EBITDA stands for earnings before interest, taxes, depreciation, and amortization. It starts with net income and adds back those four categories to show earnings before financing choices, taxes, and certain accounting charges. Investors may encounter it in earnings releases, valuation multiples, debt discussions, and acquisition analysis. The U.S. Securities and Exchange Commission (SEC) identifies “earnings” in EBITDA as net income presented under generally accepted accounting principles (GAAP).

EBITDA Explained: How Investors Use It—and Its Limits

EBITDA stands for earnings before interest, taxes, depreciation, and amortization. It starts with net income and adds back those four categories to show earnings before financing choices, taxes, and certain accounting…

7 min read

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Want to learn more?

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

For a beginner investor, EBITDA is best treated as one comparison tool—not a verdict on profitability or value. It can help examine operating performance across businesses with different debt, tax, or asset profiles, but it is not the same as cash flow and can look strong even when capital spending or debt creates pressure.

How to calculate EBITDA

There are two common routes to the same basic result.

Starting with net income:

EBITDA = Net income + Interest + Taxes + Depreciation + Amortization

Starting with operating income:

EBITDA = Operating income + Depreciation + Amortization

The second formula works when operating income already appears before interest and taxes. In either case, use figures covering the same reporting period and check how the company labels each line item.

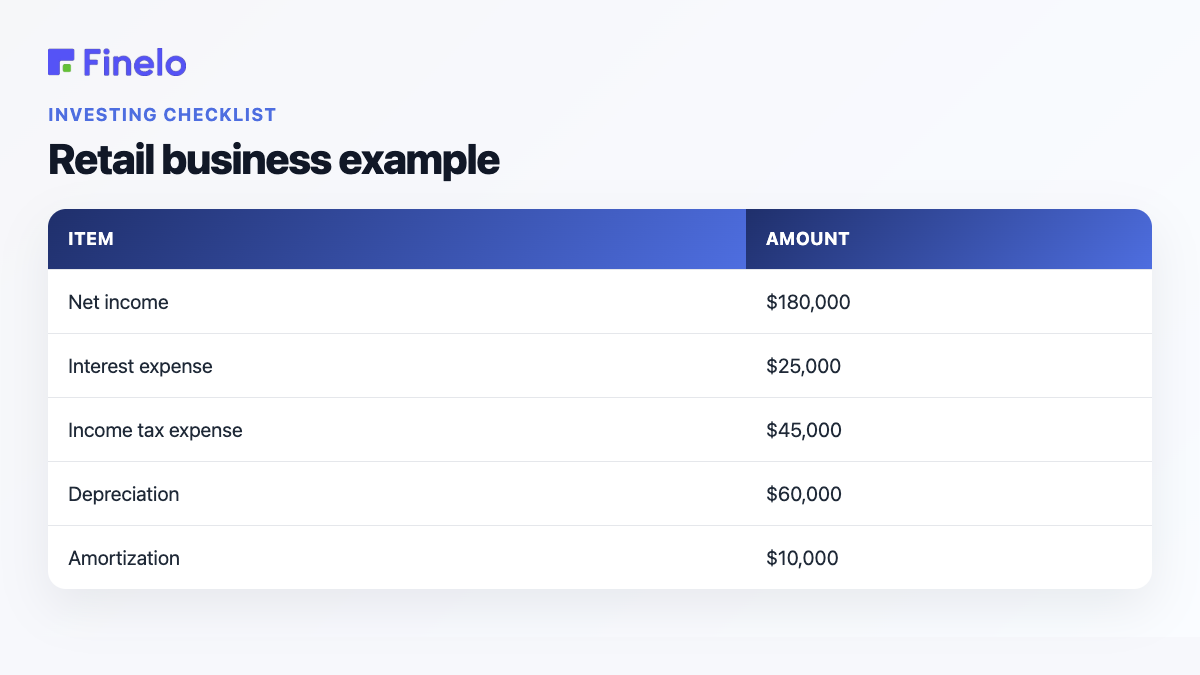

Retail business example

Imagine a hypothetical retailer reports the following annual figures:

| Item | Amount |

|---|---|

| Net income | $180,000 |

| Interest expense | $25,000 |

| Income tax expense | $45,000 |

| Depreciation | $60,000 |

| Amortization | $10,000 |

Its EBITDA would be:

