An annuity is an insurance agreement designed to convert one premium or a series of payments into income now or in the future. That is the clearest answer to “what is an annuity?” and the key to understanding every variation: the buyer commits money under stated terms, and the insurer takes on specific payment obligations. Investor.gov confirms that annuities can be funded with a lump sum or multiple payments and can provide periodic income immediately or later.

What is an Annuity? A Complete Guide

An annuity is an insurance agreement designed to convert one premium or a series of payments into income now or in the future. That is the clearest answer to “what is an annuity?” and the key to understanding every…

15 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

Annuities are often discussed in retirement planning because they can turn part of a person’s savings into scheduled income. But “annuity” is a broad label, not a single standardized deal. The payment timing, growth method, access rules, costs, beneficiary provisions, and insurer obligations depend on the specific contract. This guide is for beginners who want to understand that structure before comparing offers or speaking with a financial professional.

Introduction to Annuities

The purpose of an annuity is easier to understand when it is treated as an income-planning tool rather than a single investment category. A buyer identifies money that can be committed under a contract, chooses when payments should begin, and reviews how the promised benefit fits alongside savings, investments, pensions, or Social Security.

That structure creates a tradeoff. The buyer may gain a more defined income arrangement, but the contract can reduce flexibility and introduce costs or conditions. The right starting point is therefore not “Which annuity has the highest advertised rate?” It is “What financial job needs to be done, and does this contract perform it at an acceptable cost and level of risk?”

How Annuities Work

An annuity has two sides. The buyer contributes money; the insurance company accepts contractual obligations in return. The verified definition from Investor.gov makes clear that funding can happen through a lump sum or a series of payments, while income can begin immediately or at a future date.

That creates a simple three-part framework:

- Funding: You decide how much money to commit and whether the contract accepts one payment or multiple payments.

- Waiting or accumulation: Some contracts are intended to begin paying soon, while others leave time between funding and income.

- Distribution: Payments begin under the schedule and options selected in the contract.

Consider a hypothetical buyer named Maya. She has retirement savings in several places and wants one portion of her future budget to arrive on a schedule. An annuity might let her assign part of her money to that purpose. The useful question is not merely, “How much will it pay?” She also needs to ask when payments start, how long they last, what access she gives up, what the contract costs, and what happens if her plans change.

That example shows why an annuity should be evaluated as a complete contract rather than as an advertised payment figure. Two offers that appear to provide similar income could have materially different conditions.

