A fiduciary is a person or organization trusted to act for someone else and put that person’s interests first within the scope of their relationship. In financial advice, the concept is more than a promise to be helpful: the SEC describes an investment adviser’s fiduciary duty as including a duty of care, a duty of loyalty, and an overarching obligation to act in the client’s best interest.

What is a Fiduciary? Understanding Roles and Responsibilities

A fiduciary is a person or organization trusted to act for someone else and put that person’s interests first within the scope of their relationship. In financial advice, the concept is more than a promise to be…

5 min read

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Want to learn more?

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

The details depend on the role, agreement, and applicable law. That is why “Are you a fiduciary?” is a useful opening question—but not the only question to ask.

What does a fiduciary do?

A fiduciary is expected to use entrusted authority for its intended purpose. The practical responsibilities usually center on three ideas:

- Care: Make decisions thoughtfully, using relevant and sufficiently complete information.

- Loyalty: Put the beneficiary’s or client’s interests ahead of competing personal interests.

- Clarity: Explain the relationship, important limitations, costs, and conflicts in a way the other person can understand.

Consider a financial adviser reviewing two possible investments. A careful analysis would look beyond a single feature such as cost and consider how each choice fits the client’s objectives and circumstances. Loyalty also matters: if one option benefits the adviser financially, that incentive creates a conflict that should be addressed rather than quietly steering the recommendation.

Fiduciary responsibility does not mean guaranteeing a good result. A decision can be reasonable when made and still turn out poorly. The central question is whether the fiduciary followed the required standard while making and carrying out the decision.

Who can be a fiduciary?

“Fiduciary” is a description of a relationship, not one universal job title. Depending on the circumstances, fiduciary roles may arise in financial advice, trust administration, estate matters, business leadership, guardianship, or professional representation.

Common examples include:

- An investment adviser serving a client

- A trustee managing trust property for beneficiaries

- An executor handling an estate

- An attorney acting for a client

- A person authorized to manage another person’s affairs

- Certain corporate leaders acting for an organization and its owners

The title alone does not settle the issue. The person may owe fiduciary duties only for particular services or decisions. For example, someone offering several financial services could act in different capacities at different times. Ask for a written explanation of the capacity in which the person is acting for the specific service you need.

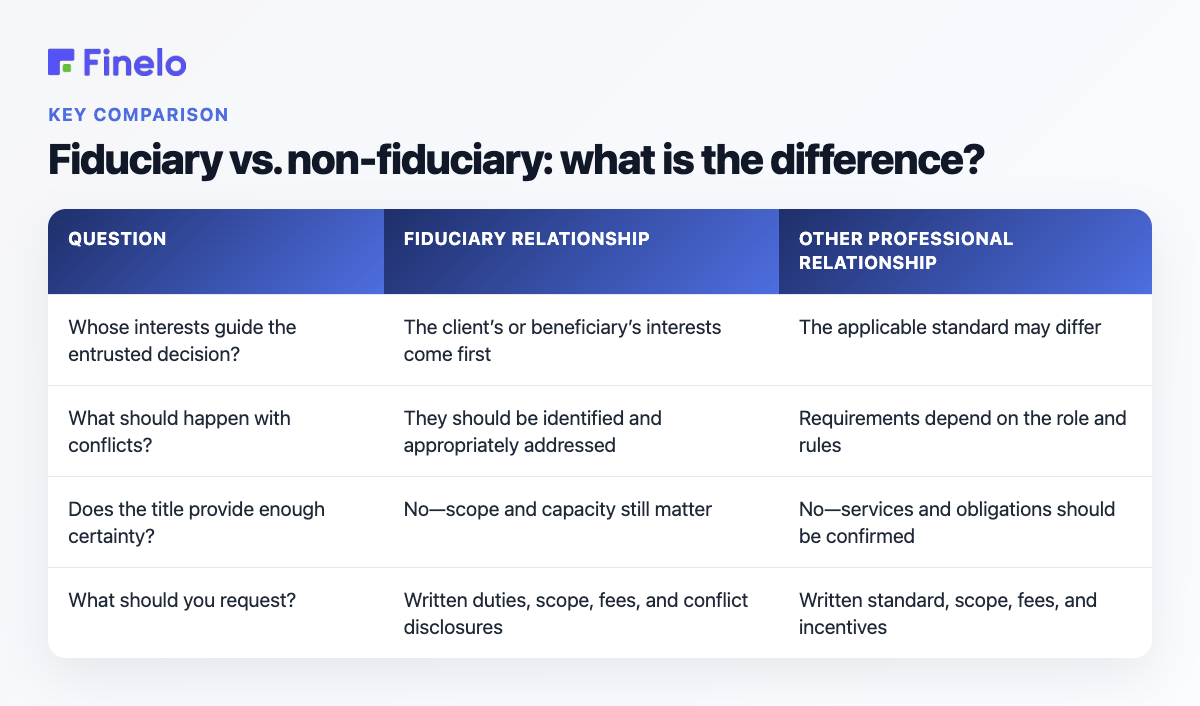

Fiduciary vs. non-fiduciary: what is the difference?

