A recession is a broad, sustained decline in economic activity. It is usually visible across several areas at once: businesses sell less, production slows, hiring weakens, unemployment rises, and households become more cautious about spending. A short-lived decline in one statistic does not necessarily mean the whole economy is in recession.

What is a Recession? Understanding Economic Downturns

A recession is a broad, sustained decline in economic activity. It is usually visible across several areas at once: businesses sell less, production slows, hiring weakens, unemployment rises, and households become more…

9 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

For most people, the practical meaning is simpler: jobs may become less secure, borrowing can feel harder, businesses may delay expansion, and financial markets can move sharply. Understanding those effects helps households and business owners respond calmly instead of making decisions based only on alarming news reports.

The Economic Cycle: Recession and Recovery

Economies do not grow at a constant rate. Activity tends to move through a cycle:

- Expansion: Production, employment, income, and spending generally grow.

- Peak: Growth reaches a high point before momentum turns.

- Contraction or recession: Economic activity declines across a meaningful part of the economy.

- Trough: The decline reaches its low point.

- Recovery: Activity begins expanding again, although different households and industries may recover at different speeds.

Think of a manufacturer during an expansion. Strong orders may encourage it to hire workers, buy equipment, and increase inventory. If customer demand later weakens, the company may reduce production, postpone equipment purchases, and stop hiring. Similar choices across many businesses can reinforce a wider downturn. During recovery, improving orders may gradually reverse those decisions.

This cycle is not a clock. A recession does not begin or end merely because a certain amount of time has passed, and not every industry turns at the same moment.

Historical recessions do not follow one script. Some begin with financial stress. Others follow a sudden disruption, weaker demand, or the reversal of an overheated part of the economy. The trigger affects which industries weaken first and how the damage spreads.

Federal Reserve researchers have compared real GDP and unemployment across the last nine post-war U.S. recessions. This long view shows why one downturn should not become a universal template for the next (Federal Reserve Board).

