The central difference between a pension and a 401(k) is what the plan promises. A traditional pension generally promises a retirement benefit defined by the plan, while a 401(k) builds an individual account whose eventual value depends on contributions, investment choices, and what happens to those investments. A pension may suit someone who values predictable income and expects to remain with an employer long enough to earn the benefit. A 401(k) may suit someone who wants more control and portability. If your employer offers both, using both may provide a useful mix of predictable benefits and personal savings.

Pension vs 401(k): A Comprehensive Comparison

The central difference between a pension and a 401(k) is what the plan promises. A traditional pension generally promises a retirement benefit defined by the plan, while a 401(k) builds an individual account whose…

7 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

This comparison is for employees reviewing workplace benefits, people changing jobs, and anyone deciding which plan should play the larger retirement role. Your next step is to collect the vesting, contribution, benefit, fee, and distribution details for the plans actually available to you, then use the decision table below.

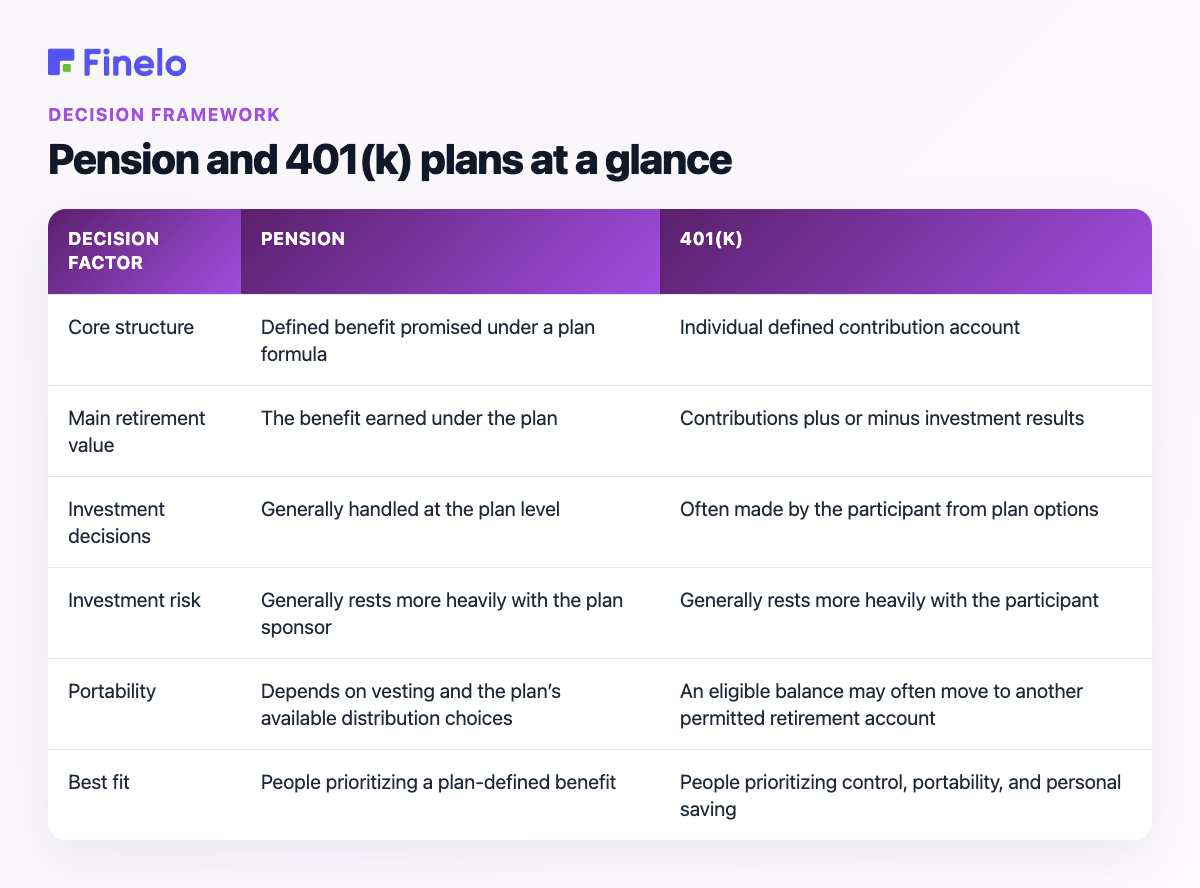

Pension and 401(k) plans at a glance

The IRS describes a defined benefit plan as a pension plan that pays the retirement benefit stated in the plan. That makes the benefit formula—not a personal investment balance—the defining feature of a traditional pension. See the IRS description of employer retirement-plan coverage.

A 401(k), by contrast, is an account-based workplace plan. The employee usually decides how much to contribute and how to allocate the money among the choices available in the plan. The employer may also contribute, depending on the plan’s terms.

| Decision factor | Pension | 401(k) |

|---|---|---|

| Core structure | Defined benefit promised under a plan formula | Individual defined contribution account |

| Main retirement value | The benefit earned under the plan | Contributions plus or minus investment results |

| Investment decisions | Generally handled at the plan level | Often made by the participant from plan options |

| Investment risk | Generally rests more heavily with the plan sponsor | Generally rests more heavily with the participant |

| Portability | Depends on vesting and the plan’s available distribution choices | An eligible balance may often move to another permitted retirement account |

| Best fit | People prioritizing a plan-defined benefit | People prioritizing control, portability, and personal saving |