The clearest distinction is whose interests must guide the decision. A fiduciary relationship places the beneficiary’s or client’s interests at the center of the entrusted task. Another professional may still have contractual, ethical, or regulatory obligations without owing the same fiduciary duties in every interaction.

| Question | Fiduciary relationship | Other professional relationship |

|---|---|---|

| Whose interests guide the entrusted decision? | The client’s or beneficiary’s interests come first | The applicable standard may differ |

| What should happen with conflicts? | They should be identified and appropriately addressed | Requirements depend on the role and rules |

| Does the title provide enough certainty? | No—scope and capacity still matter | No—services and obligations should be confirmed |

| What should you request? | Written duties, scope, fees, and conflict disclosures | Written standard, scope, fees, and incentives |

This comparison is not a ranking of every professional. A non-fiduciary relationship is not automatically dishonest or unsuitable. It simply means you should understand the standard that applies before relying on the person’s recommendation or authority.

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Common conflicts of interest

A conflict exists when another interest could pull a fiduciary away from objective judgment. Typical situations can include compensation tied to a particular choice, benefits from recommending an affiliated provider, personal use of entrusted assets, or responsibilities to two parties whose interests do not align.

Imagine a trustee considering hiring a company owned by a relative. Even if that company could do the work, the family connection raises an obvious question about impartiality. A sound process would bring the relationship into the open and handle it according to the trust terms and applicable requirements.

When evaluating a potential conflict, ask:

- What incentive or competing obligation exists?

- Could it influence the recommendation or decision?

- Has it been clearly disclosed?

- How will it be avoided, reduced, or otherwise addressed?

- Is there a reasonable alternative with fewer conflicts?

Disclosure matters, but it should not become a substitute for careful judgment.

How to choose a fiduciary

Start by matching the person’s experience to the task. Someone qualified for investment management may not be the right choice for estate administration, and a family member may be trustworthy without having the time or expertise to manage complex responsibilities.

Use this checklist before agreeing:

- Ask whether the person will act as a fiduciary for the specific service at all times.

- Request the answer in writing, including the scope and duration of the duty.

- Confirm qualifications, relevant experience, and any disciplinary history through appropriate official records.

- Ask how the person is paid and calculate the total costs you may bear.

- Request a plain-language list of material conflicts and how they are handled.

- Clarify who will actually make decisions and whether work can be delegated.

- Understand how performance, decisions, and expenses will be reported.

- Review how you can end the relationship or raise a complaint.

Pay attention to the quality of the answers. Clear, specific responses are more useful than a simple “yes.” If the arrangement is important or difficult to understand, consider getting independent legal or financial guidance before signing.

What happens when fiduciary duty is breached?

A breach may occur when a fiduciary acts disloyally, handles the entrusted matter carelessly, hides a material conflict, or uses authority for an improper benefit. The consequences depend on the facts, governing documents, jurisdiction, and type of relationship. Possible responses can include removing the fiduciary, seeking repayment or other remedies, filing a complaint with an appropriate regulator or professional body, or pursuing legal action.

For example, suppose a person managing entrusted funds secretly directs business to an entity they own on unfavorable terms. The problem is not merely that the investment performed badly; it is the undisclosed personal benefit and failure to put the beneficiary’s interests first.

If you suspect a breach, preserve agreements, statements, messages, invoices, and notes from conversations. Avoid making accusations based only on a disappointing outcome. A qualified professional can help distinguish poor performance from conduct that may violate an actual duty.

Your next step

The best short answer to “what is a fiduciary?” is: someone entrusted to act for another person who must put that person’s interests first within the agreed scope of the relationship.

Before hiring or appointing one, identify the exact task, ask what legal or professional standard applies, and get the duties, fees, authority, and conflicts in writing. This article is educational and does not replace advice tailored to your situation.

Frequently asked questions

Is every financial adviser a fiduciary?

Do not assume the answer from a title alone. Ask whether the adviser will act as a fiduciary for your specific service, whether that duty applies throughout the relationship, and where the obligation is documented.

Can a family member be a fiduciary?

Potentially, if the role and governing arrangement place fiduciary responsibilities on that person. Trustworthiness is important, but so are competence, available time, impartiality, and the ability to keep records.

Does a fiduciary have to choose the cheapest option?

Not necessarily. Cost can be important, but a responsible decision may also consider objectives, risks, services, and other relevant circumstances. The goal is a well-supported decision in the client’s or beneficiary’s best interest, not an automatic choice based on one factor.

How do I know whether a fiduciary is acting in my best interest?

Look for a documented process: clear reasoning, appropriate investigation, transparent costs, disclosed conflicts, regular reporting, and decisions connected to your stated objectives. Ask questions whenever the explanation is incomplete or inconsistent.

InvestingBeginnerInvestor ProtectionMarkets

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Investing

Working Capital: What It Tells Investors About Liquidity

Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day…

Finelo Team

Investing

What is Venture Capital?

Venture capital (VC) is money invested in young businesses in exchange for equity, or an ownership stake. It is generally aimed at startups and early-stage companies that need capital to develop a product, hire people…

Finelo Team

Investing

What Is the S&P 500? A Complete Overview

The S&P 500 is a stock market index designed to show how a broad group of leading large-cap U.S. companies is performing. Rather than checking hundreds of stocks individually, investors can look at the index for a…

Finelo Team