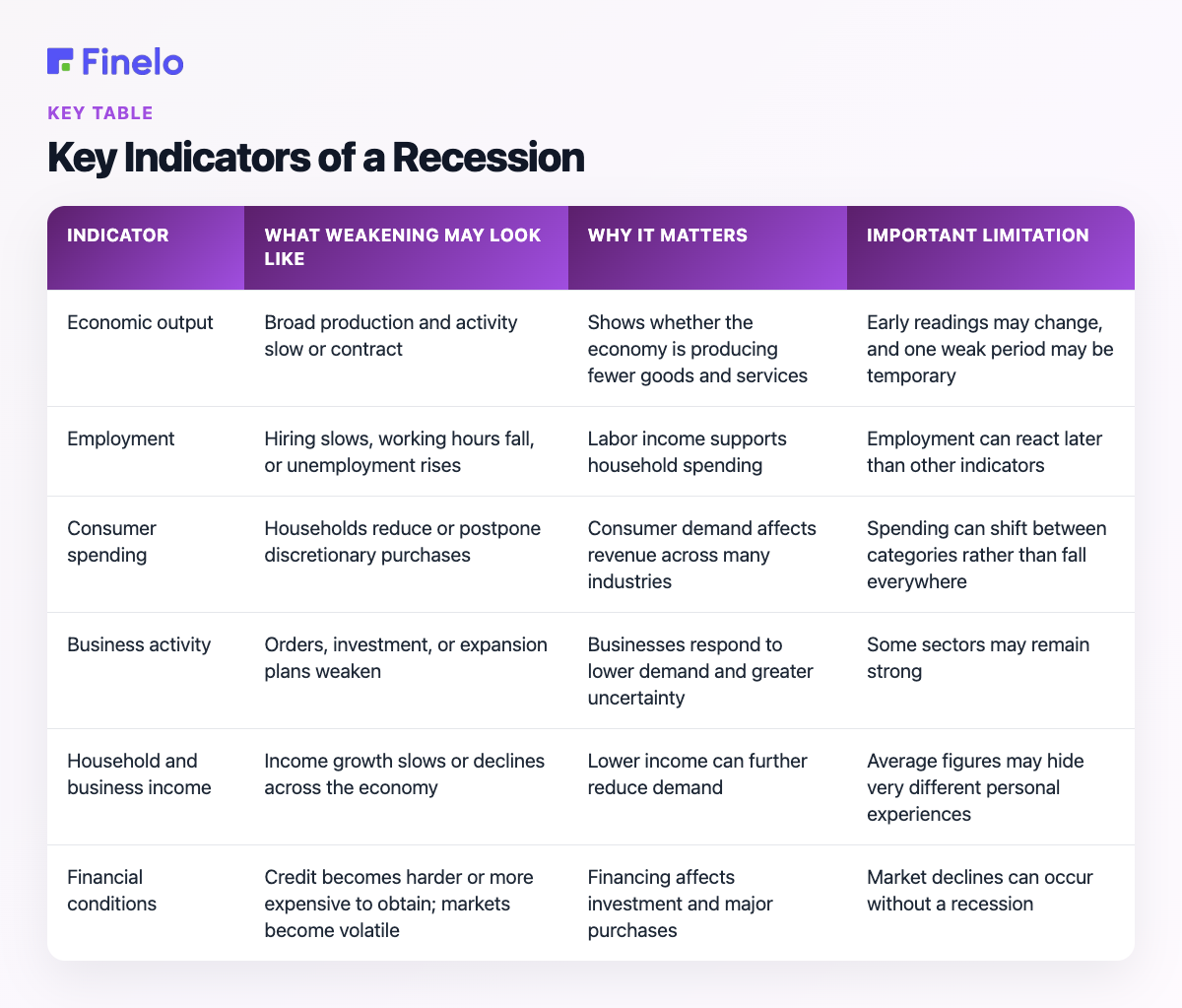

Key Indicators of a Recession

No single measure gives a complete real-time answer. Economic data may be delayed or revised. Individual sectors can also weaken while the wider economy remains resilient. A better approach is to look for a persistent pattern across output, employment, income, spending, inflation, and business conditions.

| Indicator | What weakening may look like | Why it matters | Important limitation |

|---|---|---|---|

| Economic output | Broad production and activity slow or contract | Shows whether the economy is producing fewer goods and services | Early readings may change, and one weak period may be temporary |

| Employment | Hiring slows, working hours fall, or unemployment rises | Labor income supports household spending | Employment can react later than other indicators |

| Consumer spending | Households reduce or postpone discretionary purchases | Consumer demand affects revenue across many industries | Spending can shift between categories rather than fall everywhere |

| Business activity | Orders, investment, or expansion plans weaken | Businesses respond to lower demand and greater uncertainty | Some sectors may remain strong |

| Household and business income | Income growth slows or declines across the economy | Lower income can further reduce demand | Average figures may hide very different personal experiences |

| Financial conditions | Credit becomes harder or more expensive to obtain; markets become volatile | Financing affects investment and major purchases | Market declines can occur without a recession |

The best warning sign is usually not one red cell in this table. It is several indicators deteriorating together and remaining weak. The Federal Reserve describes recession-risk models that combine financial variables with leading indicators of confidence and economic activity. This supports a dashboard approach instead of relying on one statistic (Federal Reserve Board).

For example, falling share prices alone do not prove a recession. But weaker business orders, slower hiring, rising unemployment, reduced household spending, and tighter credit at the same time would present a more concerning picture. The Federal Reserve notes that recessions can bring large increases in unemployment and major shifts in financial markets, illustrating why both the real economy and financial conditions deserve attention (Federal Reserve Board).

Are two quarters of falling GDP always a recession?

Two consecutive quarters of declining economic output are often used as a convenient rule of thumb. However, a broad assessment asks a bigger question: Is the weakness significant, persistent, and spread across the economy? Looking only at quarterly output can miss important changes in employment, income, and other activity—or suggest a downturn that is narrower than it first appears.

Different countries and institutions may emphasize different indicators or dating methods. In the United States, the National Bureau of Economic Research Business Cycle Dating Committee defines recession dates. Federal Reserve research also uses real GDP and unemployment to assess past recessions (Federal Reserve Board).

What Causes Recessions?

Recessions rarely have one simple cause. They can develop when a shock hits demand or supply, when financial stress limits borrowing, when earlier imbalances unwind, or when several pressures interact.

Common pathways include:

- Households cut spending. If people fear job losses or face tighter budgets, they may delay travel, vehicles, home improvements, and other purchases.

- Businesses reduce investment. Weak demand or uncertainty can lead companies to postpone hiring, buildings, equipment, and new projects.

- Credit conditions tighten. When financing becomes less available or more burdensome, spending and investment may slow.

