A sinking fund is money you set aside gradually for a specific expense you expect in the future. Instead of finding the full amount when a bill or purchase arrives, you divide the goal into smaller contributions and save them over time. You might use one for annual insurance, a vacation, home maintenance, holiday gifts, or a replacement laptop you expect to buy next year.

What is a Sinking Fund? Understanding Its Importance and Benefits

A sinking fund is money you set aside gradually for a specific expense you expect in the future. Instead of finding the full amount when a bill or purchase arrives, you divide the goal into smaller contributions and…

6 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

Introduction to sinking funds

The term also has a formal meaning in bond finance: a bond issuer may make periodic payments into an account used to redeem outstanding bonds, according to Charles Schwab’s fixed-income glossary. In personal budgeting, the same basic idea becomes a practical planning tool: contribute now toward a known future obligation.

How a sinking fund works

A sinking fund has four parts:

- A clearly defined expense

- A target amount

- A deadline

- A regular contribution

The basic calculation is:

Amount still needed ÷ number of saving periods remaining = contribution per period

Suppose you want $1,200 for a trip in 10 months and have already saved $200. You still need $1,000, so your target contribution is $100 per month:

($1,200 − $200) ÷ 10 = $100

If you are paid every two weeks and prefer to contribute from each paycheck, you can divide the remaining amount by the number of paychecks before the deadline instead. The useful interval is the one that fits your budget and makes progress easy to track.

A sinking fund is a purpose, not necessarily a special financial product. You can keep the money in an account or budgeting category that lets you identify the balance for that goal. For short-term goals, Investor.gov says a savings account can be a suitable choice. If you maintain several funds, separate labels or subaccounts can help prevent money intended for one expense from quietly being used for another.

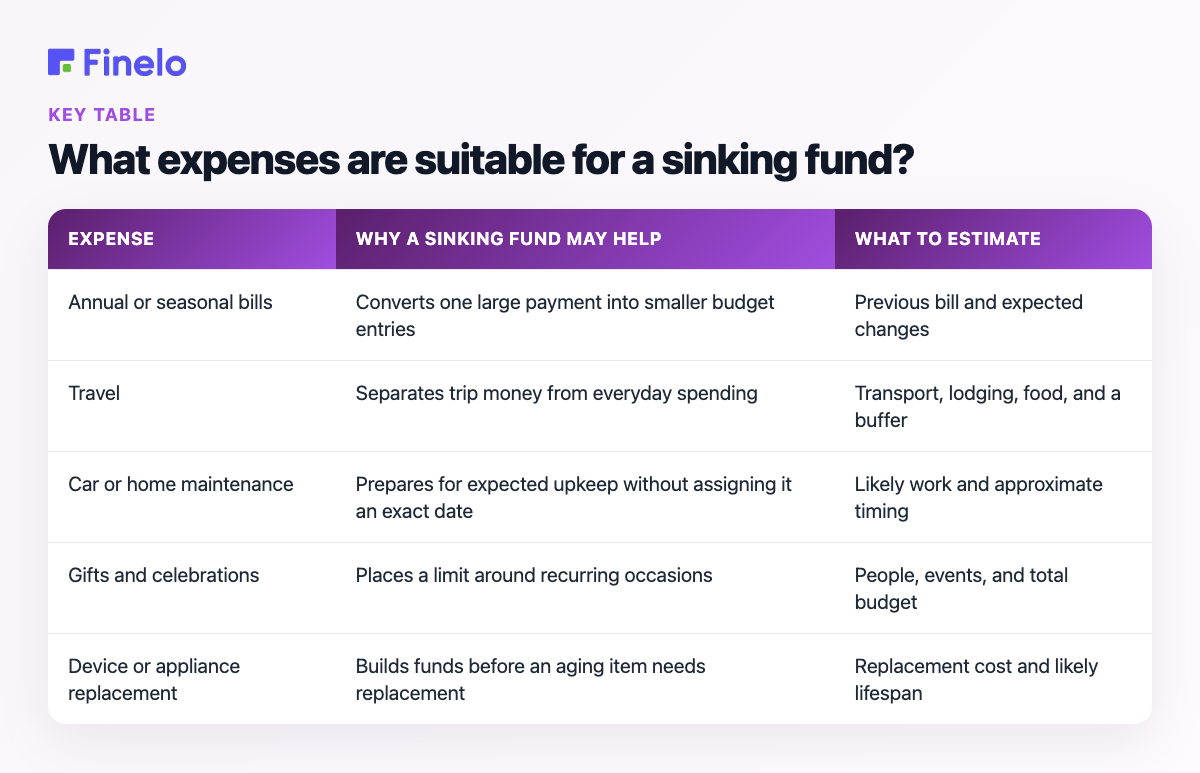

What expenses are suitable for a sinking fund?

