To open a brokerage account, choose a brokerage firm and select an account type. Then complete the application, verify your identity, connect a funding source, and decide how to invest the money. Before you apply, compare fees, investment choices, service, security, and the treatment of uninvested cash.

How to Open a Brokerage Account: A Complete Guide

To open a brokerage account, choose a brokerage firm and select an account type. Then complete the application, verify your identity, connect a funding source, and decide how to invest the money. Before you apply…

10 min read

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Want to learn more?

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

Most applications ask for personal, financial, and tax-identification information because brokers must meet legal and regulatory requirements, according to Investor.gov. Preparing that information first can make the process smoother. Opening the account is only the administrative step; choosing suitable investments and understanding their risks requires a separate decision.

What Is a Brokerage Account?

A brokerage account is an account used to hold cash and investments and to place buy or sell orders. Unlike a bank account designed mainly for spending and saving, it provides access to investments offered by the brokerage.

Brokerage accounts can serve different purposes. You might use one for a long-term goal or to invest outside a workplace plan. The right structure depends on who will own the account, how you will use it, and whether you want the option to borrow.

Opening an account does not automatically invest your deposit. You still need to choose investments or enroll in a managed service. Fidelity describes the broad sequence as completing an application and then funding the account. It also outlines self-directed, professionally managed, and automated service models (Fidelity).

What You Need to Open a Brokerage Account

Gathering your information before beginning helps prevent interruptions, expired application sessions, and mismatched details.

Personal and identification information

A brokerage application may request:

- Your legal name

- Residential and mailing addresses

- Date of birth

- Phone number and email address

- Social Security number or another tax-identification number

- Details from a passport, driver’s license, or other government-issued identification

- Citizenship or residency information

- Employment and occupation information

The exact list varies by firm and applicant. The key is consistency: enter your name, address, and identification details exactly as they appear on your documents.

Financial profile

The application may also ask about:

- Annual income and approximate net worth

- Employment status

- Investment experience

- Existing investments

- Investment objectives

- Time horizon and liquidity needs, meaning when you need access to the money

- Risk tolerance

These questions are not a test of whether you are “good enough” to invest. Answer them accurately. Your goal is to give the firm a truthful picture of your situation and avoid selecting an objective merely because it sounds more ambitious.

Banking details

If you plan to fund the account electronically, have the details for the bank account you intend to connect. Check that the ownership names are compatible and review the brokerage’s instructions before initiating a transfer.

Choose the Right Account and Service Model

The phrase “brokerage account” covers several decisions. Separate them so that a convenient application flow does not steer you into an unsuitable structure.

Cash account or margin account?

Investor.gov identifies cash and margin as the two account types brokerage firms generally offer.

In a cash account, you pay for purchases with available funds. In a margin account, you can borrow from the brokerage and use securities in the account as collateral. You pay interest, and larger losses are possible (Investor.gov). Margin is not simply a more advanced cash account.

Current rules also matter. FINRA says firms generally monitor margin-account equity during the trading day under intraday margin requirements that took effect on June 4, 2026 (FINRA). If you do not understand the loan agreement or what happens when the account falls short, do not enable margin.

Individual, joint, or another ownership structure?

An individual account has one owner. A joint account has multiple owners. Other structures may be available for retirement, custodial, trust, business, or estate purposes.

Ownership affects control, access, and tax reporting, so select it deliberately. For example, opening an individual account now and assuming another person can simply be “added later” may create avoidable administrative or legal complications. If ownership has meaningful tax or estate consequences, consider obtaining qualified professional guidance.