- Costs or supply disruptions rise. Businesses may struggle to produce profitably, while households lose purchasing power.

- Asset or financial stress spreads. Falling values, defaults, or loss of confidence can weaken balance sheets and restrict activity.

- Policy settings restrain demand. Measures intended to address one economic problem can also slow borrowing and spending.

These forces can form a feedback loop. Imagine several retailers reporting weaker sales. They order less and reduce staff hours. Suppliers then cut production. Affected workers spend less, so other local businesses also feel the decline. A recession is the broad version of this process.

Historical downturns also differ in character. One may begin with financial disruption, another with an external shock, and another with an overheated part of the economy reversing. The lesson is not that every recession follows the same timeline, but that declining demand, employment, income, and confidence can reinforce one another.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Impacts of Recessions on Individuals and Businesses

The effects are uneven. A recession may be a worrying news story for one household, a reduction in hours for another, and a job loss or business closure for someone else.

Job security and household finances

When sales weaken, employers may freeze recruitment or leave vacancies unfilled. They may also reduce overtime, shorten hours, or eliminate roles. Industries tied to optional purchases or business investment may slow first. Essential services may follow a different pattern. The word “recession” alone cannot predict the fate of one job.

Lower or less predictable income can make fixed costs harder to manage. Concern about employment may also lead households to save more and spend less, which can further weaken demand. This does not mean caution is irrational; it means many sensible individual decisions can collectively slow the economy.

Businesses and entrepreneurs

Businesses may face lower revenue, slower customer payments, cautious lenders, and pressure on cash flow. Small companies can be especially sensitive when they depend on a few customers or carry high fixed costs.

Consider two businesses with similar sales. One has flexible expenses and enough cash for several weak months. The other has large debt payments, high inventory, and little room for a sales decline. The same downturn can affect them very differently. Cash flow and fixed obligations often matter as much as the industry.

Savings and investments

Recessions can coincide with sharp market movements. The Federal Reserve explicitly links recessions with large shifts in financial markets and increases in unemployment (Federal Reserve Board). Still, the economy and asset prices do not move in perfect lockstep. Markets reflect expectations, so they may react before economic data confirms a downturn.

That is why a recession report alone is a weak basis for an investment decision. A better process considers time horizon, diversification, liquidity needs, costs, risk tolerance, and the possibility that forecasts will be wrong. Financial education can help readers understand those concepts, but it does not replace personalized professional advice.

