A pension plan is a workplace retirement arrangement designed to provide income after employment ends. The key question is what the plan promises: a defined benefit plan promises a specified retirement benefit, while a defined contribution plan builds an individual account whose eventual value can vary. The U.S. Department of Labor identifies these as the two main plan types.

What Is a Pension Plan? Pricing, Plans, and Value

A pension plan is a workplace retirement arrangement designed to provide income after employment ends. The key question is what the plan promises: a defined benefit plan promises a specified retirement benefit, while a…

6 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

For employees, the practical value of a pension depends on the plan’s formula or contribution rules, vesting requirements, payout choices, and restrictions—not simply on whether an employer calls it a “pension.” Always compare the official plan documents before making a retirement decision.

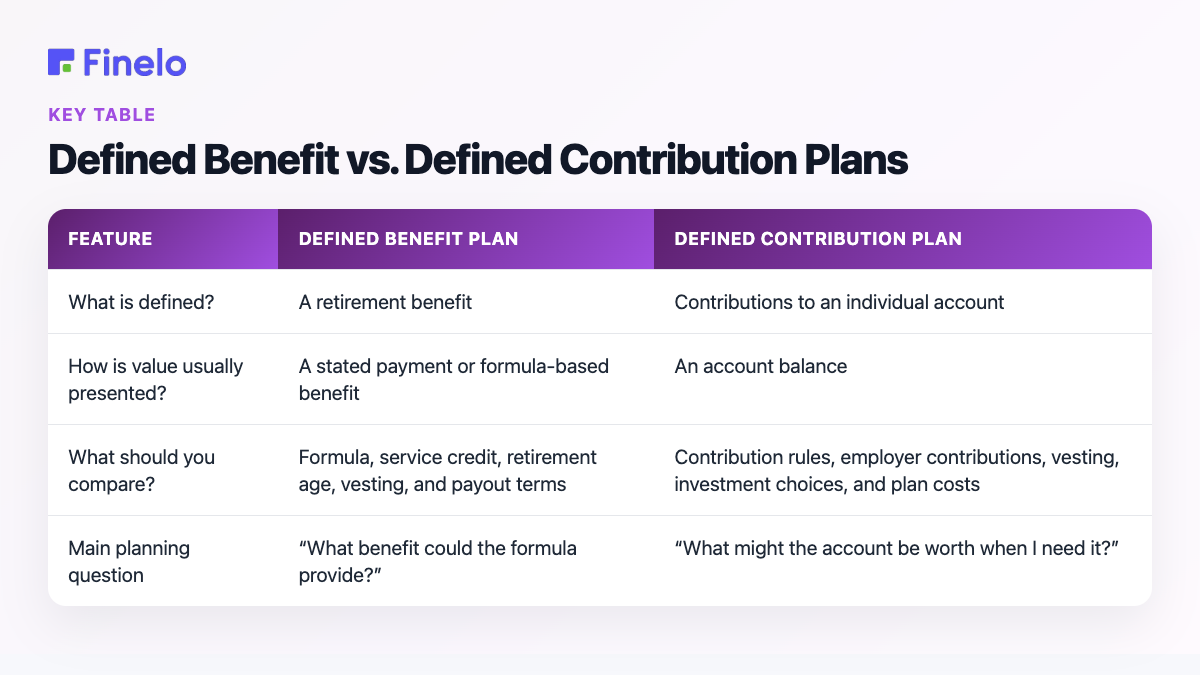

Defined Benefit vs. Defined Contribution Plans

The two plan types answer different questions. A defined benefit plan defines what the participant is promised at retirement. A defined contribution plan defines money going into an individual account, rather than promising a particular retirement payment.

| Feature | Defined benefit plan | Defined contribution plan |

|---|---|---|

| What is defined? | A retirement benefit | Contributions to an individual account |

| How is value usually presented? | A stated payment or formula-based benefit | An account balance |

| What should you compare? | Formula, service credit, retirement age, vesting, and payout terms | Contribution rules, employer contributions, vesting, investment choices, and plan costs |

| Main planning question | “What benefit could the formula provide?” | “What might the account be worth when I need it?” |

The Department of Labor explains that a defined benefit plan may promise an exact amount or use a formula based on factors such as salary and service. Its example uses 1% of average salary over the last five years of employment for each year of service.

That distinction matters when comparing value. A larger contribution percentage does not automatically make one plan better, and a formula-based benefit cannot be judged from a single summary figure. The useful comparison is the likely benefit under your circumstances, the conditions attached to it, and how it fits with your other retirement resources.

How Pension Benefits Are Calculated

There is no universal pension formula. For a defined benefit plan, a common structure is:

benefit factor × pensionable pay × credited service

For example, imagine a plan using the Department of Labor’s illustrative structure: 1% of average salary for the final five years, multiplied by years of service. If average salary were $60,000 and credited service were 25 years, the calculation would be:

1% × $60,000 × 25 = $15,000 per year

This is an educational example, not an estimate for any specific plan. A real plan may define pay differently, cap credited service, apply early-retirement adjustments, or use another formula entirely. The only reliable inputs are those in the employer’s official plan documents and benefit statement.

