Deflation is a broad decline in the overall price level of goods and services. In practical terms, money gains purchasing power: the same amount can buy more than before. That may sound entirely positive, but economy-wide deflation is different from a temporary discount or one product becoming cheaper. If falling prices persist, households may postpone purchases, companies may earn less, and fixed debts may become harder to manage.

What is Deflation? Understanding Its Causes and Effects

Deflation is a broad decline in the overall price level of goods and services. In practical terms, money gains purchasing power: the same amount can buy more than before. That may sound entirely positive, but…

8 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

The key is to look at the whole economy, not a single price. The Federal Reserve describes deflation as a period when the overall level of prices is falling and notes that it has been rare in modern U.S. history (Federal Reserve).

Key takeaways

- Deflation means the broad price level is falling; it is not the same as a sale or slower inflation.

- Weak demand and expectations of further price declines can reinforce one another.

- Lower prices may increase purchasing power, but persistent deflation can make debt harder to repay and weaken jobs and investment.

- Governments and central banks may support demand, although conventional interest-rate cuts have limits.

- Personal and business decisions should be based on cash flow, debt, risk, and time horizon—not a single economic forecast.

What causes deflation?

Deflation generally develops when spending is too weak relative to the economy’s capacity to produce, when the supply of goods and services expands faster than demand, or when money and credit conditions become unusually tight. Several forces can overlap.

-

Falling consumer demand: If households become worried about income or employment, they may cut or delay spending. Businesses then lower prices to attract buyers.

-

Reduced business investment: Companies facing uncertain sales may postpone hiring, expansion, or equipment purchases. That removes another source of demand.

-

Tighter credit: When lenders become more cautious or borrowing becomes difficult, households and businesses may be unable or unwilling to finance purchases.

-

Higher productivity or lower production costs: New technology, more efficient processes, or cheaper inputs can reduce prices. This form of price decline can benefit buyers and efficient producers, especially when demand and incomes remain healthy.

-

Excess capacity: When factories, stores, housing, or other productive resources outnumber willing buyers, sellers may compete by lowering prices.

-

Restrictive monetary conditions: Conditions that constrain money, credit, and spending can contribute to broad downward pressure on prices.

The Federal Reserve specifically identifies persistently weak demand—and expectations that prices will keep falling—as forces that can lead to deflation. It also explains that monetary policy affects demand through financial conditions and inflation expectations (Federal Reserve).

Not every price reduction signals deflation. Electronics, communications, or manufacturing costs may fall because firms become more productive. That can improve value for consumers without producing an economy-wide contraction or recession. Deflation becomes a broader concern when falling prices are persistent and accompanied by weak spending, income, investment, or employment.