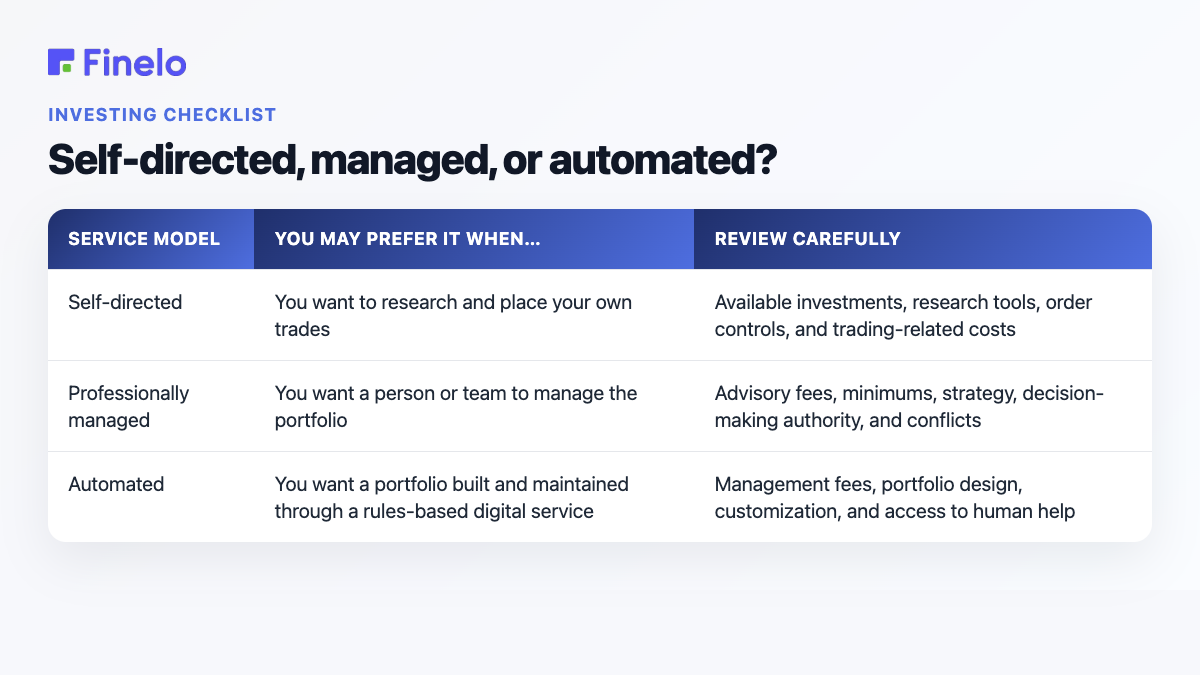

Self-directed, managed, or automated?

Choose how much responsibility you want for portfolio decisions:

| Service model | You may prefer it when… | Review carefully |

|---|---|---|

| Self-directed | You want to research and place your own trades | Available investments, research tools, order controls, and trading-related costs |

| Professionally managed | You want a person or team to manage the portfolio | Advisory fees, minimums, strategy, decision-making authority, and conflicts |

| Automated | You want a portfolio built and maintained through a rules-based digital service | Management fees, portfolio design, customization, and access to human help |

No model is automatically best. A beginner who wants guidance may value support, while an experienced investor may prioritize control. Compare the complete service, not just the account-opening promotion.

How to Compare Brokerage Firms

Because pricing and offerings change, use the firms’ current public disclosures and account agreements rather than relying on an old comparison chart.

Score each candidate against the same questions:

| Decision area | What to check | Why it matters |

|---|---|---|

| Eligibility | Residency, citizenship, age, and account-type rules | A firm may not accept every applicant or ownership structure |

| Total cost | Maintenance, advisory, trading, transfer, closure, and service fees | A “no commission” claim does not describe every possible cost |

| Investment access | Whether it offers the stocks, bonds, mutual funds, or other securities you plan to use | The account must support the portfolio you intend to build |

| Minimums | Opening, investment, and managed-service minimums | Different thresholds may apply at different stages |

| Uninvested cash | Where cash is held and what choices you have | Deposited money may remain uninvested until you act |

| Support | Service channels and availability | Help can matter during verification, transfers, or account restrictions |

| Security | Sign-in protections and fraud-response procedures | Strong account hygiene reduces avoidable exposure |

| Transfers and closure | Process, timing, limitations, and costs | Future portability matters even when you plan to stay |

Read the brokerage’s relationship summary, fee schedule, and account agreement before applying. Investor.gov says maintenance fees may be monthly, quarterly, or annual, may depend on an account threshold, and do not apply to every account. It also notes that firms may charge wire or transfer fees (Investor.gov). Save the documents you accept. Ask the firm to explain unclear fees before you fund the account.

Step-by-Step: How to Open a Brokerage Account

1. Define the account’s job

Write down the goal, approximate timeline, and whether you may need quick access to the money. A near-term expense and a decades-away goal should not be treated as the same problem.

Investor.gov notes that new-account applications may ask about objectives and risk tolerance, using terms such as capital preservation, income, growth, aggressive growth, or speculation. It also advises considering when you may need fast access to the funds (Investor.gov).

2. Select the account type and ownership

Decide among cash and margin, then choose the correct ownership structure. Do not opt into borrowing features merely because they are preselected or presented as convenient.

3. Compare a short list of firms

Use the framework above to compare two or three firms on the factors that matter to your goal. Check current official pages and documents on the same day so the comparison is internally consistent.

4. Complete the application

Apply online or through an available representative. Enter accurate details, read each disclosure, and note any optional features. Avoid guessing about financial information; use reasonable, truthful estimates where the form asks for approximate amounts.

5. Complete identity verification

The brokerage may verify the information electronically or request additional documents. A mismatch, an unreadable image, a recent address change, or incomplete tax information can slow the review.

6. Review the account before accepting

Confirm:

- The account owner and account type are correct

- You selected cash or margin intentionally

- Optional services match your choices

- Beneficiary or trusted-contact fields are complete if you chose to provide them

- You understand the main fees and how uninvested cash is handled

- Your contact information is accurate

7. Fund the account

Choose a supported funding method and follow the brokerage’s instructions. Before transferring a large amount, consider testing the connection with a smaller transfer if the firm permits it.

Funding and investing are separate actions. Confirm that transferred cash has arrived and is available, then make an investment decision based on your plan. Do not assume the brokerage automatically invests every deposit.