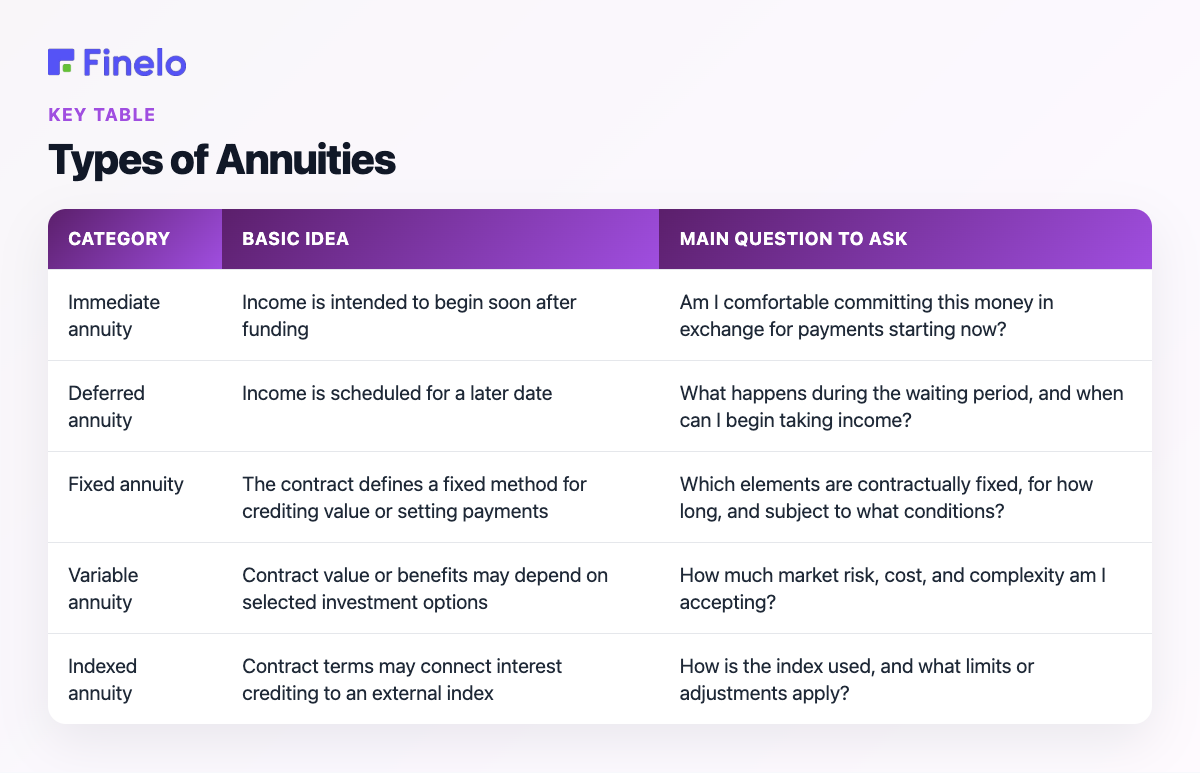

Types of Annuities

Annuities are commonly described along two separate dimensions: when payments begin and how the contract’s value or payments are determined. Keeping those dimensions separate prevents a common misunderstanding. “Immediate” and “deferred” address timing; terms such as “fixed” and “variable” describe a different feature of the contract.

| Category | Basic idea | Main question to ask |

|---|---|---|

| Immediate annuity | Income is intended to begin soon after funding | Am I comfortable committing this money in exchange for payments starting now? |

| Deferred annuity | Income is scheduled for a later date | What happens during the waiting period, and when can I begin taking income? |

| Fixed annuity | The contract defines a fixed method for crediting value or setting payments | Which elements are contractually fixed, for how long, and subject to what conditions? |

| Variable annuity | Contract value or benefits may depend on selected investment options | How much market risk, cost, and complexity am I accepting? |

| Indexed annuity | Contract terms may connect interest crediting to an external index | How is the index used, and what limits or adjustments apply? |

These labels can overlap. A contract can be deferred and fixed, for example, because one word describes payment timing and the other describes how value is determined.

Immediate versus deferred

The choice between immediate and deferred income begins with a practical question: When do you need the payments? Investor.gov explains that immediate annuities are generally purchased with one payment and typically begin paying within a year, while deferred annuities accept one or flexible payments to build money for future income. See the official immediate and deferred annuity overview.

An immediate structure may be relevant to someone who has already reached the point when income is needed. A deferred structure may be considered by someone planning for a later income date. In either case, the contract should state when payments begin. Investor.gov’s definition specifically notes that the insurer’s periodic payments may start immediately or in the future.

The timing decision affects flexibility. Money committed for near-term income serves a different purpose from money that may need to cover an emergency, a major purchase, or an uncertain transition. Before committing funds, separate the amount intended for scheduled future income from the amount that must remain readily accessible.

Fixed, variable, and indexed structures

These terms require careful contract reading because a short category name cannot explain the entire risk-and-return arrangement.

A fixed structure emphasizes contractually defined terms. A variable structure introduces investment choices and uncertainty in value. Investor.gov describes a variable annuity as an insurance contract that also functions as an investment account, may grow on a tax-deferred basis, and can later be converted into periodic payments. Read the official variable annuity explanation.

An indexed structure uses a formula connected in some way to an index, but that does not mean the contract is identical to owning the index. Investor.gov explains that fixed indexed annuity interest is based partly on a specified benchmark, is credited at the end of a specified term, and is not known in advance. See the official explanation of fixed indexed annuities. For any structure, ask what can change, what cannot change, who bears the risk, and how costs affect the outcome.

Avoid choosing solely because one label sounds safer or more rewarding. The meaningful details are found in the actual crediting method, payment formula, restrictions, optional benefits, and insurer promises.

Benefits of Annuities

The central appeal of an annuity is organization: it can assign a defined role to part of a financial plan. Instead of leaving every dollar in a general pool, a buyer may use an annuity to support a future payment objective.

Potential benefits may include:

- Scheduled income: The contract can establish periodic payments, which may make future cash-flow planning easier.

- Choice of payment timing: Depending on the contract, payments can be designed to begin immediately or later.

- Separation of financial goals: A person can distinguish money intended for future income from money kept for near-term spending or emergencies.

- Contract options: Different structures may allow buyers to select among payment, beneficiary, or optional-benefit arrangements.

These are not automatic reasons to buy. Every benefit has a corresponding question. Scheduled income may require reduced access to principal. Optional features may add conditions or costs. A long-term contract may become inconvenient if a buyer’s health, family situation, or spending needs change.