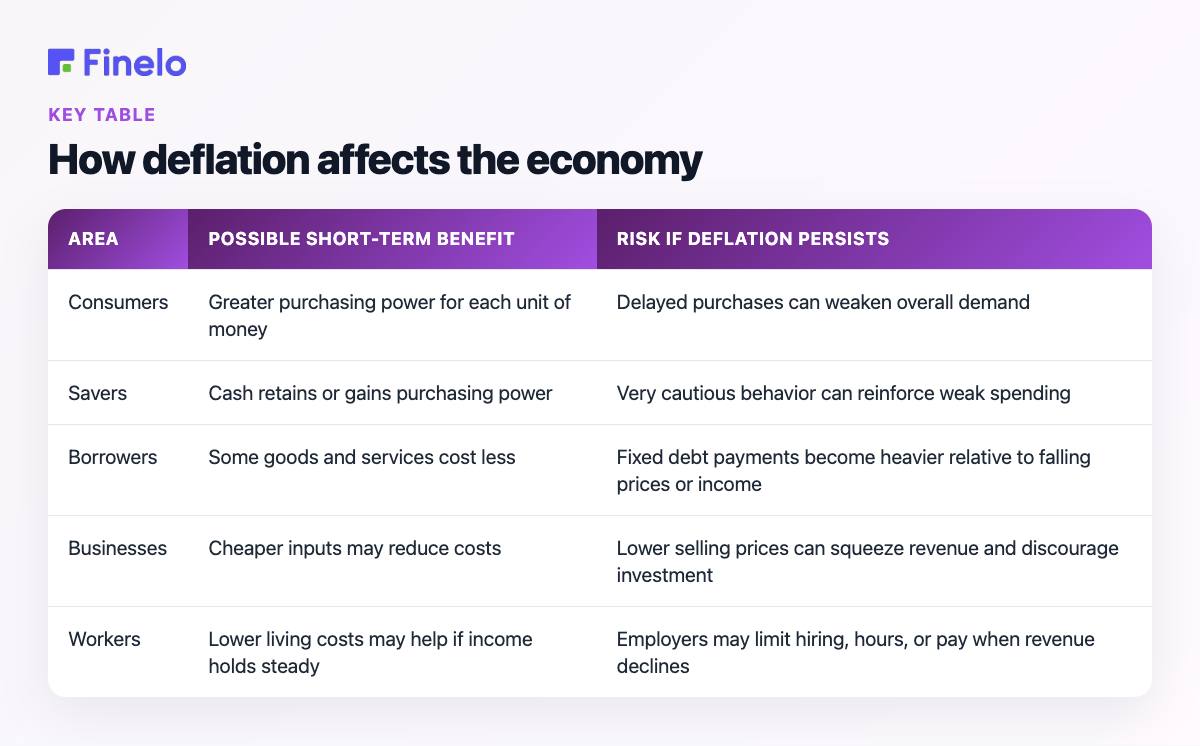

How deflation affects the economy

The effects depend on why prices are falling, how long the decline lasts, and whether wages and incomes are also changing.

| Area | Possible short-term benefit | Risk if deflation persists |

|---|---|---|

| Consumers | Greater purchasing power for each unit of money | Delayed purchases can weaken overall demand |

| Savers | Cash retains or gains purchasing power | Very cautious behavior can reinforce weak spending |

| Borrowers | Some goods and services cost less | Fixed debt payments become heavier relative to falling prices or income |

| Businesses | Cheaper inputs may reduce costs | Lower selling prices can squeeze revenue and discourage investment |

| Workers | Lower living costs may help if income holds steady | Employers may limit hiring, hours, or pay when revenue declines |

For consumers, lower prices can initially feel like a raise. If income stays unchanged while groceries, transportation, or other expenses cost less, purchasing power improves. Yet expectations matter. A buyer who believes a car, appliance, or business asset will be cheaper next month has an incentive to wait. When many people wait at once, sales fall.

Businesses then face a difficult adjustment. They may lower prices to move inventory, but lower prices can reduce revenue. If costs do not fall as quickly, profit margins narrow. A company may respond by delaying investment, reducing production, or limiting hiring—all of which can further weaken demand.

Debt adds another pressure. Loans are normally stated in fixed currency amounts. If prices and incomes fall, the number printed on the debt does not automatically fall with them. A mortgage, business loan, or other obligation can therefore consume a larger share of the borrower’s available income. The Federal Reserve notes that an unexpected fall in the price level can leave firms with fewer dollars to service debt and may restrain job creation and economic activity (Federal Reserve). This is why a period that benefits a cash-rich buyer can be painful for a heavily indebted household or company.

Deflation, disinflation, and ordinary price cuts

These terms are easy to confuse, but they describe different situations.

-

Deflation: The general price level is falling, so the inflation rate is below zero.

-

Disinflation: Prices are still rising, but more slowly than before.

-

A price cut: One company, product, or industry becomes cheaper; the overall price level may still be rising.

For example, if inflation slows from 4% to 2%, that is disinflation, not deflation. If the broad price level declines by 2%, that is deflation (Charles Schwab). Likewise, a cheaper laptop does not prove that the economy is in deflation. Its price may have fallen because production improved or a newer model arrived while rent, food, and services continued to become more expensive.

This distinction matters because disinflation can mean that high inflation is easing, while deflation means the direction of the overall price level has reversed.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

What is a deflationary spiral?

A deflationary spiral is a self-reinforcing cycle in which falling prices weaken spending and income, leading to further price declines. A simplified sequence looks like this:

- Households and businesses reduce spending.

- Sellers lower prices because demand is weak.

- Business revenue and cash flow decline.

- Companies reduce production, investment, or labor costs.

- Income and confidence weaken.

- Spending falls again, restarting the cycle.

Expectations can accelerate the process. If people believe prices will keep falling, waiting seems rational for each individual buyer. Collectively, however, widespread delay removes demand from the economy. Businesses then have more reason to cut prices and costs.

Debt can intensify the loop. When income declines but fixed payments remain, borrowers direct more of their cash toward servicing debt and less toward new purchases. Reduced spending creates additional pressure on business revenue. This does not mean every episode of falling prices becomes a spiral; it explains why policymakers watch persistent, broad deflation more closely than isolated bargains.

Historical examples of deflation

The United States experienced sharp consumer-price declines after World War I and during the first years of the Great Depression, according to the Federal Reserve’s historical overview. These examples illustrate that deflation often appears alongside a major economic adjustment rather than as a simple improvement in affordability.

After World War I

Wartime production and demand patterns changed when the conflict ended. The subsequent price declines show how quickly an economy can shift when spending, production, and financial conditions readjust. The lesson is that a broad fall in prices can be part of a disruptive transition, even though individual consumers may welcome cheaper goods.

