A Roth conversion moves retirement money from a traditional, tax-deferred account into a Roth IRA. The central tradeoff is timing: you generally recognize untaxed converted money as taxable income now in exchange for holding it in a Roth account for the future. The IRS confirms that untaxed amounts converted to a Roth IRA are taxed and that the conversion is reported on Form 8606.

What is a Roth Conversion?

A Roth conversion moves retirement money from a traditional, tax-deferred account into a Roth IRA. The central tradeoff is timing: you generally recognize untaxed converted money as taxable income now in exchange for…

7 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

That can be useful when paying tax today appears preferable to paying it later. It can also be costly if the conversion pushes more income into a higher tax bracket, creates an unaffordable tax bill, or does not fit your retirement timeline. A conversion is therefore less about finding a universally “best” account and more about choosing when to recognize taxable income.

How a Roth conversion works

A conversion changes the tax status of retirement assets; it is not a new annual contribution. You select an amount in an eligible traditional retirement account, arrange for it to move into a Roth IRA, and account for any taxable portion on your tax return.

The amount can be all or part of an account. Partial conversions are often easier to evaluate because they let you control how much additional taxable income you recognize in one year.

At a high level, the process involves:

- Identifying the account and amount you may want to convert.

- Estimating how much of that amount has not previously been taxed.

- Adding the taxable portion to the rest of your projected income for the year.

- Estimating the resulting federal and state tax impact.

- Deciding whether to convert now, convert a smaller amount, or wait.

- Keeping the tax documents needed to report the transaction.

The IRS states that a Roth conversion results in taxation of untaxed traditional IRA amounts and is reported on Form 8606. That makes recordkeeping especially important when an account contains a mix of pretax and after-tax money.

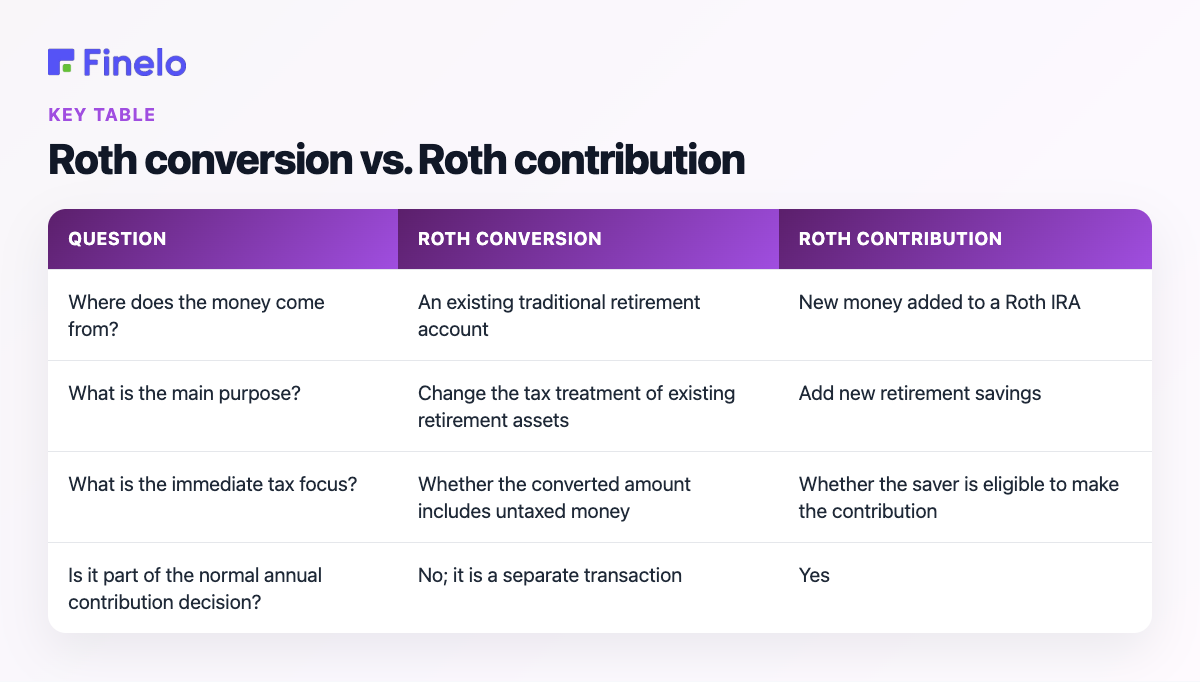

Roth conversion vs. Roth contribution

These terms sound similar but describe different actions.