Sinking funds work best for costs that are reasonably predictable, even when the exact date or amount is not certain. The Consumer Financial Protection Bureau recommends looking back over several months for less frequent costs such as insurance, gifts, and vacations. Common examples include:

| Expense | Why a sinking fund may help | What to estimate |

|---|---|---|

| Annual or seasonal bills | Converts one large payment into smaller budget entries | Previous bill and expected changes |

| Travel | Separates trip money from everyday spending | Transport, lodging, food, and a buffer |

| Car or home maintenance | Prepares for expected upkeep without assigning it an exact date | Likely work and approximate timing |

| Gifts and celebrations | Places a limit around recurring occasions | People, events, and total budget |

| Device or appliance replacement | Builds funds before an aging item needs replacement | Replacement cost and likely lifespan |

Not every goal needs its own fund. Too many small categories can become difficult to manage. You might group similar expenses—such as birthdays and holidays—when one combined target is easier to maintain.

Benefits of using a sinking fund

The main benefit is visibility. A future expense stops being a vague concern and becomes a number with a schedule. That can make it easier to judge whether the goal is realistic before committing to the purchase or relying on credit. Although saving cannot erase the cost, having money reserved may reduce the amount of new debt needed for the planned expense.

A sinking fund may also:

- Smooth irregular expenses across several monthly budgets

- Reduce the temptation to treat planned costs as emergencies

- Make tradeoffs clearer when several goals compete for limited money

- Show early when a deadline, target, or contribution needs adjustment

- Create a spending boundary for optional purchases

The method does not make an expense cheaper, and it cannot guarantee that every surprise will be covered. Its value comes from matching money to an anticipated use before the expense arrives.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

