Goodwill in accounting is the amount paid to acquire a business above the fair value of its identifiable net assets. A current SEC-filed accounting policy uses the same core definition: goodwill is the excess of the purchase price over the fair value of net assets acquired. For investors, the balance can reveal how much of a company’s reported asset base came from acquisition premiums rather than separately identifiable assets.

Goodwill in Accounting: How Investors Can Read Acquisition Risk

Goodwill in accounting is the amount paid to acquire a business above the fair value of its identifiable net assets. A current SEC-filed accounting policy uses the same core definition: goodwill is the excess of the…

8 min read

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Want to learn more?

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

Goodwill is therefore not the same as cash, equipment, or a separately identifiable brand. It is a residual amount created by the purchase-price calculation. Understanding it helps an investor evaluate acquisition strategy, compare acquisitive companies, and recognize when an impairment may point to weaker-than-expected deal performance.

Introduction to Goodwill

Goodwill exists only after the rest of the acquisition calculation has been assembled. The buyer first identifies the assets acquired and liabilities assumed, measures them as required, and then compares the resulting net amount with the purchase consideration. The unexplained residual is goodwill.

That residual can represent economic benefits that cannot be recognized separately. One SEC-filed acquisition disclosure identifies examples such as future customer relationships, new technology, and an assembled workforce. These examples help explain goodwill, but they are not a checklist that applies identically to every deal.

The key distinction is between business value and accounting goodwill. A company may have a respected name, loyal customers, and capable employees before it is sold. Yet the accounting goodwill figure does not appear merely because those qualities exist. It emerges from the acquisition price allocation.

Why Goodwill Matters to Investors

A business can be worth more to a buyer than the sum of the assets that can be individually identified and valued. A functioning organization may have trained employees, established processes, repeat customers, distribution relationships, and the ability to generate future business. Some acquired items may qualify for separate recognition; the remaining acquisition premium becomes goodwill.

This distinction matters because an acquisition price contains two broad layers:

- The fair value of identifiable assets acquired, less liabilities assumed.

- The residual premium recorded as goodwill.

For financial analysis, a large goodwill balance can show that acquisitions have played a meaningful role in building the company’s asset base. It does not, by itself, prove that management overpaid or that the deal was successful. Investors need to consider the price paid, the identifiable assets obtained, the expected benefits, and whether the acquired operation later performs as anticipated.

Goodwill also affects comparisons between companies. A business that grew mainly through acquisitions may report more goodwill than a similar business that developed its reputation and customer relationships internally. The balance sheets can therefore look different even when the companies compete in the same market.

How Goodwill is Calculated

The basic calculation is:

Goodwill = purchase consideration − fair value of identifiable net assets acquired

Identifiable net assets are the fair value of identifiable assets minus the fair value of liabilities assumed. The calculation uses acquisition-date values rather than simply copying every historical book value from the acquired company’s balance sheet.