| Question | Roth conversion | Roth contribution |

|---|---|---|

| Where does the money come from? | An existing traditional retirement account | New money added to a Roth IRA |

| What is the main purpose? | Change the tax treatment of existing retirement assets | Add new retirement savings |

| What is the immediate tax focus? | Whether the converted amount includes untaxed money | Whether the saver is eligible to make the contribution |

| Is it part of the normal annual contribution decision? | No; it is a separate transaction | Yes |

The practical distinction matters. Someone may be unable or unwilling to make a new contribution but still be evaluating whether to convert existing retirement assets. Conversely, opening or funding a Roth IRA does not automatically mean a conversion has occurred.

Potential benefits and drawbacks

A Roth conversion can create more flexibility in how retirement money is divided between account types. But its value depends on the tax paid today, the future treatment of the account, the time available, and the person’s broader financial plan.

Potential benefits

- Changing when income is taxed. A conversion may be attractive in a year when taxable income is temporarily lower than expected in future years.

- Building tax diversification. Holding retirement assets with different tax treatments may provide more options when planning future withdrawals.

- Using a long time horizon. The longer money is expected to remain invested, the more relevant the long-term account structure may become.

- Reducing uncertainty about future tax timing. Paying tax on a known conversion amount today may appeal to someone who prefers to address that liability now.

Potential drawbacks

- An immediate tax bill. The IRS says untaxed converted amounts are taxable, so a large conversion can create a substantial current-year obligation.

- Higher marginal taxation. Additional taxable income can cause later portions of a conversion to be taxed differently from earlier portions.

- Less cash available elsewhere. Money reserved for conversion taxes cannot also serve another goal, such as an emergency fund.

- Forecasting risk. The decision depends partly on future income, tax rules, spending, and longevity—none of which can be known perfectly.

- Administrative complexity. Mixed pretax and after-tax balances can make the taxable portion harder to estimate.

The key question is not simply, “Will I pay tax?” It is, “Does paying the estimated tax now improve my overall plan compared with leaving the assets where they are?”

Who may consider a Roth conversion?

A conversion may deserve closer analysis when current taxable income is unusually low, retirement is approaching but taxable withdrawals have not begun, or a person wants a different balance between traditional and Roth assets.

It may also be relevant to higher-income earners who are examining ways to reposition existing retirement money. High income does not make the tax cost disappear; it can make careful sizing more important because the conversion itself adds taxable income.

A conversion may be less appealing when:

- Current income is already unusually high.

- The tax bill would require draining cash needed for near-term expenses.

- The money may need to be withdrawn soon.

- The expected future tax benefit is small or highly uncertain.

- The account records are incomplete and the taxable portion cannot yet be estimated reliably.

This is a planning question, not a test with one correct answer. Two people with equal IRA balances can reach different conclusions because their current income, future income, cash reserves, state taxes, and time horizons differ.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

How to estimate an appropriate conversion amount

Rather than beginning with the full account balance, start with the tax return. Estimate income without a conversion, then test several conversion amounts.

Consider a simplified hypothetical example. A household projects $80,000 of taxable income before a conversion and is considering converting $10,000, $30,000, or $60,000. The decision is not made by comparing those amounts alone. The household would estimate how each scenario changes taxable income, the marginal tax applied to the added income, state taxes, available cash, and the balance left in each account type.