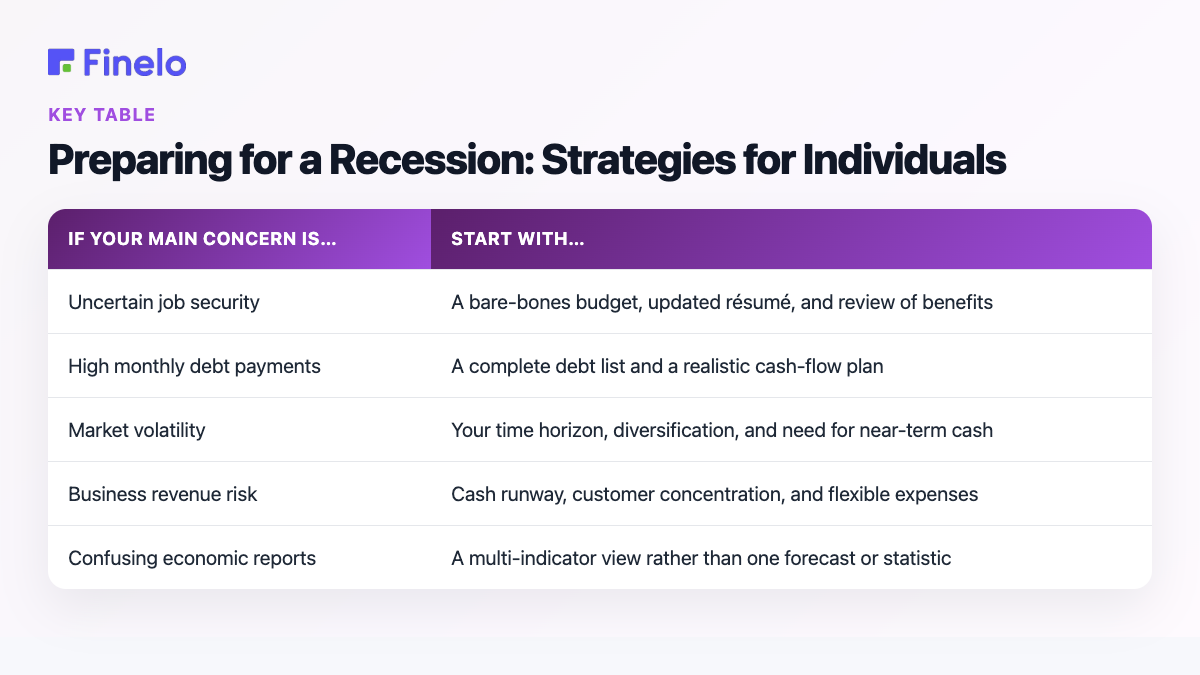

Preparing for a Recession: Strategies for Individuals

Preparation is less about predicting the exact start date. It is about making your money situation better able to absorb surprises. The following checklist is educational and should be adapted to your circumstances.

- Review essential monthly expenses. Separate necessities from spending that could be reduced temporarily.

- Build accessible financial reserves where possible. Even a modest buffer can reduce dependence on expensive borrowing after an income shock.

- Understand your debts. List balances, rates, minimum payments, and whether payments could change.

- Protect employability. Keep your résumé, professional contacts, certifications, and work samples current.

- Check insurance and workplace benefits. Know what coverage you have before you need it.

- Avoid decisions driven solely by fear. Reassess financial choices against your goals, timeline, liquidity needs, and ability to bear losses.

- Plan for more than one scenario. Consider what you would do after reduced hours, a job loss, or a major unexpected bill.

A simple decision framework can turn general concern into a next step:

| If your main concern is… | Start with… |

|---|---|

| Uncertain job security | A bare-bones budget, updated résumé, and review of benefits |

| High monthly debt payments | A complete debt list and a realistic cash-flow plan |

| Market volatility | Your time horizon, diversification, and need for near-term cash |

| Business revenue risk | Cash runway, customer concentration, and flexible expenses |

| Confusing economic reports | A multi-indicator view rather than one forecast or statistic |

For example, someone worried about layoffs might first calculate essential monthly spending and identify which costs could be paused. That creates a usable plan whether or not a recession arrives. Someone with stable employment but volatile investments may instead focus on whether near-term expenses are exposed to market losses.

Government Responses to Recessions

Public responses generally aim to support economic activity, financial stability, or household and business income. Depending on the circumstances, authorities may adjust interest-rate settings, change public spending or taxes, support credit markets, or provide targeted relief. These choices interact with inflation, employment, borrowing, and consumer spending.

Each response involves tradeoffs. Support for demand can also affect borrowing, prices, or public finances. Policy may take time to reach households and businesses. Easier financing can encourage borrowing, for example. It cannot instantly repair every balance sheet or restore demand in every industry.

This is another reason recessions and recoveries do not feel uniform. Policy can influence overall conditions, while an individual worker, region, or sector may continue to struggle after broader indicators begin improving.

Conclusion: Understanding and Navigating Recessions

A recession is not simply a falling market or one weak GDP report. It is a meaningful, broad decline in economic activity that can affect employment, income, spending, businesses, credit, and financial markets.

The most useful response is practical rather than predictive: track several indicators, understand your essential expenses, strengthen your financial buffer where possible, review debt and insurance, and keep career plans current. Readers who want to build their understanding of investing concepts can use Finelo’s financial education starting point while treating all investment decisions as personal, risk-bearing choices that require careful evaluation.

Frequently asked questions

What is the simplest definition of a recession?

A recession is a broad and sustained decline in economic activity. It usually involves weakness across several measures, such as output, employment, income, spending, and business activity—not merely a bad week in markets or a slowdown in one industry.

What is the difference between a recession and a depression?

Both terms describe economic downturns, but “depression” generally refers to an exceptionally severe and prolonged collapse. There is no need to assume that an ordinary recession will become a depression. The practical distinction is the downturn’s depth, duration, and reach.

How long does a recession last?

There is no fixed duration. The decline may be relatively brief or persist longer, and recovery can take different amounts of time across employment, household income, business activity, and financial markets.

What should I invest in during a recession?

There is no universally suitable recession investment. Choices depend on goals, time horizon, cash needs, diversification, costs, and tolerance for loss. Avoid treating an economic forecast as certainty, and verify the risks and suitability of any investment before acting.

Financial LiteracyBeginnerEconomicsPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team