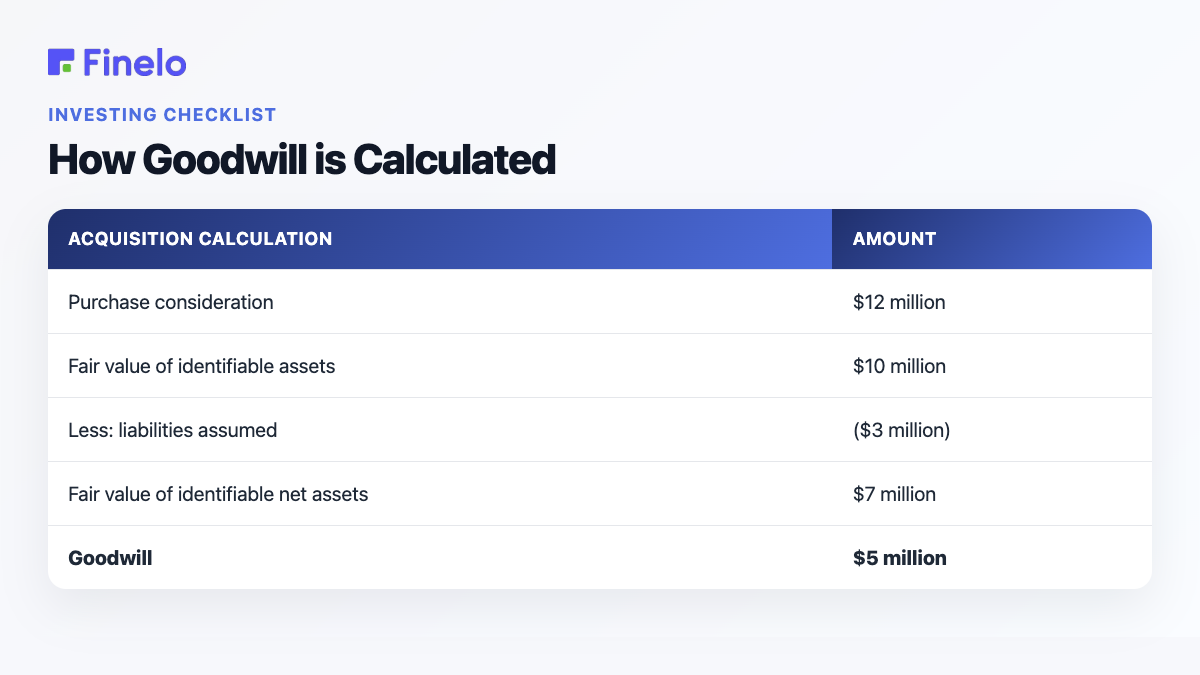

Consider a simplified example. A buyer pays $12 million for a company. At the acquisition date, the identifiable assets have a total fair value of $10 million and the assumed liabilities have a fair value of $3 million.

| Acquisition calculation | Amount |

|---|---|

| Purchase consideration | $12 million |

| Fair value of identifiable assets | $10 million |

| Less: liabilities assumed | ($3 million) |

| Fair value of identifiable net assets | $7 million |

| Goodwill | $5 million |

The buyer records $5 million of goodwill because the $12 million purchase consideration exceeds the $7 million fair value of identifiable net assets.

This example is deliberately simple. Real transactions may involve contingent consideration, noncontrolling interests, previously held stakes, taxes, and detailed valuations of tangible and intangible assets. A change in the valuation of an identifiable asset or liability can also change the residual goodwill amount.

A useful way to interpret the result is to ask what the premium represents economically. The $5 million does not mean the acquired company has a separable “good reputation asset” that could necessarily be sold on its own. It means $5 million of the acquisition price remains after the recognizable net assets have been measured.

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Goodwill on Financial Statements

Goodwill is recorded on the acquiring company’s balance sheet following a qualifying business acquisition. It is associated with the acquired business and should not be treated as a freely adjustable estimate of the buyer’s reputation.

The initial entry can increase total assets substantially. As a result, analysts may review financial measures both with and without goodwill when they want to understand the composition of a company’s asset base. Removing goodwill from an analytical measure does not mean it has no economic relevance; it simply isolates assets that are more readily identifiable.

Goodwill generally does not create a recurring cash inflow on its own. Its economic justification depends on whether the acquired business delivers the benefits that supported the purchase price. That makes post-acquisition performance important. Revenue retention, successful integration, cost control, employee stability, and the realization of expected synergies can all inform whether the original deal assumptions remain reasonable.

Under U.S. public-company accounting, goodwill is not routinely amortized into expense and is instead subject to impairment testing. The SEC has described the applicable treatment as requiring goodwill and indefinite-lived intangibles to be tested at least annually for impairment. A current SEC-filed policy also describes annual assessment plus more frequent review when events or changes suggest the carrying value may not be recoverable. The detailed accounting for a particular company depends on its reporting framework and facts.

GAAP and IFRS: do not assume identical details

Both U.S. GAAP and IFRS address acquired goodwill, but their detailed impairment models, terminology, testing units, and some application requirements can differ. A reader analyzing published accounts should identify which framework the company uses and read its goodwill accounting policy rather than transferring a rule from one framework to the other.

This is especially important when comparing companies across jurisdictions. A difference in reported goodwill or impairment expense may reflect not only business performance but also acquisition history, valuation judgments, and the accounting framework applied.

Goodwill Impairment Testing

Goodwill impairment means the recorded balance is no longer fully supported under the applicable accounting test. In practical terms, the acquired business or the unit containing the goodwill is not supporting the carrying amount previously recorded.