For a defined contribution plan, there is no comparable promised-benefit formula. Its value depends on amounts contributed to the account and what happens to those funds over time. When comparing plans, look beyond the current balance and identify which contributions are yours, which come from the employer, and which amounts are vested.

Vesting, Leaving a Job, and Accessing Money

Vesting determines when an employer-provided benefit becomes yours. It is different from eligibility. You may join a plan before all employer-funded benefits are vested. The Department of Labor says workers may lose unvested employer benefits when they leave, but they keep the vested portion.

If you leave your job, do not assume that the benefit disappears—or that you can immediately withdraw all of it. The outcome depends on the plan type and its terms. A vested defined benefit may remain payable at an eligible retirement date, while a defined contribution plan may offer choices for handling the vested account balance. Unvested employer-funded amounts may be treated differently.

Before leaving, ask the plan administrator for a written explanation covering:

- Your vested percentage and credited service

- The benefit or account balance currently shown

- The normal and earliest permitted retirement dates

- Available payout or transfer choices

- Deadlines, restrictions, and possible reductions

- Who to contact after your employment ends

Early access is plan-specific. The IRS says plans generally distribute benefits only after certain events. The plan summary should state whether it allows early withdrawals, hardship distributions, or loans. Getting money sooner may leave less for later. Review the financial and tax effects before acting.

Payout Options and Overall Value

Some plans offer more than one payout method. For defined benefit plans, the IRS describes the normal method as an annuity for the employee’s life or the joint lives of the employee and spouse. Other options may be available. Compare choices on the same basis instead of focusing on the largest-looking number.

A practical checklist is:

- Is the quoted amount monthly, annual, or a one-time payment?

- When can payments begin?

- Does starting earlier change the payment?

- Does the option provide anything for a spouse or beneficiary?

- Can the choice be changed after it is made?

- What taxes, costs, or administrative limits could apply?

This is the pension equivalent of comparing pricing and plan limits. The “cost” is not just an amount paid today; it can include reduced flexibility, delayed access, plan fees where applicable, or giving up one form of future benefit for another. The “value” is the benefit you can actually use under the plan’s conditions.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Pension Plans and Social Security

A workplace pension and Social Security are separate parts of retirement planning. A major federal rule has changed. The Social Security Administration says a pension from work not covered by Social Security no longer reduces benefits payable from January 2024 onward. The Social Security Fairness Act removed two former reductions: the Windfall Elimination Provision and Government Pension Offset.

That does not make a generic pension estimate sufficient for retirement planning. Use separate, current statements for each benefit, then compare expected start dates, payment amounts, and assumptions. Workers whose careers span different employers, states, or public and private employment should confirm the records used by each program. State and public-sector pension plans can have their own eligibility and benefit provisions, so the relevant plan administrator—not a general example—should confirm the pension rules.

Common Pension Misconceptions

“Every pension guarantees the same kind of income.”

No. The plan type and official terms determine what is promised. Defined benefit and defined contribution plans work differently.

“My salary alone determines the benefit.”

Not necessarily. A defined benefit formula may consider salary and service, but the plan decides how each input is defined.

“Leaving my employer means losing everything.”

No. Vesting and the plan’s separation rules determine what remains available. Once vested, a participant retains the right to the vested benefit even after leaving before retirement.

“The biggest lump sum is always the best option.”

A one-time figure cannot be compared fairly with ongoing payments without considering timing, longevity, beneficiary needs, taxes, and flexibility.

What to Do Next

This page is for employees and beginners who need a clear framework before reviewing a workplace retirement offer or benefit statement. Start by identifying the plan type, then collect the summary plan description, current statement, vesting information, and payout rules. Write down any unclear terms and ask the plan administrator to explain them in writing.

Finelo approaches the topic as financial education rather than personalized advice. You can continue building your investing and retirement vocabulary through Finelo’s learning experience, then verify any decision against your official plan documents and, when needed, a qualified financial or tax professional.

Product, Course, App and Platform Experience

This page provides education, not pension administration or personal advice. A course, app, or learning platform can explain terms and help you prepare questions. Only your plan documents and administrator can confirm your benefit.

Frequently asked questions

How do I know whether my employer offers a pension plan?

Check your benefits portal, offer materials, pay information, or employee handbook, then ask human resources or the plan administrator for the official plan name and documents. Do not rely only on informal workplace descriptions.

What happens to my pension if I leave my job?

It depends on vesting and the plan’s rules. Ask for a statement showing the vested benefit or account balance, when it can be accessed, and which choices remain available after separation.

Can I access pension funds early?

Only if the plan permits an early distribution or early retirement option. Access may be restricted or may change the amount available later, so review the written terms and consequences first.

Should I use a financial advisor for a pension decision?

Professional help may be useful when comparing irreversible payout choices, coordinating several retirement resources, or evaluating tax consequences. An advisor can help analyze the options, but the plan administrator remains the source for the plan’s actual rules and benefit figures.

Financial LiteracyBeginnerRetirementPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team