$180,000 + $25,000 + $45,000 + $60,000 + $10,000 = $320,000

The calculation does not mean the retailer generated $320,000 of cash. It means the business recorded $320,000 in earnings before the specified items. Inventory purchases, supplier payments, equipment spending, loan repayments, and other cash movements still matter.

EBITDA margin

EBITDA margin puts the figure in the context of revenue:

EBITDA margin = EBITDA ÷ Revenue × 100

If the hypothetical retailer generated $2 million in revenue, its EBITDA margin would be 16%. A margin is often more useful than a raw amount when comparing periods or differently sized businesses. Even then, the comparison is meaningful only if the companies calculate EBITDA consistently and operate under reasonably similar conditions.

Why EBITDA Matters to Investors

EBITDA helps separate operating results from several factors that can obscure comparisons.

- Financing: Two similar businesses may have different interest costs because one uses more debt.

- Tax circumstances: Tax expenses can differ because of location, legal structure, or prior-period tax items.

- Asset accounting: Depreciation and amortization can vary with the age and composition of a company’s assets.

- Scale: EBITDA margin can help place earnings in the context of revenue.

This makes the metric a useful starting point for asking whether a change came from the underlying business or from financing, tax, or accounting effects. For example, rising EBITDA alongside flat revenue might prompt an analyst to investigate better pricing, a lower cost base, or a change in how management calculated the metric. Falling EBITDA could lead to questions about demand, gross margin, staffing, rent, or other operating expenses.

For investors, the key word is starting. EBITDA can reveal a useful operating pattern, but net income, cash flow, debt, capital expenditures, and the calculation notes are needed to understand the fuller financial picture.

EBITDA in business valuation

Business valuations sometimes express value as a multiple of EBITDA. In a simplified illustration, if a buyer applies a 5× multiple to $1 million of EBITDA, the implied enterprise value would be $5 million.

That arithmetic is straightforward; selecting an appropriate multiple is not. The multiple may reflect growth expectations, risk, customer concentration, recurring revenue, competitive position, asset needs, and the quality of the financial records. A higher EBITDA does not automatically justify a higher multiple, and a multiple observed for one business may be unsuitable for another.

Hypothetical acquisition case

Suppose a buyer is reviewing two retailers:

- Retailer A reports EBITDA of $900,000.

- Retailer B reports EBITDA of $1 million.

At first glance, Retailer B appears stronger. Due diligence then shows that B excluded a recurring annual expense of $180,000 from its adjusted figure, while A made no comparable adjustment. Restoring that expense would reduce B’s adjusted amount to $820,000.

The lesson is not that all adjustments are inappropriate. It is that a buyer must understand every add-back, test whether it is genuinely non-recurring, and calculate both businesses on a consistent basis before applying a valuation multiple.

