A high-yield savings account is a savings account designed to pay a more competitive interest rate than a standard savings account. It keeps money separate from everyday spending while allowing the balance to earn interest. That can make it useful for an emergency fund, a planned purchase, or other short-term savings goals.

What is a High-Yield Savings Account?

A high-yield savings account is a savings account designed to pay a more competitive interest rate than a standard savings account. It keeps money separate from everyday spending while allowing the balance to earn…

5 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

The word “high-yield” does not guarantee that one account will always have the best rate. Rates, fees, balance rules, access methods, and account terms can differ and may change. The practical goal is therefore to compare the whole account—not just the advertised rate—and choose one that fits how you plan to save and withdraw money.

How a high-yield savings account works

You deposit money, the financial institution applies an interest rate, and the account periodically credits the interest earned. If credited interest remains in the account, future interest may be calculated on a larger balance. This is the basic compounding effect.

The most useful comparison figure is usually the annual percentage yield, or APY. The Consumer Financial Protection Bureau explains APY as an annualized rate reflecting the relationship between the interest a consumer would earn for an account term and the principal used to calculate it. In plain language, APY gives you a standardized annual view of earning potential under stated assumptions.

APY and the underlying interest rate are related, but they are not interchangeable. When comparing accounts, use APY against APY and read the assumptions and conditions attached to each offer. An attractive advertised rate may apply only when certain balance, deposit, or account-use requirements are met.

Here is a simple hypothetical example. Suppose two accounts have the same balance and neither charges a fee. If Account A has a higher APY than Account B throughout the same period, Account A would be expected to credit more interest. But if Account A adds a monthly fee or requires behavior you cannot maintain, its practical advantage may shrink or disappear.

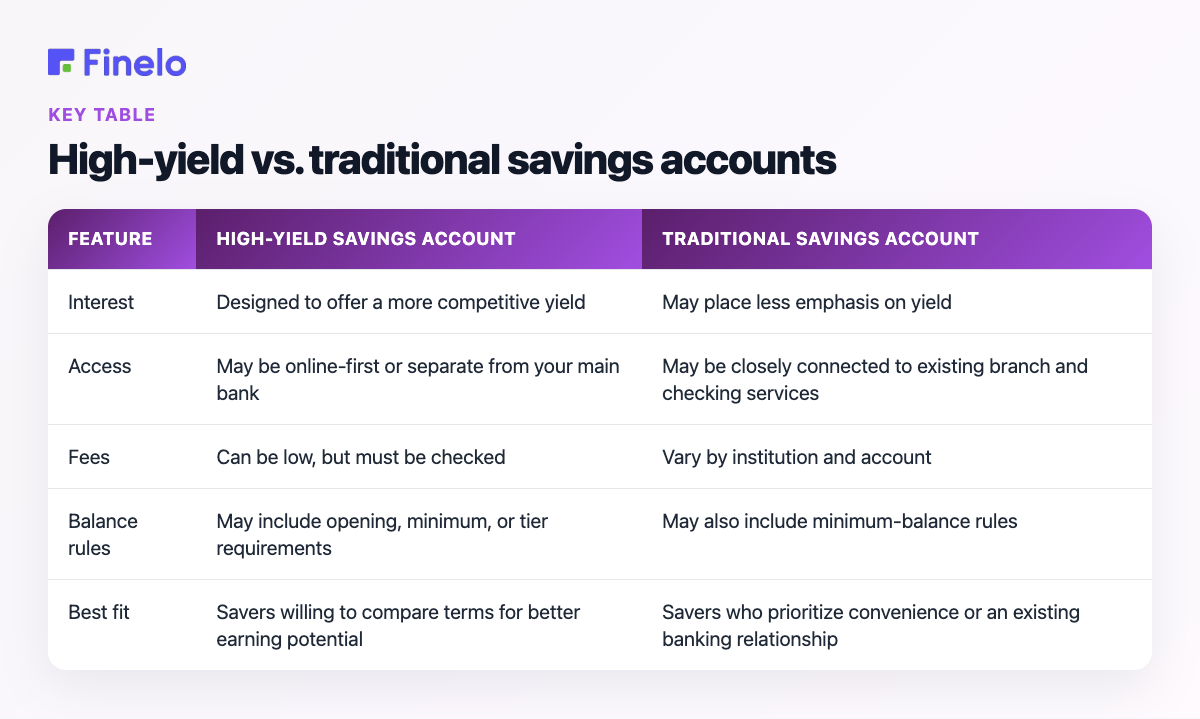

High-yield vs. traditional savings accounts

Both account types serve the same broad purpose: holding savings while paying interest. The meaningful differences are found in the current account terms.

| Feature | High-yield savings account | Traditional savings account |

|---|---|---|

| Interest | Designed to offer a more competitive yield | May place less emphasis on yield |

| Access | May be online-first or separate from your main bank | May be closely connected to existing branch and checking services |

| Fees | Can be low, but must be checked | Vary by institution and account |

| Balance rules | May include opening, minimum, or tier requirements | May also include minimum-balance rules |

| Best fit | Savers willing to compare terms for better earning potential | Savers who prioritize convenience or an existing banking relationship |

Neither label tells the complete story. A traditional account with favorable terms may suit you better than a high-yield account with inconvenient access or costly conditions. Compare the actual disclosures rather than assuming the category name guarantees value.