This framework keeps the decision focused:

| Scenario | Current-year tax cost | Cash needed for tax | Traditional balance remaining | Roth balance created | Overall fit |

|---|---|---|---|---|---|

| No conversion | Baseline | Baseline | Highest | None from conversion | Preserves current tax deferral |

| Smaller partial conversion | Lower added cost | Lower | Moderately reduced | Smaller | May limit tax impact |

| Larger partial conversion | Higher added cost | Higher | More reduced | Larger | May accelerate the strategy |

| Full conversion | Highest immediate exposure | Highest | None in converted account | Largest | Requires the strongest tax and cash-flow case |

The figures in this exercise should come from the person’s own records and current tax estimates. The useful output is not merely a projected tax bill, but a comparison showing what is gained and given up in each scenario.

When comparing different tax brackets, focus on the marginal cost of each additional conversion dollar. A first portion may fit within a lower bracket while another portion falls into a higher one. That is one reason people often evaluate conversions in annual stages instead of treating the decision as all-or-nothing.

Tax planning details to review

Before acting, review more than the account balance.

- Taxable versus after-tax amounts: Determine whether the account contains money that has already been taxed.

- Other income: Wages, business income, investment income, and other taxable items can affect the conversion’s marginal cost.

- State treatment: State tax consequences may differ from federal consequences.

- Cash source: Decide how the conversion tax would be paid without weakening essential reserves.

- Timing: Income can change during the year, so an estimate made early may need to be updated.

- Documentation: Retain account statements and tax forms, including the information needed for Form 8606.

- Beneficiaries: If estate planning is part of the goal, review how the account fits the needs of the intended beneficiaries rather than assuming every heir will benefit in the same way.

For non-spouse beneficiaries in particular, inherited-account decisions can be sensitive to the beneficiary’s own circumstances and the rules in effect at the time. A conversion should not be justified solely by a general claim that “Roth is better for heirs.” The account owner’s tax cost and the beneficiary’s likely situation both belong in the analysis.

A practical decision checklist

Use this checklist to organize a conversation with a tax or financial professional:

- What portion of the proposed conversion would be taxable?

- What is projected taxable income before the conversion?

- How would several conversion amounts change the estimated tax bill?

- Can the tax be paid from cash without disrupting essential goals?

- How long is the converted money expected to remain in the account?

- What assumptions are being made about future income and tax rates?

- Does a partial conversion provide enough benefit with less current-year risk?

- Are federal and state consequences both included?

- Are account records complete enough to report the conversion correctly?

- How does the decision affect beneficiaries and the rest of the retirement plan?

If several answers are uncertain, the next step is better information—not a rushed conversion.

Next steps

Start by gathering your latest tax return, retirement account statements, records of any after-tax contributions, and an estimate of current-year income. Then compare no-conversion, smaller-conversion, and larger-conversion scenarios. Verify the tax calculation and reporting requirements before moving money.

A Roth conversion can be useful, but only when the current tax cost, available cash, time horizon, and retirement goals work together. Use the framework above for education and preparation, then seek individualized tax or financial guidance if the decision could materially affect your finances. For more foundational investing education, explore Finelo.

Frequently asked questions

Can a Roth conversion be undone?

Do not assume you can reverse the transaction later. Confirm the current rules and the consequences before converting, especially when the amount is large.

How much should I convert each year?

There is no universal amount. Compare multiple scenarios based on projected income, marginal tax cost, available cash, time horizon, and the desired balance between traditional and Roth assets. A partial conversion may offer more control than converting an entire account at once.

Does a conversion avoid tax?

Not necessarily. It generally changes the timing of taxation. The [IRS specifically states that untaxed amounts in a traditional IRA become taxable when converted to a Roth IRA](https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-iras).

Is a Roth conversion only for high-income earners?

No. Income is one factor, but the decision can be relevant to anyone comparing the current tax cost with the potential long-term fit of Roth assets. Higher earners may need to pay particular attention to the marginal cost of adding conversion income.

Financial LiteracyBeginnerRetirementPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team