A derivative is a financial instrument whose value depends on something else, called the underlying. The underlying might be a stock, commodity, currency, interest rate, market index, or another measurable reference. Investor.gov describes derivatives as instruments whose performance is derived, at least partly, from an underlying asset, security, or index; a stock option is one example because its value changes with the underlying stock’s price (Investor.gov).

What is a Derivative in Finance?

A derivative is a financial instrument whose value depends on something else, called the underlying. The underlying might be a stock, commodity, currency, interest rate, market index, or another measurable reference…

8 min read

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Want to learn more?

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

Derivatives can help manage risk, but they can also create substantial losses. Understanding the contract, payoff, costs, and worst-case outcome matters more than memorizing the terminology.

How derivatives work

A derivative establishes rules for how two parties will exchange value. Those rules may specify:

- The underlying asset or reference

- The contract size

- A price, rate, or other threshold

- An expiration or settlement date

- Whether a party has a right or an obligation

- How the contract will be settled

The connection between the derivative and its underlying is the key idea:

Underlying value changes → contract payoff changes → derivative value changes

Imagine a contract linked to a stock currently priced at $50. The contract might give its buyer the right to purchase the stock for $55 during the next three months. If the stock remains below $55, that right may not be useful. If the stock rises well above $55, the right becomes more valuable. The derivative does not need to represent ownership of the stock itself; it represents a contractual payoff linked to the stock.

Derivative prices may also respond to more than the current underlying price. Time remaining, expected volatility, interest rates, and the likelihood that a counterparty can meet its obligation can all matter, depending on the contract.

Rights, obligations, and settlement

The words right and obligation are crucial. An option buyer generally acquires a right, while a futures or forward contract generally creates obligations for both sides. That difference changes the possible payoff and risk.

Settlement can occur through delivery of the underlying or through a cash payment based on the contract’s terms. Before entering any derivative, a participant should know what triggers settlement, when it occurs, and whether the position can require additional funds along the way.

The main types of derivatives

Four broad categories provide a useful starting point: forwards, futures, options, and swaps. Individual contracts can be customized or structured in more complicated ways, but these categories explain many common derivative relationships.

| Type | Basic structure | Typical purpose | Central risk question |

|---|---|---|---|

| Forward | Two parties agree today on a future transaction | Lock in a future price or rate | Can both parties fulfill the agreement? |

| Futures | A standardized future transaction with ongoing position requirements | Hedge or take a view on a market | How large could losses and funding needs become? |

| Option | The buyer pays for a right to buy or sell under stated terms | Limit, transfer, or take selected price risk | What is the maximum loss for each side? |

| Swap | Parties exchange cash flows under an agreed formula | Change exposure to rates, currencies, or other references | How do market moves and counterparty risk interact? |

Forwards

A forward is a private agreement to transact later at terms set today. Consider a hypothetical coffee roaster that expects to buy beans in three months. It could agree with a supplier on a price now. If market prices rise, the agreed price helps protect the roaster’s budget. If prices fall, the roaster may still be required to pay the higher contracted price.

The hedge reduces one uncertainty but introduces trade-offs. The roaster gives up the benefit of a favorable price move, and each party depends on the other to perform.

Futures

Futures apply a similar future-price concept through standardized contracts. Their standardization can make positions easier to compare and trade, but it does not make them simple or low-risk.

Suppose a farmer is concerned that the selling price of a crop could fall before harvest. A futures position designed to gain value when the crop price falls could offset part of the lower cash-market revenue. If prices instead rise, the hedge may lose value while the crop earns more. A well-designed hedge aims to reduce the combined uncertainty, not maximize the profit of each position separately.

Options

An option gives its buyer a contractual right under specified conditions. A call relates to buying the underlying; a put relates to selling it. The buyer pays a premium for that right.

For example, an investor who owns a stock might buy a put with a strike price below the current share price. If the stock declines sharply, the put may offset part of the loss. If the stock does not fall, the put may expire unused, and the premium remains a cost of protection.

Option sellers face a different payoff. Receiving a premium can come with a potentially large obligation, so the buyer’s limited premium cost should never be mistaken for a statement that all option strategies have limited risk.

Swaps

A swap is an agreement to exchange cash flows according to a formula. A business with payments tied to a changing interest rate might use a swap to exchange that floating exposure for payments based on a fixed rate. Another business may prefer the opposite exposure.

The swap changes how risk is distributed; it does not make risk disappear. The result depends on the contract terms, future market conditions, and each party’s ability to perform.