Consider two workers. Maya expects to stay with one employer for much of her career and values knowing how her benefit will be calculated. A pension may be especially valuable to her. Jordan changes employers more frequently and wants to keep building retirement assets across jobs. A 401(k) may fit that work pattern better. Neither plan is universally superior; the stronger fit depends on the actual plan rules and the worker’s priorities.

How each plan shapes retirement security

What a pension does well

A pension converts years of eligible service under the plan into a defined retirement benefit. Its appeal is clarity: instead of asking how large an investment account might become, the participant can focus on the benefit formula and the requirements for earning it.

The tradeoff is that the details are controlled by the plan. Vesting, the benefit formula, retirement dates, survivor choices, and what happens after leaving employment can materially affect the value to a particular worker. Someone comparing job offers should therefore look beyond the word “pension” and read the plan’s summary and benefit estimate.

Example: Elena is comparing two positions. One has a pension, but she is uncertain whether she will stay long enough to become vested. The other has a 401(k) that she can begin funding from her paycheck. Her decision should account for her likely tenure, not merely which benefit sounds more generous.

What a 401(k) does well

A 401(k) gives the participant an identifiable retirement account and typically more responsibility for funding and investing it. That flexibility can be useful, but it also creates decisions: how much to save, which investments to select, how to respond to market changes, and how to manage the account when changing jobs.

Portability is a practical advantage when a receiving plan permits a transfer. Fidelity documents that old 401(k) assets may be consolidated into a new workplace retirement account, including a self-employed 401k, when allowed. Review Fidelity’s discussion of old retirement-plan options.

Example: Marcus leaves an employer with a 401(k). Instead of treating the balance as spendable cash, he reviews the choices permitted by the old plan and any new retirement plan. His goal is to preserve the account’s retirement purpose while comparing investment choices, fees, and convenience.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Taxes, withdrawals, and changing jobs

Taxes should be evaluated from the documents for the specific plan and the type of contribution involved. Pension payments and 401(k) withdrawals can create taxable income, but the result may differ depending on how money entered the plan, the form of distribution, the participant’s circumstances, and current tax rules. A Roth feature, after-tax contributions, a rollover, or an early distribution can change the analysis.

The practical lesson is to avoid making a withdrawal decision from the plan name alone. Before taking money out:

- Identify whether the money is pre-tax, after-tax, or associated with a Roth feature.

