The difference between qualified and ordinary dividends is their federal tax treatment. Ordinary dividends are included in ordinary income, while qualified dividends meet requirements that allow them to be taxed at lower capital gain rates, according to the IRS. You do not choose the classification yourself: the payer identifies which ordinary dividends are also qualified on Form 1099-DIV. For most investors, the practical task is to check the form, understand how the classification affects taxable income, and use the current tax instructions or professional help when filing.

Qualified vs Ordinary Dividends: What You Need to Know

The difference between qualified and ordinary dividends is their federal tax treatment. Ordinary dividends are included in ordinary income, while qualified dividends meet requirements that allow them to be taxed at…

6 min read

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Want to learn more?

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

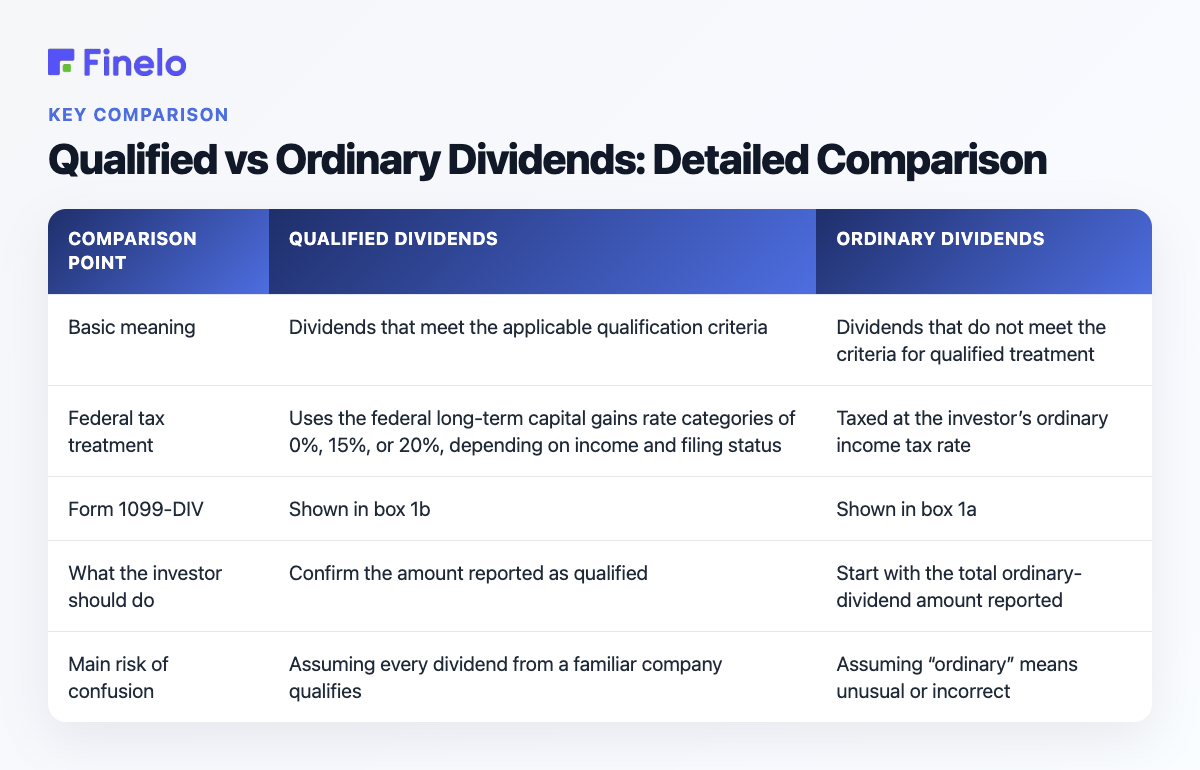

Qualified vs Ordinary Dividends: Detailed Comparison

Both labels describe dividend income, but “qualified” is a tax category within the broader dividend reporting framework.

| Comparison point | Qualified dividends | Ordinary dividends |

|---|---|---|

| Basic meaning | Dividends that meet the applicable qualification criteria | Dividends that do not meet the criteria for qualified treatment |

| Federal tax treatment | Uses the federal long-term capital gains rate categories of 0%, 15%, or 20%, depending on income and filing status | Taxed at the investor’s ordinary income tax rate |

| Form 1099-DIV | Shown in box 1b | Shown in box 1a |

| What the investor should do | Confirm the amount reported as qualified | Start with the total ordinary-dividend amount reported |

| Main risk of confusion | Assuming every dividend from a familiar company qualifies | Assuming “ordinary” means unusual or incorrect |

The key point is that these categories overlap in reporting. The IRS states that the payer must identify which ordinary dividends are also qualified when preparing Form 1099-DIV. In other words, box 1b identifies a qualified portion rather than a completely unrelated stream of income.

What Are Ordinary Dividends?