An impairment review connects the goodwill balance to the relevant part of the business. Management then evaluates that unit under the applicable framework. In one current SEC-filed policy, the quantitative test compares the reporting unit’s fair value with its carrying amount, including goodwill. If carrying amount exceeds fair value, the company recognizes an impairment loss, subject to the goodwill allocated to that unit.

Imagine that the buyer in the earlier example records $5 million of goodwill. Two years later, the acquired operation loses major customers and its outlook deteriorates. If the applicable impairment test indicates that $2 million of the goodwill is no longer supported, the company would recognize an impairment charge and reduce goodwill from $5 million to $3 million.

The charge lowers reported profit for the period, but it is not a new payment made at the impairment date. The cash outflow occurred when the acquisition was completed. Impairment is an accounting recognition that the balance sheet can no longer support all of the previously recorded premium.

For investors, an impairment can be informative, but it needs context. It may signal weaker-than-expected acquisition performance, adverse market conditions, or changes in management assumptions. It should be considered alongside cash flow, operating results, debt, integration progress, and management’s explanation of the underlying causes.

Common Misconceptions about Goodwill

“A company can record goodwill whenever its reputation improves.”

Accounting goodwill is tied to an acquisition calculation. A company may build a valuable name, workforce, or customer base internally without recording a corresponding goodwill asset.

“Goodwill equals the value of a brand.”

A qualifying brand or trade name may be identified and valued separately in an acquisition. Goodwill is the residual amount left after identifiable assets and liabilities have been measured.

“More goodwill always means a stronger company.”

A high balance may reflect substantial acquisition activity and large premiums paid. Whether those purchases created value depends on later business performance, not the goodwill number alone.

“An impairment means cash just left the business.”

The impairment charge reduces accounting profit and the carrying value of goodwill. It normally relates back to value assigned in an earlier acquisition rather than representing a same-period acquisition payment.

“Goodwill and a bargain purchase are the same.”

They describe opposite directions in the purchase-price comparison. Goodwill arises when the relevant purchase amount exceeds identifiable net assets. If the calculation runs the other way, specialized accounting analysis is required; it is not positive goodwill.