It is also important to distinguish a contract promise from an investment outcome. The value of a promise depends on its exact wording, exclusions, and the insurer responsible for fulfilling it. Read “guaranteed” as an invitation to identify precisely what is guaranteed, by whom, for how long, and under which conditions.

Considerations Before Purchasing an Annuity

The most important annuity risks are often not visible in the advertised benefit. They sit in the contract: charges, withdrawal rules, payment elections, changing rates or formulas, and optional features. Because products vary, a responsible comparison starts with documents rather than assumptions.

Fees and charges

Do not ask only, “What is the annual fee?” An annuity can contain more than one kind of cost. Investor.gov warns that variable annuities carry several fees and expenses that reduce account value and investment return. Review its variable annuity fee guidance. It also distinguishes explicit fees deducted from contract value from harder-to-identify implicit costs, both of which can reduce an annuity’s value. See the broader Investor.gov annuity fee overview. Request a complete list in both percentage and dollar terms where possible, and ask how each charge affects the contract value and future payments.

Use this checklist:

- What charges apply when the contract is purchased or funded?

- Are there ongoing administrative, insurance, investment, or contract charges?

- Does an optional feature add a separate cost?

- Is there a charge for withdrawing or ending the contract?

- Can any charge change, and how would the buyer be notified?

- What is the estimated total cost under a realistic holding period?

The goal is to understand the combined effect. A feature may sound attractive on its own while offering poor value after its cost, restrictions, and likelihood of use are considered together.

Access to your money

Can you access money in an annuity before retirement? The only dependable general answer is: consult the specific contract. Investor.gov says many deferred annuities permit withdrawals during accumulation; removing all the money is commonly called a surrender and ends the annuity, while partial withdrawals may also be possible. Review the official withdrawal and surrender explanation. Access may still be limited, conditioned, or costly, and the rules depend on the contract.

Before buying, ask the insurer to explain these situations in writing:

- A small partial withdrawal

- A large unexpected expense

- Full cancellation or surrender

- Starting income earlier than planned

- Delaying income

- A need to change the beneficiary or payment option

Do not treat “withdrawals allowed” as equivalent to “full, cost-free access.” Ask how much is available, when it is available, what charges or adjustments may apply, and whether the withdrawal changes later benefits. The SEC cautions that some annuities stop allowing withdrawals after regular annuity payments begin. Read the SEC’s variable annuity guide. In the United States, the IRS says pension or annuity payments received before age 59½ may also face an additional 10% tax unless an exception applies. Check the current IRS rule and exceptions.

Tax treatment

“Tax deferred” does not mean “tax free,” and the right tax answer depends on the type of contract, how it was funded, and the nature of the distribution. For payments from a qualified employer retirement plan, the IRS states that all or part of pension or annuity payments may be taxable unless the payment is a qualified distribution from a designated Roth account. See IRS Topic No. 410.

Before purchasing, ask who will report distributions, which portion may be taxable, how withdrawals differ from scheduled payments, and whether state taxes also need to be considered. Tax rules can be detailed and personal, so a qualified tax professional can help apply the current rules to a specific situation.

Inflation and purchasing power

A payment can remain numerically stable while buying less over time. That makes inflation a central planning question, especially when income may continue for many years.

When reviewing a proposal, compare the payment pattern with a range of future living-cost scenarios. If the contract offers a payment that may change over time, identify the exact formula and tradeoff. If it offers a level payment, consider how other parts of the plan might address rising expenses. This is a planning exercise, not a prediction of future inflation.

The insurer’s financial strength

An annuity is an insurance-company contract, so the provider is not a minor detail. Investor.gov notes that the insurer’s obligations depend on its financial strength and claims-paying ability; financial difficulty could impair its ability to pay. Review the official risk explanation. Evaluate the insurer as carefully as the payment illustration.

Ask which legal entity issues the contract, then review its financial information and independent strength assessments. Check whether ratings differ across agencies, understand that ratings can change, and confirm what a rating does—and does not—measure. A sales representative’s confidence is not a substitute for documented due diligence.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