Ordinary dividends are dividend payments that do not qualify for the lower-rate treatment available to qualified dividends. They are also commonly called nonqualified dividends. Fidelity’s educational explanation states that they are taxed at ordinary income tax rates rather than long-term capital gains rates (Fidelity).

The word “ordinary” refers to tax classification, not the quality of the investment or the importance of the payment. Receiving an ordinary dividend does not, by itself, indicate that anything went wrong. It means the payment is handled as ordinary income for federal tax purposes.

This distinction matters most in a taxable account. Two investors could receive the same dollar amount in dividends but have different tax results if one amount is classified as qualified and the other is ordinary. The actual effect depends on each investor’s broader tax situation, so the classification is an input to the calculation—not a complete estimate of the final tax bill.

What Are Qualified Dividends?

A qualified dividend is an ordinary dividend that meets the applicable IRS criteria. It is eligible for the federal long-term capital gains rate categories of 0%, 15%, or 20%. The rate that applies depends on income and filing status (Fidelity).

For a common stock or ETF dividend, the standard holding-period test is more than 60 days during a 121-day window. That window starts 60 days before the ex-dividend date. Fidelity defines the ex-dividend date as the day the stock or ETF trades without the dividend (Fidelity). Other requirements and exceptions can apply, so holding a stock long enough is necessary but may not be sufficient in every case.

For a quick practical check, look at Form 1099-DIV. Fidelity notes that qualified dividends appear in box 1b, while ordinary dividends appear in box 1a. Investors should avoid trying to reclassify a payment based solely on the company name, the size of the payment, or how long they intended to own the investment.

If the classification seems inconsistent with your records, review the payer’s tax documents and contact the payer before changing the reported amount. Questions involving eligibility criteria or an unusual transaction may warrant help from tax software or a qualified tax professional.

Tax Implications of Qualified vs Ordinary Dividends

Qualified dividends use the 0%, 15%, or 20% federal long-term capital gains rate categories. Ordinary dividends are included in ordinary income and taxed at the investor’s ordinary income tax rate. That makes classification important, but it does not mean qualified dividends are automatically the “better investment.”

Investment quality depends on more than tax treatment. A dividend’s classification does not tell you whether a security fits your goals, what risks it carries, whether its payments will continue, or how its total return may develop. Tax considerations should be evaluated alongside risk, diversification, costs, and suitability.

Consider a simple hypothetical: Investor A and Investor B each receive the same amount of dividends in taxable accounts. Investor A’s entire amount is reported only as ordinary dividends, while part of Investor B’s amount is also reported as qualified. Investor B may receive lower-rate treatment on the qualified portion, while Investor A’s amount remains ordinary income. This example shows why box 1a and box 1b both matter without assuming a particular tax bracket or calculating an unsupported dollar outcome.

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

IRS Reporting Requirements

The payer is responsible for identifying the dividend categories on Form 1099-DIV. The IRS explains that the payer reports which ordinary dividends are also qualified and the amounts distributed.

Use this basic review process:

- Find total ordinary dividends in box 1a.

- Check box 1b for the portion reported as qualified dividends.

- Report box 1a on line 3b of Form 1040 or 1040-SR, as directed by the IRS.

- Report box 1b on line 3a of Form 1040 or 1040-SR (IRS).

- Do not treat boxes 1a and 1b as two unrelated totals. Box 1b identifies the qualified portion within the dividend reporting structure.

- Compare the form with your records and check for corrected tax documents.

Use the instructions for the return you are filing. If the form contains other distribution categories or appears incorrect, consider tax software, the payer’s support team, or a qualified tax professional.

Common misconceptions

“All ordinary dividends are separate from qualified dividends”

Not in the way Form 1099-DIV presents them. The payer identifies which ordinary dividends are also qualified. That is why investors should read boxes 1a and 1b together.

“A qualified dividend is tax-free”

Qualified means eligible for lower capital gain rates, not automatically free from federal tax. The result depends on the taxpayer’s circumstances and the rules applicable to the filing year.

“The lower-tax category is always the better investment”

Tax treatment is only one factor. Choosing an investment solely to seek a particular dividend classification can overlook business risk, concentration, fees, volatility, and whether the investment suits the investor’s objectives.

“I can determine the category from the payment alone”

The amount of a dividend does not establish its classification. Start with the payer’s Form 1099-DIV and investigate discrepancies rather than guessing.