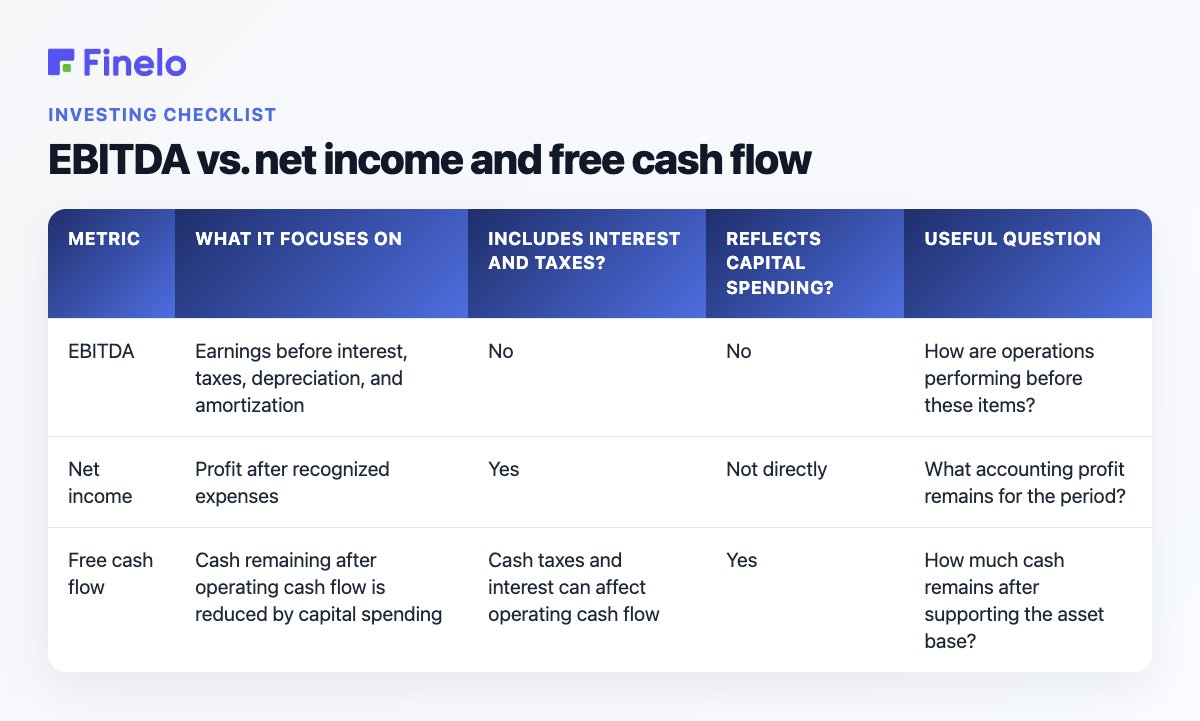

EBITDA vs. net income and free cash flow

No single metric answers every financial question.

| Metric | What it focuses on | Includes interest and taxes? | Reflects capital spending? | Useful question |

|---|---|---|---|---|

| EBITDA | Earnings before interest, taxes, depreciation, and amortization | No | No | How are operations performing before these items? |

| Net income | Profit after recognized expenses | Yes | Not directly | What accounting profit remains for the period? |

| Free cash flow | Cash remaining after operating cash flow is reduced by capital spending | Cash taxes and interest can affect operating cash flow | Yes | How much cash remains after supporting the asset base? |

EBITDA may be informative when comparing operating results. Net income provides a broader accounting measure after interest, taxes, depreciation, and amortization. Free cash flow shifts attention from earnings to cash and recognizes that maintaining or expanding a business can require real investment.

Consider a company that reports healthy EBITDA but needs frequent equipment replacement. EBITDA adds back depreciation and does not deduct capital expenditures, so it may look stronger than the cash economics suggest. Conversely, a company may report modest net income because of substantial depreciation even when current cash generation is steadier. Reading the three measures together helps expose these differences.

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

EBITDA vs. adjusted EBITDA

Standard EBITDA adds back interest, taxes, depreciation, and amortization. Adjusted EBITDA makes further changes, often for items management considers unusual, non-operating, or unrepresentative.

The distinction matters. The SEC’s guidance says measures calculated differently from the described EBITDA formula should use a distinct title, such as “Adjusted EBITDA.”

Non-recurring costs

A company might adjust for a one-time legal settlement, transaction cost, or restructuring charge. The analytical question is whether the expense is truly unusual. If “one-time” restructuring occurs regularly, excluding it each year can make recurring costs disappear from the performance story.