- Ask the plan administrator which distribution and rollover choices are available.

- Compare the immediate tax cost with the effect of removing money from retirement savings.

- Confirm the current rules with an appropriate tax professional when the amount or decision is significant.

Changing jobs also does not automatically mean that a pension becomes a 401(k). These are different plan structures. A former employee may retain an earned pension benefit under the pension’s rules, while separately deciding what to do with a 401(k) balance. If a pension offers a lump-sum choice, the decision between keeping a future plan benefit and moving an eligible amount deserves careful review; it should not be treated as a routine account transfer.

Example: Priya leaves a company that provided both plans. She first asks for a pension benefit statement and confirms whether she is vested. Separately, she reviews the permitted options for her 401(k). Keeping the decisions separate helps her avoid assuming that the same rules apply to both benefits.

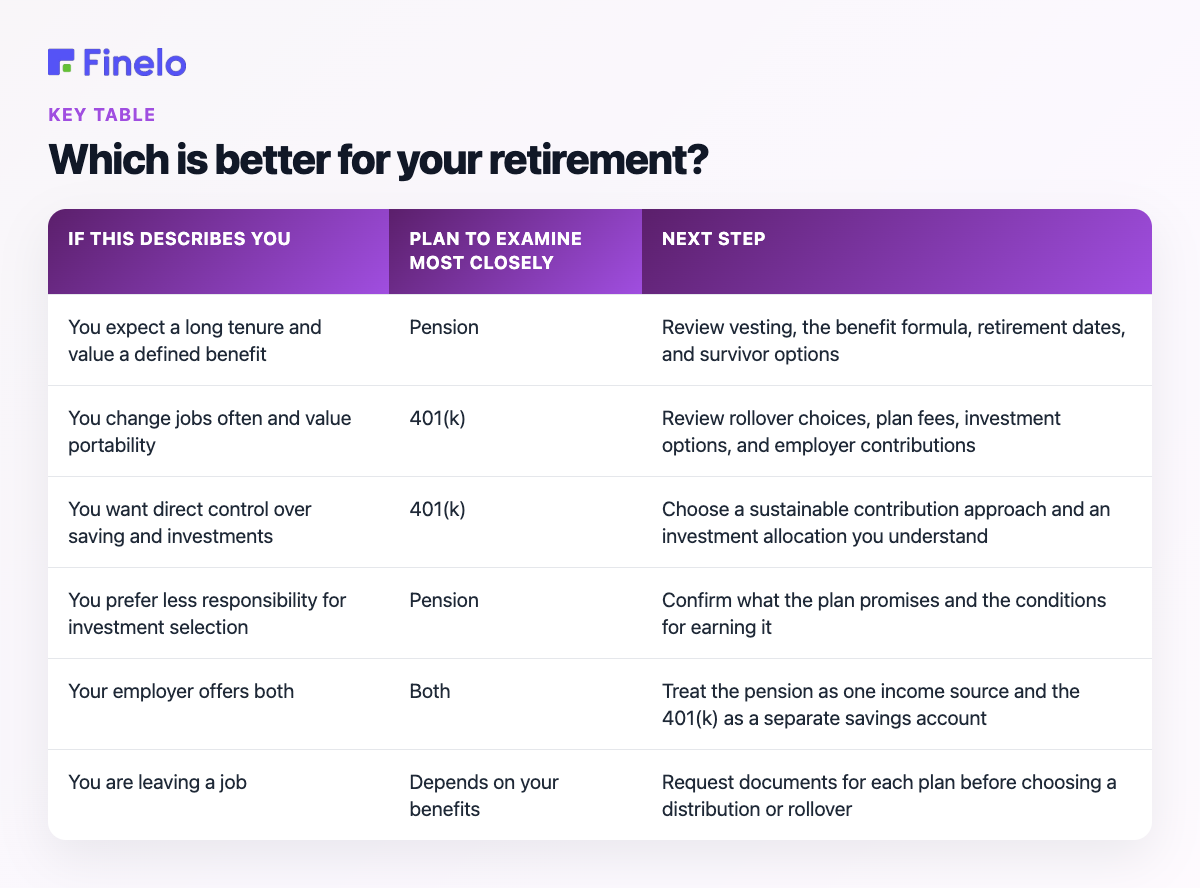

Which is better for your retirement?