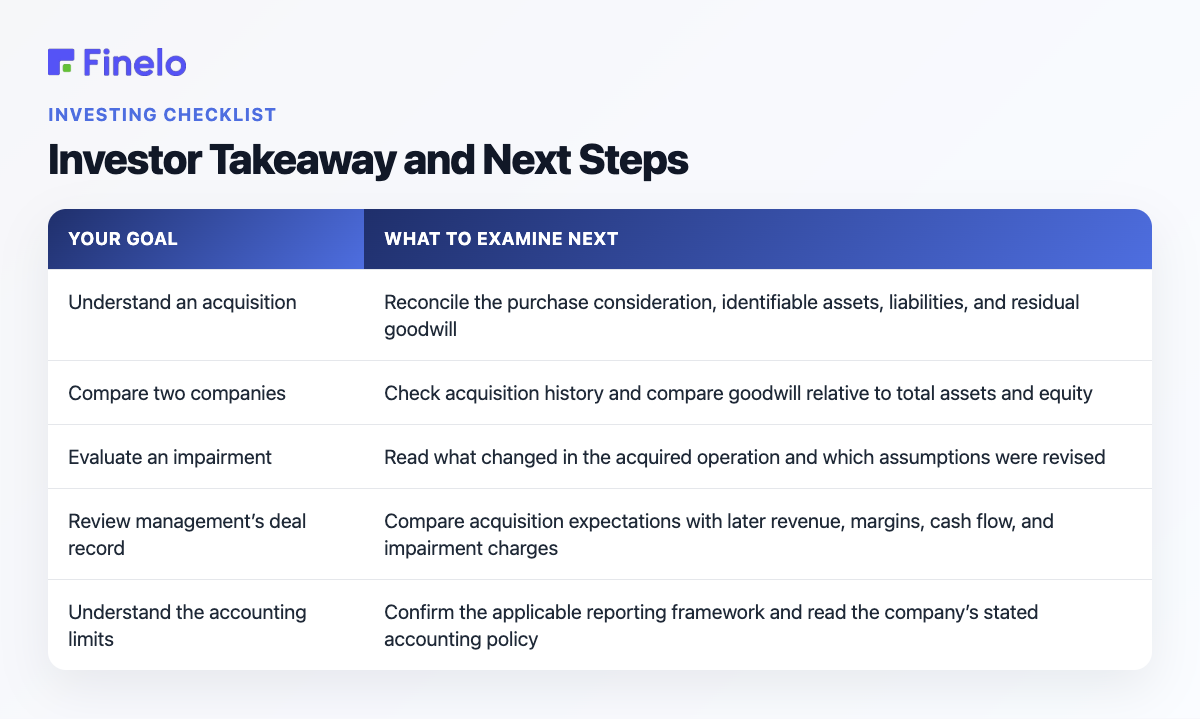

Investor Takeaway and Next Steps

The best next step depends on the investment question you are trying to answer:

| Your goal | What to examine next |

|---|---|

| Understand an acquisition | Reconcile the purchase consideration, identifiable assets, liabilities, and residual goodwill |

| Compare two companies | Check acquisition history and compare goodwill relative to total assets and equity |

| Evaluate an impairment | Read what changed in the acquired operation and which assumptions were revised |

| Review management’s deal record | Compare acquisition expectations with later revenue, margins, cash flow, and impairment charges |

| Understand the accounting limits | Confirm the applicable reporting framework and read the company’s stated accounting policy |

Start with the acquisition note and the company’s accounting-policy disclosure. Then trace changes in the goodwill balance from one reporting period to the next. Look for new acquisitions, disposals, currency effects, reclassifications, and impairment charges. This turns goodwill from an isolated balance-sheet number into a clearer story about management’s capital-allocation decisions.

When judging management’s acquisition record, focus on the commercial assumptions behind the premium rather than treating a larger goodwill balance as a sign of strength. Customer retention, integration costs, operating margins, workforce stability, cash flow, and the delivery of expected benefits provide more useful evidence. The accounting balance follows the transaction and applicable standards; it is not an investment score.

The clearest answer to “what is goodwill in accounting?” is: the residual acquisition premium left after subtracting the fair value of identifiable net assets from the purchase amount. It matters because it connects an acquisition price to the balance sheet and creates an ongoing need to assess whether the acquired business supports the recorded value.

After reading, locate a public company’s acquisition note, reproduce the calculation, and review later impairment disclosures. That sequence—price, net assets, residual, subsequent performance—offers a disciplined investor workflow for interpreting goodwill. This Finelo guide is educational and does not recommend buying or selling any security.

Frequently asked questions

Can goodwill be negative?

The standard goodwill formula can produce a negative preliminary result when the relevant purchase amount is below the fair value of identifiable net assets. That result is not recorded as negative goodwill without further analysis. The measurements and transaction terms need to be reassessed, followed by the treatment required under the applicable accounting framework.

Can goodwill be sold?

Goodwill is generally connected to a business or business unit rather than functioning as a separable asset that can be sold independently. Its treatment in a disposal depends on what operation is sold and how the related goodwill was assigned.

Does goodwill affect cash flow?

Recording goodwill at acquisition is part of accounting for the purchase, while a later impairment charge is generally non-cash at the time it is recognized. However, the original acquisition involved consideration, and the acquired business’s later operating cash flows are central to evaluating whether the purchase delivered its expected benefits.

Who should pay attention to goodwill?

Investors can use it to understand acquisition exposure and impairment risk. Business owners may encounter it when buying or selling a company. Accounting students and financial-statement readers use it to connect purchase-price allocation, intangible value, and post-acquisition performance.

InvestingBeginnerFinancial StatementsMarkets

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Investing

Working Capital: What It Tells Investors About Liquidity

Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day…

Finelo Team

Investing

What is Venture Capital?

Venture capital (VC) is money invested in young businesses in exchange for equity, or an ownership stake. It is generally aimed at startups and early-stage companies that need capital to develop a product, hire people…

Finelo Team

Investing

What Is the S&P 500? A Complete Overview

The S&P 500 is a stock market index designed to show how a broad group of leading large-cap U.S. companies is performing. Rather than checking hundreds of stocks individually, investors can look at the index for a…

Finelo Team