Owner-related and discretionary expenses

For a closely held business, a valuation analysis may normalize an owner’s compensation or remove a personal expense recorded by the company. Any adjustment should reflect the cost a new owner would reasonably expect, not merely maximize the reported result.

Other adjustments may involve gains or losses on asset sales, impairment charges, or share-based compensation. These items differ economically, so analysts should not accept an add-back simply because it appears below an “adjusted” label.

When reviewing adjusted EBITDA, ask:

- What was added back or removed?

- Is the item genuinely outside normal operations?

- Has a similar item appeared in earlier periods?

- Would a buyer or future operator still incur the cost?

- Can the figure be reconciled to net income?

Limitations of EBITDA

EBITDA is useful precisely because it excludes certain items. Those exclusions are also its main weaknesses.

It is not cash flow

EBITDA does not capture all cash entering and leaving a business. Changes in inventory, receivables, payables, capital expenditures, and debt principal can create a large gap between EBITDA and available cash.

It ignores the cost of assets

Depreciation and amortization are non-cash charges in the current period, but the underlying assets may have required cash in the past and may need replacement. This is especially important for asset-intensive businesses.

It removes financing and tax burdens

Interest and taxes may be excluded from EBITDA, but they can still be unavoidable claims on cash. A highly indebted company can show positive EBITDA while facing serious repayment pressure.

Adjustments reduce comparability

Companies may calculate adjusted EBITDA differently. Aggressive or recurring add-backs can overstate the earnings a buyer or investor expects to continue.

A higher figure is not automatically better

EBITDA can rise because the company expanded profitably, but it can also rise while debt, capital needs, or working-capital pressure increase. Direction alone does not explain quality.

An Investor’s EBITDA Review Checklist

Use this checklist when analyzing a public company:

- Confirm the reporting period and currency.

- Recalculate EBITDA from net income.

- Reconcile the result with the company’s presentation.

- Separate standard EBITDA from adjusted EBITDA.

- List every additional adjustment and its rationale.

- Compare several periods, not just one year.

- Check revenue and EBITDA margin trends.

- Review operating cash flow and capital expenditures.

- Examine debt, interest obligations, and taxes.

- Compare only with businesses using similar definitions.

- Read the financial statement notes for context.

The bottom line

EBITDA is net income before interest, taxes, depreciation, and amortization. It can help beginner investors compare operating results and understand valuation discussions, but it does not replace net income, free cash flow, balance-sheet analysis, or an examination of the company’s risks.

After calculating it, review the trend, audit every adjustment, and compare EBITDA with operating cash flow, capital expenditures, debt, and net income. That broader process turns a convenient high-level metric into a more disciplined investment analysis. This Finelo guide is educational rather than personalized financial advice and does not recommend buying or selling a security.

Frequently asked questions

Is EBITDA the same as profit?

No. EBITDA is one earnings measure before specified expenses. Net income is the profit remaining after those expenses and other recognized items.

Can EBITDA be negative?

Yes. Negative EBITDA means the calculation remains below zero even before interest, taxes, depreciation, and amortization. The cause still requires investigation: weak revenue, low gross margin, high operating costs, or temporary disruption can produce very different situations.

What is a good EBITDA?

There is no universal amount or margin. A useful assessment considers the company’s industry, size, business model, history, capital needs, and calculation method. Consistency and cash conversion can matter as much as the reported figure.

InvestingBeginnerFinancial StatementsMarkets

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Investing

Working Capital: What It Tells Investors About Liquidity

Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day…

Finelo Team

Investing

What is Venture Capital?

Venture capital (VC) is money invested in young businesses in exchange for equity, or an ownership stake. It is generally aimed at startups and early-stage companies that need capital to develop a product, hire people…

Finelo Team

Investing

What Is the S&P 500? A Complete Overview

The S&P 500 is a stock market index designed to show how a broad group of leading large-cap U.S. companies is performing. Rather than checking hundreds of stocks individually, investors can look at the index for a…

Finelo Team