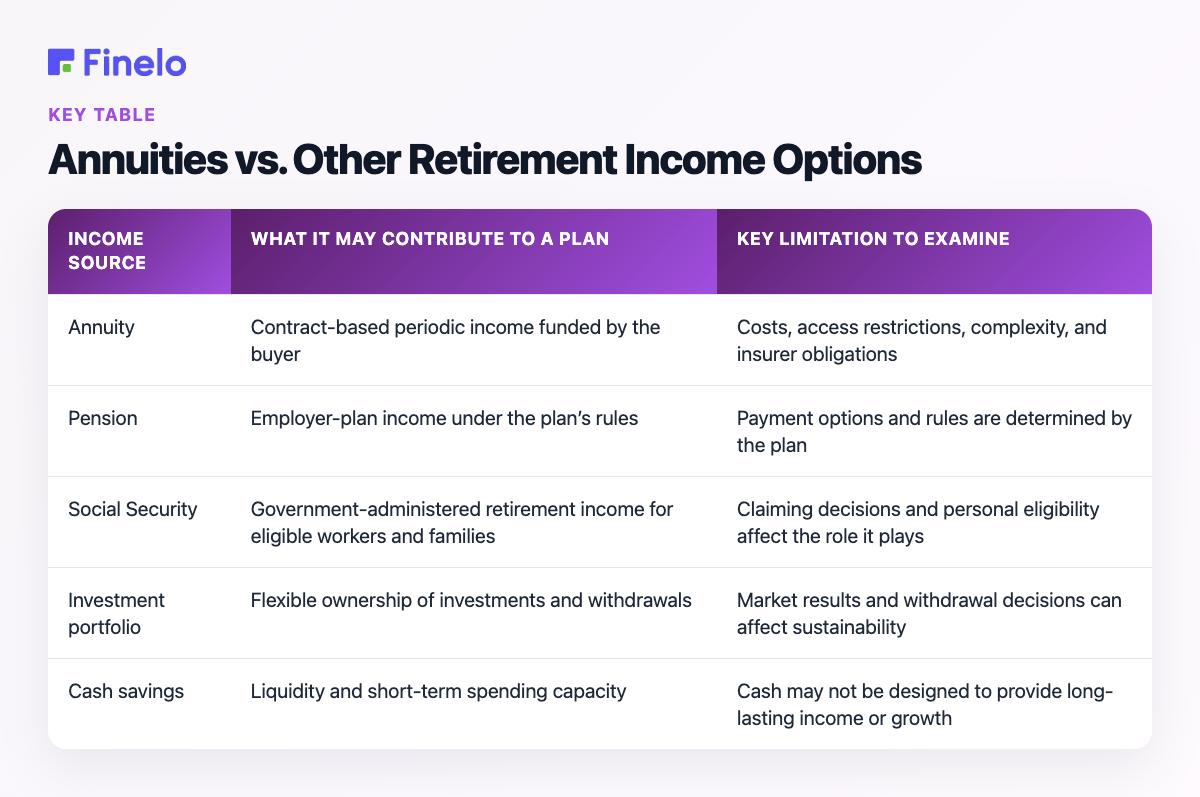

Annuities vs. Other Retirement Income Options

An annuity does not need to be an all-or-nothing choice. It can be compared with other resources based on the job each one performs.

| Income source | What it may contribute to a plan | Key limitation to examine |

|---|---|---|

| Annuity | Contract-based periodic income funded by the buyer | Costs, access restrictions, complexity, and insurer obligations |

| Pension | Employer-plan income under the plan’s rules | Payment options and rules are determined by the plan |

| Social Security | Government-administered retirement income for eligible workers and families | Claiming decisions and personal eligibility affect the role it plays |

| Investment portfolio | Flexible ownership of investments and withdrawals | Market results and withdrawal decisions can affect sustainability |

| Cash savings | Liquidity and short-term spending capacity | Cash may not be designed to provide long-lasting income or growth |

The comparison should focus on gaps rather than labels. Start by listing expected essential expenses and the income sources already available. Then identify which expenses are not covered, how much flexibility is needed, and which risks remain.

For example, Leo expects some income from existing sources but wants more predictability for a portion of his monthly expenses. He could compare using part of his savings for an annuity with leaving all of it invested. The annuity route may increase payment predictability for that portion, while the portfolio route may preserve more control and flexibility. The appropriate balance depends on the actual contract, the rest of his finances, and his tolerance for uncertainty.

Real-Life Case Studies

The following hypothetical cases show how the decision framework can work. They are illustrations, not recommendations or promises of a particular result.

A retiree seeking near-term income

Elena is preparing to retire and wants help covering a predictable part of her regular expenses. She has other money available for emergencies and is considering an immediate annuity for only the portion assigned to that income goal.

Her comparison should start with the proposed payment, but it should not end there. She needs to review whether the payment is fixed or can change, what happens at death, whether any remaining value can pass to a beneficiary, and how inflation could affect the payment’s purchasing power. She should also compare the insurer’s financial strength and the annuity terms with keeping the money in other retirement income options.