Why derivatives are used

The same derivative can serve different goals depending on the position and the participant’s existing exposure.

Hedging

Hedging means taking a position intended to offset another risk. A producer may hedge against falling output prices, an importer may hedge against an unfavorable currency move, and a borrower may seek to reduce uncertainty around interest costs.

A practical hedge begins with the exposure, not the product:

- Identify the risk in plain language.

- Estimate its size and timing.

- Choose a derivative linked closely enough to that risk.

- Compare the hedge’s potential benefit with its cost and new risks.

- Decide how the position will be monitored and closed or settled.

Hedges are often imperfect. The contract may expire on a different date, track a related rather than identical underlying, or cover only part of the exposure. That mismatch is one reason a hedge can reduce risk without eliminating it.

Speculation

A speculator uses a derivative to take a view on price direction, volatility, rates, or another market outcome without necessarily holding an offsetting business or investment exposure. Derivatives may create a large economic exposure relative to the initial amount paid or posted. That leverage can amplify gains, but it can also amplify losses.

Adjusting portfolio exposure

Derivatives can also change exposure without immediately buying or selling every underlying holding. A participant might seek temporary market exposure, protection over a limited period, or a different pattern of possible gains and losses. Whether that adjustment is appropriate depends on the full portfolio and the contract’s terms, not on the derivative in isolation.

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

Risks to understand before trading derivatives

Derivative risk is not limited to predicting whether a market will rise or fall. A sound review considers several ways a position can fail.

Market risk. The underlying price, rate, volatility, or other reference may move against the position. A move can be damaging even if the participant’s long-term view later proves correct, because the contract may expire first.

Leverage risk. A relatively small initial payment or deposit can control a much larger exposure. This magnifies sensitivity to market moves and may cause losses to accumulate quickly.

Liquidity risk. It may be difficult or expensive to exit a position at a reasonable price, particularly during stressed markets or in a customized contract.

Counterparty risk. One party may fail to make a required payment or otherwise honor the agreement. Contract structure and settlement arrangements can affect this risk but do not justify ignoring it.

Funding risk. Some positions can require additional cash while they remain open. A participant may be forced to close a position at a poor time if those demands cannot be met.

Basis risk. A hedge and the exposure it is intended to protect may not move in exact opposition. Differences in timing, location, quality, or reference prices can weaken the hedge.

Complexity risk. Small differences in strike price, expiration, settlement method, or embedded conditions can materially change a payoff. If the worst-case outcome cannot be explained clearly, the position is not yet understood.

Operational and legal risk. Errors in execution, recordkeeping, valuation, or contract interpretation may create losses or disputes. Customized agreements deserve especially careful review.

Before trading, write down the maximum plausible loss, the circumstances that could produce it, any additional funding that might be required, and the exit plan. If those answers are unclear, pausing is a risk-management decision.

How derivatives are regulated

Derivatives do not all trade in the same place or under one identical framework. The relevant rules can depend on the product, underlying, trading venue, participant, and jurisdiction. Some contracts are standardized and traded through organized markets; others are privately negotiated.

For an individual, the practical lesson is straightforward: verify who provides the product, where and how it trades, what disclosures apply, how customer assets or collateral are handled, and what happens if a party defaults. Regulation can establish market rules and oversight, but it does not prevent investment losses or make a complex product suitable for every person.