Benefits and appropriate uses

The central benefit is the opportunity to earn more interest on cash that would otherwise sit in a lower-yield account. A high-yield account can also create useful separation between daily spending and planned savings.

Common uses include:

- An emergency fund that needs to remain accessible

- Money reserved for a near-term purchase

- A sinking fund for irregular bills

- Cash being held while you decide on a longer-term plan

Liquidity matters here. A savings account is generally chosen for money you may need sooner than funds committed to a long-term investment. However, “accessible” does not necessarily mean instant. Transfer timing, withdrawal methods, transaction rules, and links to another bank can affect how quickly you can use the money.

A higher yield may help cash lose purchasing power more slowly when prices rise, but it does not guarantee that savings will keep pace with inflation. The account remains a cash-management tool, not a promise of a positive return after inflation.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Risks and tradeoffs to consider

High-yield savings accounts are relatively straightforward, but they are not free of tradeoffs.

The rate can change. Savings rates are often variable. An account that looks attractive today may become less competitive later, so occasional reviews are worthwhile.

Fees can offset interest. Monthly maintenance, excess activity, outgoing transfer, or other charges may reduce the account’s net benefit. Check the current fee schedule before opening.

Requirements may limit the advertised benefit. A promoted APY may depend on balance tiers or other conditions. Confirm which APY applies to the amount and activity you expect.

Access may be less convenient. An online-first account may not provide the branch, cash, ATM, or immediate-transfer experience you prefer.

Protection depends on the institution and account structure. Do not rely on a “high-yield” label as proof that your deposits are protected. Verify the institution, the account’s eligibility for applicable deposit protection, and how ownership or aggregate balances affect coverage.

Opportunity cost still exists. Cash held for stability and near-term access may have different long-term growth potential from investments, which carry their own risk of loss. The right allocation depends on the purpose and time horizon of the money.

How to choose an account

Start with your savings goal, then compare accounts using the same checklist:

- Confirm the applicable APY. Check whether it applies to your expected balance and whether any conditions are attached.

- Review every fee. Estimate what you would pay based on how you will actually use the account.

- Check minimums and tiers. Look for opening-deposit rules, minimum balances, and different yields at different balance levels.

- Test the access model on paper. Identify how you would deposit, transfer, and withdraw money—and how long each method may take.

- Verify the institution and deposit protection. Use the appropriate official regulator or insurance provider rather than relying only on marketing language.

- Read the account disclosures. Pay attention to how and when interest is calculated, when terms can change, and what could reduce earnings.

- Compare net usefulness. The best account is not automatically the one with the largest advertised APY; it is the one whose yield, costs, access, and rules work together for your needs.

If you are moving existing savings, keep enough money available for upcoming bills during the transition. Open and verify the new account, make a small test transfer, confirm access, and only then move the remaining amount you intend to save. Review any old account requirements before closing it.

Next steps

Define what the money is for, how soon you may need it, and what access you require. Then shortlist a few accounts and compare their current APYs, fees, minimums, transfer methods, and protection using the same checklist.

A high-yield savings account can be a practical home for short-term cash, but it is only one part of a broader financial plan. Finelo provides educational resources for people building their financial knowledge; use that learning alongside official account disclosures and consider professional guidance when a decision depends on your individual circumstances.

Frequently asked questions

How do I open a high-yield savings account?

Choose an institution, review its disclosures, and follow its application process. You may need to provide identity and contact information and select a way to fund the account. Before transferring a large balance, confirm the account details, applicable APY, fees, access methods, and deposit protection.

Can I access my money at any time?

That depends on the account. Review available withdrawal methods, transfer processing, transaction restrictions, and any fees. If the money is your emergency fund, focus on how quickly it can reach the account you use for essential payments.

How often do high-yield savings rates change?

There is no universal schedule. A variable rate can change when the institution updates its terms. Check current disclosures and account notices, and compare the account again if its yield changes materially.

Is a high-yield savings account worth it?

It can be worthwhile when the additional interest exceeds any added fees or inconvenience and the account matches your access needs. Compare the expected net benefit with your current account rather than deciding from the advertised APY alone.

Financial LiteracyBeginnerPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team