A worker planning income for later

Daniel is still working and does not need current payments. A deferred annuity offer may look relevant because the income date is in the future. His key questions are different from Elena’s: how the contract value is determined, which fees apply during the waiting period, whether the rate or other terms can change, and what happens if he needs access before payments begin.

Daniel should compare the offer with the retirement accounts and investments he already has. If the annuity’s main attraction is tax-deferred growth, he should examine the tax treatment carefully rather than assuming “tax deferred” means “tax free.” He also needs enough liquid savings outside the contract to avoid relying on an early withdrawal.

These examples point to the same lesson: a suitable use case begins with a specific job for the money. The product should be evaluated in the context of the buyer’s life, cash-flow needs, taxes, existing income sources, and ability to accept restrictions.

How to Decide Whether an Annuity May Fit

An annuity may be worth investigating when a person has a clear future-income objective, understands that the product is a long-term contract, and can keep adequate liquid resources outside it. It may be a poor fit when flexibility is the overriding priority, the terms are not understood, or the buyer feels pressured to decide quickly.

Use this decision framework before comparing providers:

- Define the job. Write one sentence explaining what the annuity is supposed to accomplish.

- Set the income date. Decide whether the need is immediate or years away.

- Protect liquidity. Identify money that must stay accessible and exclude it from the amount under consideration.

- Compare alternatives. Test whether a simpler combination of savings, investments, or existing income sources could perform the same job.

- Read the contract. Mark every charge, restriction, adjustment, and optional benefit.

- Stress-test the choice. Consider an emergency expense, higher living costs, changed family needs, and a desire to exit early.

- Verify the issuer. Review the insurer’s identity and financial strength.

- Seek an independent explanation. If the contract remains unclear, consult a qualified professional who can explain the tradeoffs in the context of your circumstances.

A useful rule is that complexity should earn its place. If you cannot explain what the contract does, what it costs, when money can be accessed, and what could reduce the expected benefit, more review is needed.

Questions to Ask Before Signing

Bring a written list to any sales or advice conversation. Ask for answers tied to the contract rather than a brochure or verbal summary.

For a variable annuity, the SEC recommends requesting and carefully reading the prospectus because it contains information about fees and charges, investment options, death benefits, and payout options. See the SEC’s investor guidance. The SEC also warns that variable annuity charges reduce account value and investment return, reinforcing the need to compare total costs rather than one advertised feature.

- Which company is legally responsible for the promised benefits?

- Is the annuity immediate or deferred?

- How is the contract’s value determined?

- When can income begin, and what payment choices are available?

- Which terms are guaranteed, and which can change?

- What is the full cost, including optional features?

- What happens if I withdraw part or all of the money?

- How could a withdrawal affect future income or benefits?

- What happens if I die before or after payments begin?

- Can I change payment or beneficiary choices later?

- How does the proposed payment address—or fail to address—inflation?

- What assumptions appear in the illustration?

- What happens if the insurer’s financial condition weakens?

Take time to compare the written answers across offers. Similar product names do not ensure similar terms.

Conclusion and Next Steps

An annuity is best understood as a trade: money and flexibility are committed under a contract in exchange for defined benefits that may include periodic income now or later. Whether that trade is worthwhile depends on the contract’s timing, costs, access rules, risks, and fit with the rest of the buyer’s plan.

Before taking action, write down the income problem you are trying to solve, keep emergency funds separate, compare the annuity with simpler alternatives, and request the full contract and cost disclosure. Use educational resources such as Finelo to build your financial vocabulary, then verify the details with the insurer and an appropriately qualified professional. This article is educational and is not personalized financial advice.

Frequently asked questions

Is an annuity the same as an investment account?

No. An annuity is an insurance-company contract funded by the buyer in exchange for contractual benefits, which may include future periodic payments. Some annuities may contain investment-related elements, but the contract structure, insurer obligations, costs, and access rules remain central.

What happens to an annuity when the owner dies?

It depends on the contract and the choices made when it was established. Ask what happens before payments begin, after payments begin, and under each available beneficiary or payment option. Do not assume that an unused balance automatically passes to heirs.

Can an annuity lose value?

The answer depends on how the contract determines value, the options selected, withdrawals, charges, and other terms. Ask for a clear description of every situation in which the contract value, payment, or benefit could be lower than expected.

Should all retirement savings go into an annuity?

Treating any one product as the entire plan can create concentration and liquidity problems. A better starting point is to decide what portion, if any, has a specific income job while preserving resources for emergencies, flexible spending, and other goals.

Financial LiteracyBeginnerRetirementPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team