A 529 plan is an education-focused account with tax advantages. It is operated by a state or educational institution and is intended to help pay eligible costs for a designated beneficiary, such as a child, grandchild, or even the account owner. The IRS describes 529 plans as a way to save for college, other post-secondary training, and certain elementary or secondary school tuition.

What Is a 529 Plan? Pricing, Plans, and Value

A 529 plan is an education-focused account with tax advantages. It is operated by a state or educational institution and is intended to help pay eligible costs for a designated beneficiary, such as a child, grandchild…

7 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

The key decision is not simply whether to open one. It is which type of 529 plan fits the goal, what the plan charges, which tax benefits apply, and how much flexibility the family needs.

How a 529 Plan Works

A 529 plan separates two roles:

- The account owner opens and controls the account.

- The beneficiary is the person whose education expenses the money is intended to cover.

The owner contributes money and selects from the choices offered by the plan. In a savings plan, the account’s value can change with its underlying investments. A prepaid tuition plan works differently: its purpose is to address future tuition through the terms established by that plan.

Control is an important feature. Unlike a custodial account, the owner of a 529 plan retains ownership until money is withdrawn, according to Fidelity’s explanation of 529 plans. This can matter to parents or grandparents who want to set money aside without immediately transferring control to the beneficiary.

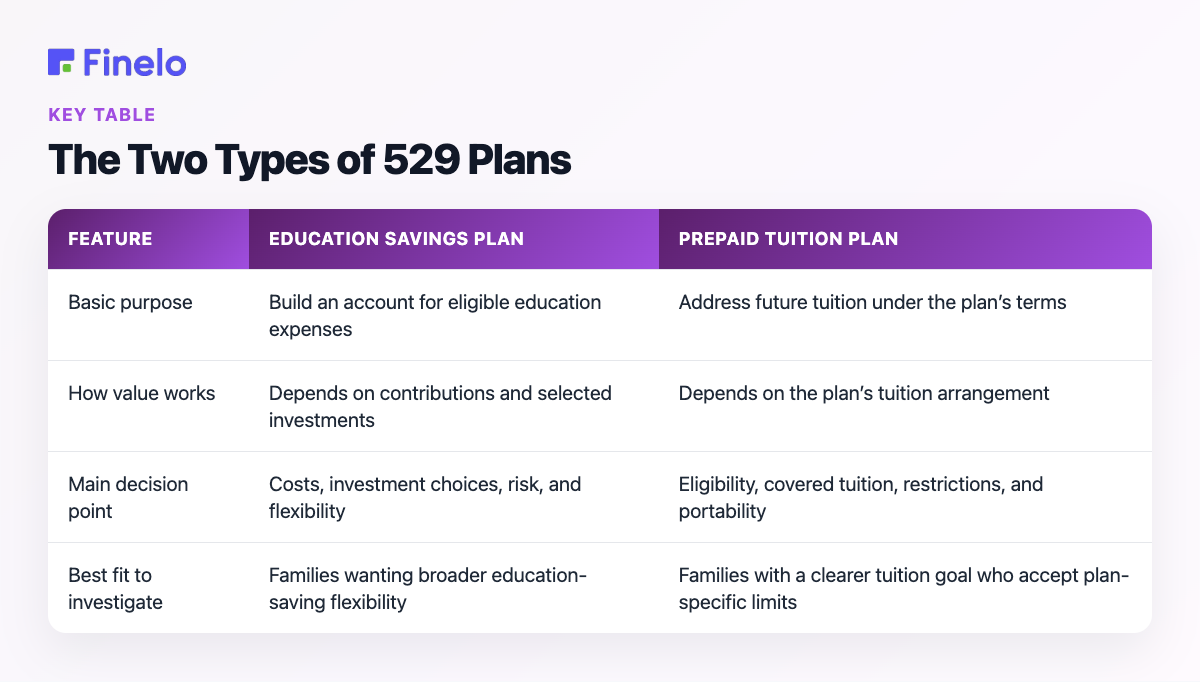

The Two Types of 529 Plans

The IRS identifies two basic types: savings plans and prepaid tuition plans. States may offer either or both, while a qualified educational institution can offer only the prepaid tuition type.

| Feature | Education savings plan | Prepaid tuition plan |

|---|---|---|

| Basic purpose | Build an account for eligible education expenses | Address future tuition under the plan’s terms |

| How value works | Depends on contributions and selected investments | Depends on the plan’s tuition arrangement |

| Main decision point | Costs, investment choices, risk, and flexibility | Eligibility, covered tuition, restrictions, and portability |

| Best fit to investigate | Families wanting broader education-saving flexibility | Families with a clearer tuition goal who accept plan-specific limits |

Neither type is universally better. A savings plan may be more practical when the beneficiary’s future school is uncertain. A prepaid plan may be worth considering when its covered institutions and restrictions closely match the family’s plans.