The better plan is the one that best complements your employment path, need for predictability, willingness to manage investments, and other retirement resources. Use the following decision framework:

| If this describes you | Plan to examine most closely | Next step |

|---|---|---|

| You expect a long tenure and value a defined benefit | Pension | Review vesting, the benefit formula, retirement dates, and survivor options |

| You change jobs often and value portability | 401(k) | Review rollover choices, plan fees, investment options, and employer contributions |

| You want direct control over saving and investments | 401(k) | Choose a sustainable contribution approach and an investment allocation you understand |

| You prefer less responsibility for investment selection | Pension | Confirm what the plan promises and the conditions for earning it |

| Your employer offers both | Both | Treat the pension as one income source and the 401(k) as a separate savings account |

| You are leaving a job | Depends on your benefits | Request documents for each plan before choosing a distribution or rollover |

Long-term implications matter. A pension can reduce uncertainty about how a portion of retirement income is determined, but its value may depend heavily on staying long enough to vest and qualify under the formula. A 401(k) can follow a more mobile career, but the participant must save consistently and manage investment risk. Inflation also matters: a fixed payment can lose purchasing power over time, while an invested account can fluctuate and may lose value. The relevant question is not simply “Which plan pays more?” but “Which risks am I taking, and which risks is the plan taking?”

For many workers, the answer is not pension or 401(k). If both are available, they can serve different roles. The pension may form a plan-defined base, while the 401(k) adds personally funded assets and flexibility. Availability, eligibility, and contribution decisions remain governed by each employer’s plan.

Questions to ask before deciding

Ask the employer or plan administrator for the documents and estimates needed to compare the real benefits:

- When do I become vested in employer-funded benefits?

- How is the pension benefit calculated?

- What contribution choices and employer contributions apply to the 401(k)?

- Who chooses and bears the risk of the investments?

- What fees or plan expenses affect the account or benefit?

- What happens to each benefit if I leave this year?

- Which payment, survivor, rollover, or distribution options are available?

- How would each plan fit with my other retirement income and savings?

Finelo’s role here is educational: the comparison organizes the decisions a beginner should investigate, while the linked first-party sources support the core plan distinctions. Your employer’s plan documents remain the controlling source for your own benefits.

Frequently asked questions

Can I have both a pension and a 401(k)?

Potentially, yes. An employer may offer more than one retirement plan, or a worker may accumulate different benefits across employers. Eligibility and participation depend on the terms of each plan. If you have both, evaluate them separately rather than assuming contributions, vesting, taxes, or distribution choices work the same way.

What happens to my pension if I leave my job?

It depends on whether you are vested and what the plan allows. Ask for a current benefit statement and the plan’s description of benefits after separation. Do not assume that leaving automatically erases the benefit or makes it transferable to a 401(k).

Should I choose a pension or a 401(k) in a job offer?

Compare the entire compensation package and the benefits you are realistically likely to earn. A pension may carry less value for someone who expects a short stay, while a 401(k) may require meaningful employee contributions to reach its potential. Salary, health coverage, vesting, employer contributions, fees, flexibility, and career fit all belong in the comparison.

What should I do next?

Collect the summary plan description, vesting schedule, pension estimate, 401(k) contribution details, investment menu, and distribution rules. Then compare the benefits using your expected tenure and retirement priorities. For a high-value or irreversible tax decision, consider obtaining qualified financial or tax guidance before acting.

Financial LiteracyBeginnerRetirementPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team