifies total ordinary dividends and the portion treated as qualified. Those figures are related: the qualified amount is a portion of the ordinary-dividend total, not a second dividend to add again.

For federal filing, the IRS instructs taxpayers to enter ordinary dividends from box 1a on line 3b of Form 1040 or Form 1040-SR and qualified dividends from box 1b on line 3a. Nonresident filers should follow the applicable Form 1040-NR instructions.

Use this filing checklist:

- Gather each Form 1099-DIV, including corrected forms.

- Match every form to its payer and account.

- Review boxes 1a and 1b without adding box 1b twice.

- Check other populated boxes and attached instructions.

- Compare the forms with year-end account statements.

- Retain purchase, sale, ex-dividend, and reinvestment records.

- Use current federal and state instructions for the filing year.

For example, someone filing in 2026 should confirm that the forms and instructions apply to the tax year being reported rather than relying on a document printed for a different year.

Dividend reinvestment plans, or DRIPs, are a frequent source of confusion. When dividends are reinvested at fair market value to buy additional shares, the IRS says the dividends must still be reported as income. Reinvestment changes what happens to the money; it does not automatically erase the dividend.

Those new shares also need records. Track the date, amount reinvested, number of shares acquired, and purchase value because the information may matter when the shares are eventually sold.

Conclusion and Practical Next Steps

To understand how your dividends are taxed, first separate ordinary from qualified amounts, verify the account type, and check whether the holding-period rule applies. Then reconcile Form 1099-DIV with your records and use the current filing-year instructions. Pay special attention to reinvested dividends, foreign-company payments, and corrected forms.

If the classification, retirement-account distribution, or state treatment remains unclear, consult the payer or a qualified tax professional. For more educational material on investing concepts, explore Finelo. This article is general education, not personalized tax or investment advice.

Frequently asked questions

Are dividends taxed if I do not withdraw the cash?

In a taxable account, leaving cash in the account does not by itself change the dividend classification. If the dividend is automatically reinvested at fair market value, the IRS still requires it to be reported as income along with other ordinary dividends.

How do I know whether a dividend is qualified?

Start with box 1b of Form 1099-DIV, then check whether you met the applicable requirements, including the holding-period rule. Contact the payer if the form appears inconsistent with your records rather than changing the classification based on an assumption.

Are dividends and capital gains the same?

No. A dividend is a distribution paid to a shareholder, while a gain can arise when an investment is sold for more than its relevant basis. Qualified dividends may use lower capital-gain tax rates, but that does not turn the dividend payment into proceeds from a stock sale.

Do states tax dividends?

State rules can differ from federal rules and from one state to another. Check current instructions for every state in which you must file, particularly if you moved during the year or are subject to tax in multiple jurisdictions.

InvestingBeginnerDividendsTaxesMarkets

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Investing

Working Capital: What It Tells Investors About Liquidity

Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day…

Finelo Team

Investing

What is Venture Capital?

Venture capital (VC) is money invested in young businesses in exchange for equity, or an ownership stake. It is generally aimed at startups and early-stage companies that need capital to develop a product, hire people…

Finelo Team

Investing

What Is the S&P 500? A Complete Overview

The S&P 500 is a stock market index designed to show how a broad group of leading large-cap U.S. companies is performing. Rather than checking hundreds of stocks individually, investors can look at the index for a…

Finelo Team