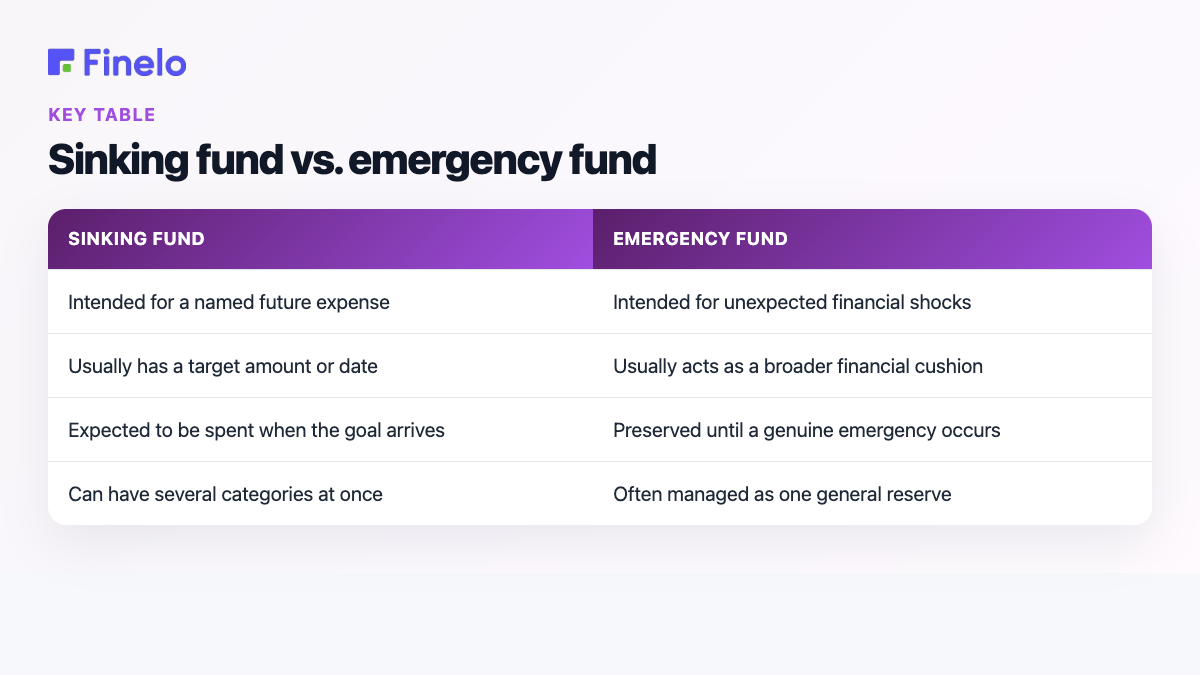

Sinking fund vs. emergency fund

The distinction is mainly about predictability and purpose.

| Sinking fund | Emergency fund |

|---|---|

| Intended for a named future expense | Intended for unexpected financial shocks |

| Usually has a target amount or date | Usually acts as a broader financial cushion |

| Expected to be spent when the goal arrives | Preserved until a genuine emergency occurs |

| Can have several categories at once | Often managed as one general reserve |

A car illustrates the difference. Saving for routine servicing or an eventual tire replacement can be a sinking-fund goal because those costs are foreseeable. A sudden major repair may call for an emergency reserve if it was not reasonably planned for.

The categories can overlap at the edges. What matters is deciding in advance what each pool of money is meant to cover. Clear rules help you avoid draining emergency savings for predictable purchases—like annual bills—or leaving planned money untouched during a situation it was created to handle.

Practical steps to create a sinking fund

- Choose one specific goal. Start with an expense that has a clear purpose rather than a general instruction to “save more.”

- Estimate the full cost. Review recent statements or receipts, include the major components, and add a reasonable cushion if the final amount could vary.

- Set a deadline. Use the payment date, event date, or your best estimate of when the money will be needed.

- Subtract what you already have. Only the remaining amount needs to be divided across future contributions.

- Calculate a contribution. Divide the balance by the months, weeks, or paychecks remaining.

- Check it against your budget. The CFPB advises including regular contributions to savings goals in your budget. If the contribution does not fit, lower the target, extend the timeline, reduce another expense, or reconsider the goal.

- Keep the money identifiable. Use a separate account, subaccount, or clearly labeled budget category if that helps you stay organized.

- Review progress regularly. Update the plan when the expected cost, deadline, or your available income changes.

Automation can reduce the number of decisions required, but it is still worth checking the balance. A transfer that once fit comfortably may become unrealistic after a change in income or essential expenses.

Common mistakes to avoid

Using an unrealistically precise estimate. Prices and plans can change. Review the target instead of assuming the first number will remain accurate.

Ignoring cash-flow timing. A monthly average may look affordable even though the transfer falls during a week with several large bills. Match contributions to the rhythm of your income.

Mixing every goal together without records. One balance can work, but only if you track how much belongs to each purpose.

Funding optional goals while neglecting urgent obligations. A sinking fund should fit within a wider budget. Reassess priorities if contributions interfere with essential expenses or required payments.

Treating a missed target as failure. If you fall behind, recalculate. Saving part of the cost can still reduce the amount you must find later.

Conclusion and next steps

Pick one predictable expense, write down its estimated cost and due date, then calculate the contribution required from each paycheck or month. Keep the plan simple enough to maintain and revisit it when your circumstances change.

This article is educational rather than personalized financial advice. For more beginner-focused financial education, explore Finelo.

Frequently asked questions

Can I have multiple sinking funds?

Yes. You can save for several goals at once if the combined contributions fit your budget. Rank them by urgency and importance rather than contributing equally by default.

Where should I keep a sinking fund?

Choose a place that keeps the money identifiable, accessible when needed, and appropriate for the goal’s timeline. Investor.gov notes that a savings account can serve [short-term goals or emergency funds](https://www.investor.gov/introduction-investing/). If you’re comparing accounts, review their access rules, costs, insurance coverage, and other terms before deciding.

What if I do not know the exact cost?

Start with a reasonable estimate, note your assumptions, and review the target periodically. For flexible purchases, you can also set a maximum spending limit and adjust what you buy to match the amount saved.

Financial LiteracyBeginnerBudgetingPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team