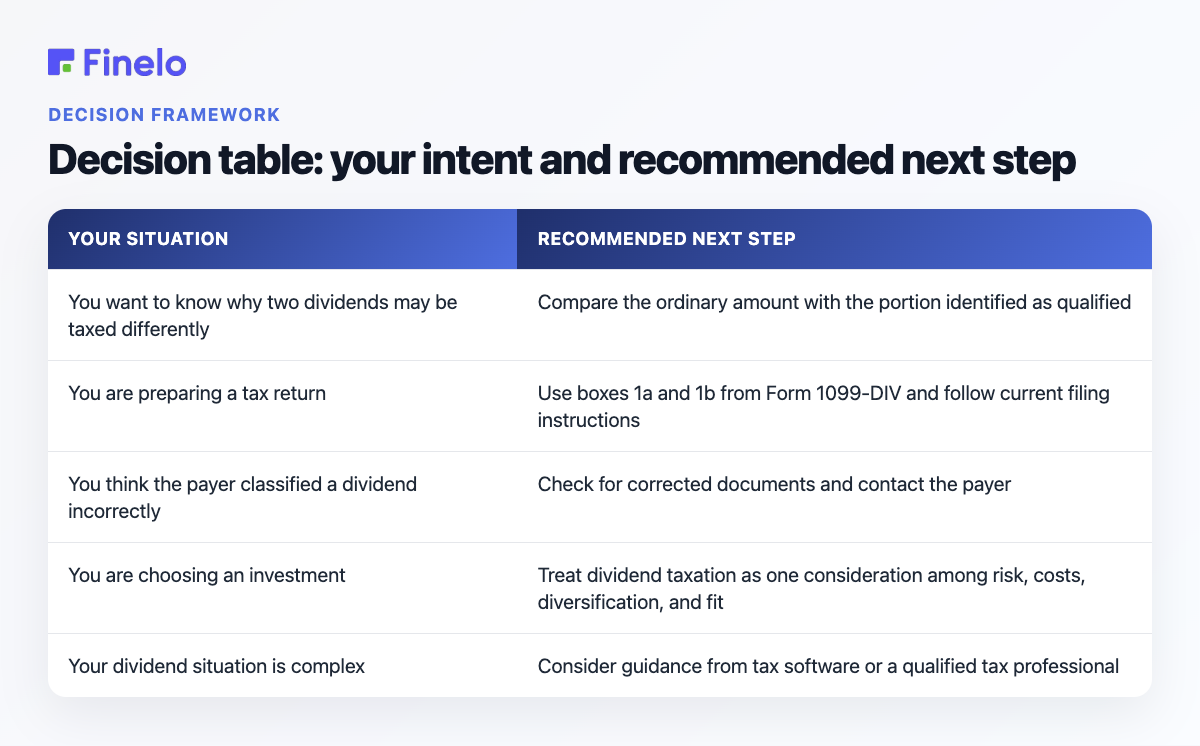

Decision table: your intent and recommended next step

| Your situation | Recommended next step |

|---|---|

| You want to know why two dividends may be taxed differently | Compare the ordinary amount with the portion identified as qualified |

| You are preparing a tax return | Use boxes 1a and 1b from Form 1099-DIV and follow current filing instructions |

| You think the payer classified a dividend incorrectly | Check for corrected documents and contact the payer |

| You are choosing an investment | Treat dividend taxation as one consideration among risk, costs, diversification, and fit |

| Your dividend situation is complex | Consider guidance from tax software or a qualified tax professional |

This comparison is especially useful for beginners reviewing brokerage tax forms and for investors estimating how taxable dividend income may be treated. Finelo provides educational explanations to help readers understand investing concepts, but this page is not individualized tax or investment advice.

Conclusion and Next Steps

Start with your latest Form 1099-DIV, compare boxes 1a and 1b, and flag any amount that does not match your records. Then use the filing instructions for the relevant tax year. When evaluating future investments, remember the central distinction: ordinary dividends are included in ordinary income, while qualified dividends meet criteria for lower capital gain rates. Use that knowledge as one part of a broader, risk-aware investment decision.

Frequently asked questions

Are qualified dividends also ordinary dividends?

The reporting categories can overlap. The IRS says the payer identifies which ordinary dividends are also qualified, and Fidelity explains that box 1b shows qualified dividends while box 1a shows ordinary dividends.

What happens if a dividend does not meet the qualification rules?

It is treated as an ordinary, or nonqualified, dividend and taxed at ordinary income tax rates rather than the lower capital gain rates available to qualified dividends.

How can I tell which type I received?

Check Form 1099-DIV. Qualified dividends are listed in box 1b, while ordinary dividends are listed in box 1a ([Fidelity](https://www.fidelity.com/learning-center/trading-investing/qualified-dividends)).

Should I choose investments based on dividend tax treatment?

Tax treatment can affect after-tax income, but it should not be the only decision criterion. Review the investment’s risks, costs, diversification role, and suitability, and seek professional guidance when your tax situation requires it.

InvestingBeginnerDividendsMarkets

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Investing

Working Capital: What It Tells Investors About Liquidity

Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day…

Finelo Team

Investing

What is Venture Capital?

Venture capital (VC) is money invested in young businesses in exchange for equity, or an ownership stake. It is generally aimed at startups and early-stage companies that need capital to develop a product, hire people…

Finelo Team

Investing

What Is the S&P 500? A Complete Overview

The S&P 500 is a stock market index designed to show how a broad group of leading large-cap U.S. companies is performing. Rather than checking hundreds of stocks individually, investors can look at the index for a…

Finelo Team