The early Great Depression

The early Great Depression is the more severe cautionary example. Falling prices occurred alongside deep economic weakness. Lower selling prices reduced cash coming into farms and businesses, while debts remained denominated in fixed dollar amounts. That combination illustrates the central danger of debt deflation: what matters is not only whether goods become cheaper, but also whether incomes and borrowers’ ability to pay deteriorate.

Historical episodes should not be treated as identical templates for the future. Financial systems, policy frameworks, labor markets, and international trade change over time. Their value is in showing the mechanisms that can connect weak demand, falling prices, debt stress, and lower activity.

How governments and central banks respond

Responses to deflation generally aim to support demand, keep credit functioning, and prevent expectations of falling prices from becoming entrenched.

Central banks may try to make financial conditions more supportive, including by reducing policy interest rates. The intended chain is that easier conditions encourage borrowing, spending, and investment, which can help stabilize demand and prices. Communication also matters: households and businesses make plans partly on what they expect inflation, income, and financing conditions to be.

Governments may use fiscal measures, including changes in public spending or taxes, to support demand. Financial-system measures may also be important when damaged credit channels prevent otherwise viable households and businesses from obtaining financing.

Policy involves tradeoffs. Support that is too weak may fail to interrupt a deflationary cycle, while poorly targeted or prolonged support may create other economic risks. Conventional rate cuts also reach a practical constraint: the Federal Reserve says its ability to counter deflation by cutting the federal funds rate becomes limited once that rate has been reduced to zero (Federal Reserve). The appropriate response depends on the source of the price decline and the condition of employment, credit, production, markets, and public finances.

Practical implications for households and businesses

Deflation is a macroeconomic condition, not a signal that every person should make the same financial move. A useful response begins with resilience rather than a prediction.

For households:

- Separate broad deflation from temporary discounts in a few categories.

- Review whether fixed debt payments would remain manageable if income weakened.

- Keep near-term spending plans tied to needs, cash flow, and affordability—not solely to guesses about future prices.

- Evaluate investments by risk, time horizon, costs, and suitability rather than assuming one asset must benefit from deflation.

For businesses:

- Test budgets against lower selling prices or slower sales.

- Monitor cash flow and debt obligations, not revenue alone.

- Avoid assuming that input costs and wages will fall as quickly as selling prices.

- Focus price reductions where they support a clear inventory or customer strategy instead of entering an uncontrolled discount cycle.

Conclusion: interpreting deflation without overreacting

The most useful takeaway is simple: falling prices can increase purchasing power, but persistent economy-wide deflation can also weaken demand and make fixed debts more burdensome. Look beyond one price or one month of data. Consider whether the decline is broad, whether incomes and employment are weakening, and whether consumers and businesses expect prices to keep falling.

This guide is part of Finelo’s financial education and investment-learning context. It is designed to explain economic concepts, not to provide investment services, predict market returns, or replace advice based on an individual’s circumstances. Readers considering a financial decision should independently review its risks, costs, and suitability.

Frequently asked questions

Is deflation always bad?

No. Lower prices caused by better productivity or lower production costs can benefit consumers and efficient businesses. The greater concern is persistent, broad deflation linked to weak demand, falling income, debt stress, and reduced investment.

How does deflation affect personal finances?

It can increase the purchasing power of cash, but the outcome depends on income and debt. If a person’s income falls while fixed loan payments remain unchanged, the apparent benefit of lower prices may be outweighed by a heavier debt burden.

What is the clearest difference between deflation and disinflation?

With deflation, the broad price level falls. With disinflation, the broad price level continues to rise, but at a slower rate.

Can one industry experience falling prices without economy-wide deflation?

Yes. Competition, innovation, cheaper inputs, or improved production can lower prices in a particular industry while the overall price level continues to rise. Economy-wide deflation requires a broad decline, not an isolated bargain.

Financial LiteracyBeginnerEconomicsPersonal Finance

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Financial Literacy

What is Stagflation? Understanding Its Causes and Effects

Stagflation is an unusual economic condition in which high inflation, weak or stagnant economic growth, and high unemployment occur together. In simple terms, prices keep rising while the economy struggles to expand…

Finelo Team

Financial Literacy

What is Quantitative Easing?

Quantitative easing (QE) is a monetary policy tool in which a central bank buys large amounts of longer-term securities to put downward pressure on long-term interest rates and stimulate the economy. It is generally…

Finelo Team

Financial Literacy

What Is Inflation? Understanding Its Impact on the Economy

Inflation is a broad rise in the prices of goods and services over time. In practical terms, it means the same amount of money buys less than it did before. The key word is “broad”: one product becoming more expensive…

Finelo Team