Before choosing, read the plan documents rather than relying on the plan name alone. Each state’s plan is somewhat unique, so two plans in the same category can still differ substantially.

Tax Advantages and Their Limits

The central value of a 529 plan is its tax treatment. While money remains in the account, income tax is not due on its earnings. Withdrawals used for qualified education expenses may be free from federal income tax and, in many cases, state tax as well, as summarized by Fidelity.

That does not mean every contribution or withdrawal receives the same treatment. Tax outcomes depend on how the money is used and may also depend on state rules. A plan should therefore be evaluated on two levels:

- Federal treatment: Determine whether the planned expense qualifies.

- State treatment: Check whether the state offers an incentive and what conditions apply.

An in-state plan should not be selected automatically. The SEC’s investor education guidance says families should also research out-of-state plans because lower costs may outweigh an in-state plan’s tax incentives or other benefits. The useful comparison is therefore net value after fees, restrictions, and applicable tax benefits, not the advertised benefit by itself.

Qualified and Non-Qualified Expenses

A qualified expense is an education cost that meets the rules for tax-advantaged treatment. The IRS definition of a 529 plan covers college and other post-secondary training as well as certain tuition connected with attendance at an elementary or secondary public, private, or religious school.

The distinction matters because using money outside the qualified rules can change its tax treatment. Before withdrawing, match the expense to current plan and tax guidance, retain relevant records, and avoid assuming that every school-related purchase qualifies.

A practical withdrawal checklist is:

- Confirm that the beneficiary and educational institution match the applicable requirements.

- Verify that the specific expense is eligible.

- Review the timing and amount of the withdrawal.

- Keep bills, receipts, and account records together.

- Check both federal and state implications when uncertain.

This is an area where precise circumstances matter. General education cannot replace advice from a qualified tax professional who can review an individual situation.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

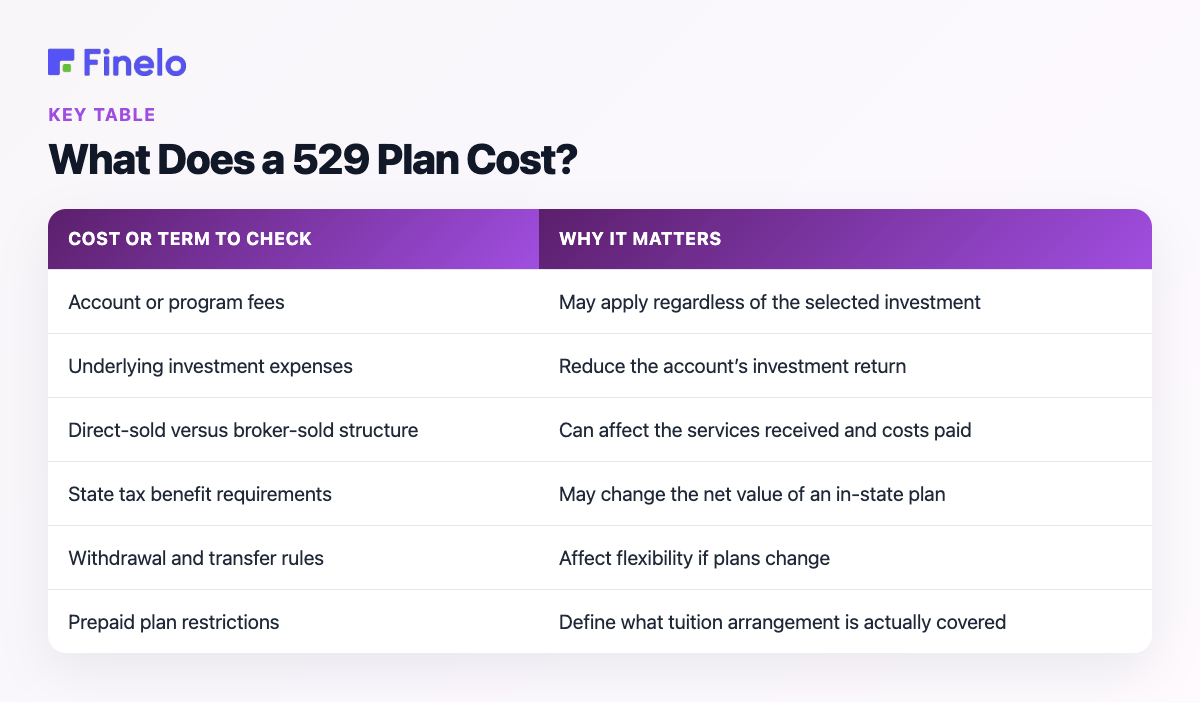

What Does a 529 Plan Cost?