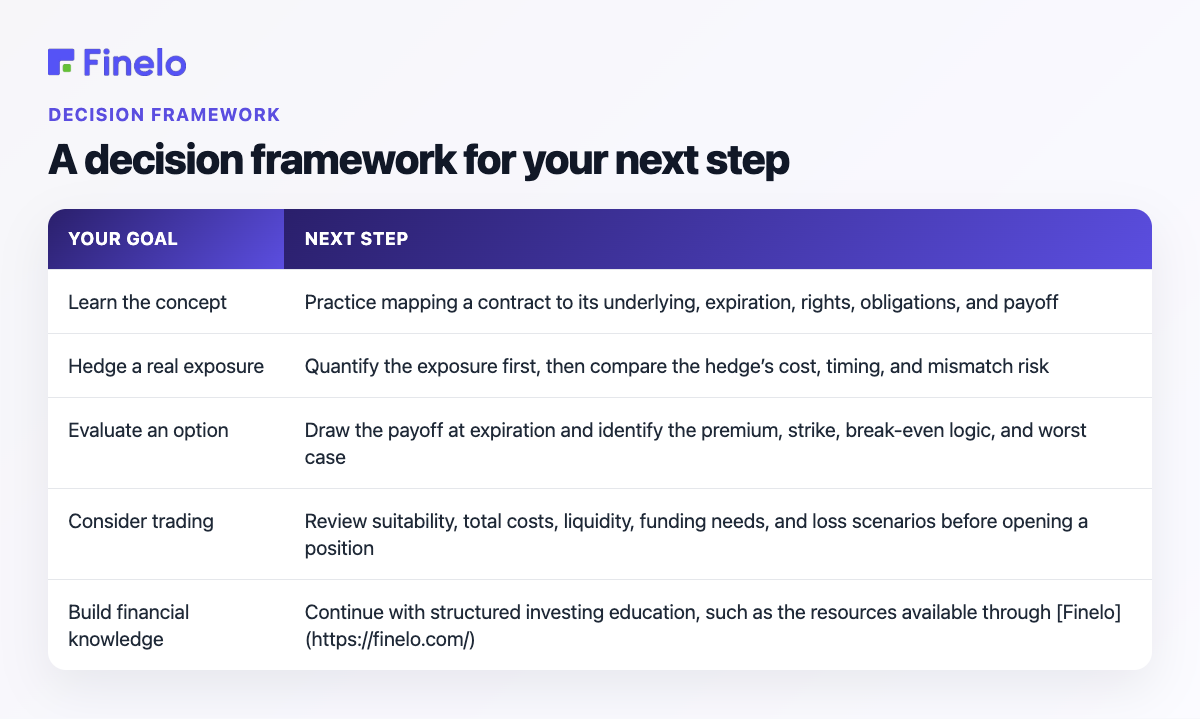

A decision framework for your next step

This article is for beginners who want to understand derivative terminology before considering a course, strategy, or trade. Use the table below to match your goal with a sensible next action.

| Your goal | Next step |

|---|---|

| Learn the concept | Practice mapping a contract to its underlying, expiration, rights, obligations, and payoff |

| Hedge a real exposure | Quantify the exposure first, then compare the hedge’s cost, timing, and mismatch risk |

| Evaluate an option | Draw the payoff at expiration and identify the premium, strike, break-even logic, and worst case |

| Consider trading | Review suitability, total costs, liquidity, funding needs, and loss scenarios before opening a position |

| Build financial knowledge | Continue with structured investing education, such as the resources available through Finelo |

The best short answer to “what is a derivative in finance?” is: a derivative is a financial instrument whose value is linked to an underlying asset, rate, index, or other reference. Its usefulness and danger both come from the same feature—the contract can reshape an existing exposure or create a new one.

Frequently asked questions

Are derivatives the same as stocks?

No. A stock represents an ownership interest in a company. A derivative is a financial instrument linked to an underlying asset or reference. A stock can itself be the underlying for a derivative such as a stock option.

What is the difference between hedging and speculation?

Hedging starts with an existing risk and seeks to offset it. Speculation deliberately takes market risk in pursuit of a favorable outcome. The same contract could be a hedge for one participant and a speculative position for another.

Can a derivative lose more than the initial payment?

It depends on the structure and the participant’s side of the contract. Some buyers may have a known upfront cost, while other positions can create additional obligations or losses beyond the initial amount. Always evaluate the specific payoff rather than applying one risk rule to every derivative.

How should a beginner learn about derivatives?

Start by studying one simple contract at a time. Identify the underlying, contract size, expiration, settlement method, rights and obligations, possible outcomes, and total costs. Paper examples can help reveal misunderstandings without putting money at risk. This material is educational, not personalized financial advice; verify whether any product is appropriate for your circumstances before acting.

TradingBeginnerDerivativesMarkets

Practice trading with Finelo

Practice in a simulator, learn with bite-sized lessons, and build confidence before risking real money.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Trading

What is Swing Trading? A Complete Guide

Swing trading is a short-term approach in which a trader holds a position for several days or weeks while trying to capture part of a price move. The goal is not to predict every fluctuation. It is to identify a…

Finelo Team

Trading

What is Slippage in Trading?

Slippage in trading is the gap between the price you expected when placing a trade and the price at which it is ultimately executed. The U.S. Securities and Exchange Commission describes price slippage as the…

Finelo Team

Trading

What is Quantitative Trading?

Quantitative trading, often called quant trading, is a method of making trading decisions with data, mathematical models, and predefined rules. A trader develops a hypothesis, translates it into measurable conditions…

Finelo Team