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Funding the Account Without Losing Track of the Cash

The opening deposit should fit both the brokerage’s rules and your own plan. A minimum required to open an account, if any, may differ from the amount needed to buy a particular investment or qualify for a managed service.

Before transferring money, ask:

- Is there an opening minimum?

- Is there a separate minimum for the investment or service I want?

- When will the transfer become available?

- Where will cash sit before it is invested?

- Do I need to place an order after the transfer?

- Are there restrictions or costs for moving money back out?

Keep an emergency reserve separate from money intended for investing. Market investments can fluctuate, so money needed on a fixed short timeline may require a different home.

Verification, Approval, and Application Problems

Approval time varies by firm, application, and verification needs. A straightforward application may move quickly, but there is no universal approval deadline. Build in extra time if you recently moved, have an identity document that is close to expiring, are applying under a business or trust, or need to provide nonstandard tax or residency documents.

If the application is delayed:

- Check your email and application portal for a document request.

- Confirm that your legal name, date of birth, address, and tax number match your records.

- Submit clear, complete documents through the firm’s approved channel.

- Contact the brokerage and ask what specific item remains unresolved.

- Keep a record of what you sent and when.

If the firm declines the application, ask whether it can explain the reason and whether corrected information can be resubmitted. Do not alter truthful information simply to obtain approval. Another brokerage may have different eligibility rules, but you should still disclose all requested information accurately.

Common Mistakes to Avoid

Choosing Based on One Promoted Feature

A promotional rate or commission claim is only one part of the decision. Compare the full cost, investment menu, cash treatment, support, and exit process.

Enabling margin without understanding it

Borrowing can magnify losses as well as gains and may trigger account requirements at difficult moments. Read the margin agreement and ask for clarification before accepting it.

Funding before making an investment plan

Depositing money without deciding what happens next can leave cash idle or encourage an impulsive trade. Decide how you will divide the money among investments first, even if your first step is simply taking time to learn.

Choosing the wrong owner or account type

Ownership is not a cosmetic setting. Verify the account owner, tax status, and intended purpose before submission.

Ignoring small or occasional fees

Maintenance, advisory, transfer, closure, paper statement, or assisted-service charges may matter depending on how you use the account. Review the current fee schedule rather than assuming “free” means every service costs nothing.

Treating the risk questionnaire as a formality

Your objective should reflect when you need the money, how quickly you may need access to it, and how much loss you can tolerate. Selecting the most aggressive label does not improve expected outcomes. It can create a mismatch between the account profile and your needs.

A Simple Pre-Submission Checklist

Before clicking “submit,” make sure you can answer yes to each item:

- I know what goal this account serves.

- I selected the ownership structure intentionally.

- I understand whether this is a cash or margin account.

- I compared current costs and service documents.

- My identity, contact, tax, and financial information is accurate.

- I know how deposits are handled before they are invested.

- I know what I plan to do after the money arrives.

- I saved the disclosures and agreements I accepted.

This checklist is especially useful for first-time investors, but it also helps anyone opening an additional account for a new goal.

Next Steps

Opening a brokerage account is a sequence of decisions, not just an online form. Define the goal, choose an account structure, compare current official disclosures, prepare accurate documents, complete verification, and fund the account only after you understand what happens to the cash.

Then pause before making the first investment. Review the investment’s risks, costs, time horizon, and fit with your plan. Finelo provides financial education for people building their investing knowledge, but educational material is not personalized financial advice. When tax, legal, or suitability questions are significant, consider consulting an appropriately qualified professional.

Frequently asked questions

What documents do I need to open a brokerage account?

Be prepared with government-issued identification and your tax-identification information, plus accurate contact, employment, and financial details. The precise documents depend on the brokerage and your circumstances. Nonstandard ownership, residency, or tax situations may require additional documentation.

How long does brokerage-account approval take?

There is no single timeline for every firm or applicant. Applications that can be verified electronically may be processed more quickly, while mismatched information or additional document requests can extend the review. Check the firm’s current estimate and respond promptly to requests.

Can I open a brokerage account if I am not a U.S. citizen?

Possibly, but eligibility depends on the brokerage, your country of residence, the account type, and the documentation the firm can accept. Review the firm’s current eligibility rules before applying and expect to provide accurate residency and tax information.

What fees can a brokerage account have?

Potential costs can relate to account maintenance, advice or management, trades, certain investments, transfers, closure, statements, or representative-assisted services. Not every firm charges every fee. Review the current fee schedule and calculate costs based on how you expect to use the account.

InvestingBeginnerGetting StartedMarkets

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Investing

Working Capital: What It Tells Investors About Liquidity

Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day…

Finelo Team

Investing

What is Venture Capital?

Venture capital (VC) is money invested in young businesses in exchange for equity, or an ownership stake. It is generally aimed at startups and early-stage companies that need capital to develop a product, hire people…

Finelo Team

Investing

What Is the S&P 500? A Complete Overview

The S&P 500 is a stock market index designed to show how a broad group of leading large-cap U.S. companies is performing. Rather than checking hundreds of stocks individually, investors can look at the index for a…

Finelo Team