There is no single price for a 529 plan. Fees and expenses vary by plan type, whether a plan is sold directly or through a broker, the plan itself, and its underlying investments. These charges reduce returns, so they should be part of the decision from the start.

Use the plan’s offering circular to build a fee comparison:

| Cost or term to check | Why it matters |

|---|---|

| Account or program fees | May apply regardless of the selected investment |

| Underlying investment expenses | Reduce the account’s investment return |

| Direct-sold versus broker-sold structure | Can affect the services received and costs paid |

| State tax benefit requirements | May change the net value of an in-state plan |

| Withdrawal and transfer rules | Affect flexibility if plans change |

| Prepaid plan restrictions | Define what tuition arrangement is actually covered |

The SEC’s 529 plan guidance specifically recommends reviewing the offering circular to understand charges for both the plan and each investment option.

Avoid comparing plans on fees alone. A low-cost plan may still be a poor fit if its choices, restrictions, or state treatment do not suit the intended use. Conversely, a state benefit does not automatically compensate for materially higher ongoing costs. Compare the complete arrangement.

How to Choose and Open a 529 Plan

Start with the education goal, not the provider. The following process keeps the comparison focused:

- Name the beneficiary and likely time horizon. A shorter horizon generally leaves less room to recover from investment declines.

- Choose the plan type to investigate. Decide whether flexibility or a defined tuition arrangement is more important.

- Compare the home-state plan with alternatives. Include costs, state incentives, restrictions, and available choices.

- Read the official plan documents. Review fees, risks, contribution rules, withdrawal terms, and investment information.

- Choose an investment approach that matches the timeline and risk tolerance. Do not select solely from past performance or an assumed return.

- Gather the required identity and beneficiary details. The specific application requirements come from the selected plan.

- Set a contribution approach that fits the household budget. Education saving should be considered alongside other financial priorities.

Fidelity states that its 529 accounts have no income restrictions. Its eligibility information also says an adult U.S. resident opening an account needs domestic contact details plus an accepted taxpayer-identification number. Treat those as provider-specific opening details and confirm the requirements of the plan you actually choose.

Who May Benefit—and Who Should Pause

A 529 plan may be worth investigating for parents, grandparents, other relatives, or individuals saving for their own eligible education. It can be especially relevant when the saver values tax-advantaged growth, wants to retain control of the account, and expects the money to be used for qualified costs.

Pause before opening one if the education goal is unclear, the money may be needed for unrelated near-term expenses, or the plan’s fees and restrictions have not been reviewed. Because savings-plan investments can involve risk, a 529 plan should not be treated as a guaranteed return or a guaranteed solution to future education costs.

Finelo provides financial education for people building their investing knowledge. Use that education to understand terms and tradeoffs, then verify the selected 529 plan’s current official documents before acting.

Product, Course, App, and Platform Experience

An educational product can help a beginner learn the vocabulary behind 529 plans, but the learning experience and the 529 plan itself should be evaluated separately. A course or app does not replace the selected plan’s official offering circular, tax information, or account agreement.

When using a financial education platform, look for explanations that distinguish facts from examples, describe risk without promising outcomes, and encourage comparison of costs and restrictions. Then apply what you learn to the official documents for each plan under consideration. That two-step approach—learn the concepts, then verify the product—reduces the risk of choosing from a simplified summary alone.

Next Steps

A 529 plan is best understood as a tax-advantaged education tool, not a single standardized product. Decide which type fits the goal, compare in-state and out-of-state alternatives, examine every layer of fees, and confirm how intended withdrawals will be treated.

Use official offering documents to narrow the options, then consult a qualified tax or financial professional if the decision depends on personal tax treatment, financial aid, or broader household planning. This content is educational and is not personalized financial advice.

Frequently asked questions

Can the beneficiary be changed?

The account owner controls the plan, but beneficiary-change rules and tax consequences depend on the applicable requirements. Review the selected plan’s official documents and current tax guidance before making a change.

What if the beneficiary does not attend college?

Do not assume the account becomes useless. First examine the plan’s options, eligible non-college education uses, beneficiary rules, and withdrawal treatment. The right choice depends on the plan and the family’s circumstances.

How does a 529 plan affect financial aid?

Financial-aid treatment can depend on account ownership and the beneficiary’s circumstances. Because the supplied evidence does not establish a universal calculation, check the current aid rules and the selected plan before estimating the effect.

Is my state’s plan always the best choice?

No. The SEC advises comparing out-of-state plans too. An in-state incentive may be valuable, but lower costs elsewhere can sometimes outweigh it. Compare net costs, benefits, choices, and restrictions.

Financial LiteracyBeginnerEducation SavingsPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team