Retained earnings are the cumulative profits a company has kept in the business instead of distributing them to shareholders. They rise when the company keeps new profit. They fall when the company records losses or makes distributions. For investors, the figure provides a record of accumulated profitability and opens a more important question: has management used retained capital productively? It is not the same thing as cash in the bank.

Retained Earnings: What They Tell Investors About Capital Allocation

Retained earnings are the cumulative profits a company has kept in the business instead of distributing them to shareholders. They rise when the company keeps new profit. They fall when the company records losses or…

7 min read

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Want to learn more?

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Explore FineloExplore Finelo's 28-day challenges

Turn learning into a daily habit with guided challenge paths.

This guide shows beginner investors where to find retained earnings, how to reconcile the balance, and how to connect it with dividends, cash flow, debt, and management’s capital-allocation decisions. A positive balance is not automatically good, and a negative balance is not a complete investment diagnosis.

Introduction to retained earnings

Retained earnings appear as a distinct account within stockholders’ equity. SEC filing guidance describes retained earnings separately when discussing changes in the accounts that make up stockholders’ equity.

Think of retained earnings as a running record. Each reporting period begins with the previous ending balance. The company then adds profit or subtracts a loss. It also subtracts dividends or other relevant distributions.

An important distinction is whether earnings are available for general use or have been set aside for a specific purpose. The Internal Revenue Service describes appropriated retained earnings as earnings reserved for specific purposes and not available for shareholder distribution. It describes unappropriated retained earnings as earnings and profits less those reserves, with shareholder dividends and distributions paid from that account.

That distinction explains why retained earnings do not represent idle money. Management may keep profits and use the resources for inventory, equipment, debt reduction, hiring, or other business needs.

Where to find retained earnings

Start with the balance sheet and statement of stockholders’ equity. For a public U.S. company, you can get these documents from its Form 10-K or Form 10-Q. Investor.gov explains that audited financial statements include the income statement, balance sheets, cash-flow statement, and statement of stockholders’ equity.

Use the balance sheet to find the ending retained earnings balance. Then use the statement of stockholders’ equity to trace what changed. Go back to the income statement for net income and review the dividend information.

How to calculate retained earnings

When calculating retained earnings, use this standard roll-forward:

Ending retained earnings = Beginning retained earnings + Net income − Dividends

If the company reports a net loss, subtract the loss instead of adding net income. Other accounting adjustments may appear in a formal statement, but this formula captures the main movement.

Retained earnings formula infographic

Beginning balance → add net income (or subtract net loss) → subtract dividends → ending balance

Simple calculation example

Suppose a fictional company starts the year with $80,000 in retained earnings. During the year, it records $30,000 of net income and declares $10,000 in dividends:

$80,000 + $30,000 − $10,000 = $100,000

Its ending retained earnings are $100,000. That ending amount normally becomes the next period’s beginning balance.

Now consider a loss. If the same company began with $80,000, recorded a $25,000 net loss, and paid no dividends, its ending balance would be:

$80,000 − $25,000 = $55,000

The company would still have positive retained earnings, but the accumulated balance would have declined.

Retained earnings calculation checklist

Before you accept the result, make these checks:

- Use the beginning balance from the immediately preceding period.

- Use net income or net loss for the same reporting period.

- Subtract dividends declared for that period.

- Keep the reporting units consistent.

- Investigate any adjustment that prevents the numbers from reconciling.

What Retained Earnings Tell Investors

Retained earnings show how profits and shareholder distributions have accumulated across the company’s history. That makes the account useful for several related questions.

First, the balance shows whether cumulative profits have exceeded losses and distributions. A growing balance may show that profitable periods are adding to equity. A falling balance can result from losses, dividends, or both.

Second, retained earnings can support reinvestment. A company may choose to keep part of its profits when management believes the business has productive uses for them. However, retaining more is not automatically better. The important question is whether management uses the resources sensibly.

Third, the balance adds context to dividend decisions. Distributions reduce retained earnings. A company therefore balances current shareholder payments against future business needs. The appropriate choice differs by company, stage of development, and financial position.

Retained earnings should therefore be read alongside net income, cash flow, debt, assets, liabilities, and the company’s explanation of capital allocation. No single account gives a complete picture of financial health.

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

Retained earnings across different business contexts

Comparing raw retained earnings across unrelated companies can be misleading. A large, established company and a young company may have very different operating histories, capital needs, and distribution policies.

Retained earnings by industry and business model

The following table is a reading framework, not a claim that every company in an industry behaves the same way:

| Business context | Why profits might be retained | What to examine next |

|---|---|---|

| Young growth business | Hiring, product development, or expansion | Cash use, losses, funding needs, and evidence of progress |

| Capital-intensive business | Equipment, facilities, or maintenance | Debt, capital spending, asset productivity, and cash flow |

| Mature dividend-paying business | Financial flexibility and selected reinvestment | Dividend history, payout decisions, and reinvestment returns |

| Seasonal business | Working-capital needs during quieter periods | Cash cycle, inventory, short-term borrowing, and liquidity |

Rather than asking which company has the biggest balance, ask whether the balance is understandable relative to the company’s age, profitability, distribution policy, and use of capital.

Real-world examples of retained earnings in action

Investor Example: Reinvesting Retained Earnings for Growth

Consider a realistic but hypothetical reinvestment case. A profitable manufacturer retains part of its annual earnings instead of distributing all available profit. Management replaces an aging production line. In later periods, an analyst should not judge the decision only by noting that retained earnings increased and the company bought equipment.

The analyst would examine whether production, costs, cash flow, and debt changed as expected. If the equipment fails to produce useful results, retaining the profit did not automatically create value. If the investment strengthens operations without putting liquidity under pressure, the decision may look more reasonable.

This example highlights the central point. Retained earnings record accumulated profit kept in the company. They do not prove that management used the resources well.

Retained earnings management checklist

Business owners can copy this checklist into their period-end review:

- Reconcile the beginning balance with the prior period.

- Add net income or subtract the net loss.

- Subtract dividends and relevant distributions.

- Record and explain any other adjustments.

- Compare the ending balance with available cash.

- Review debt, liquidity, and planned uses of capital.

- Document why profits were retained or distributed.

Common misconceptions about retained earnings

“Retained earnings are cash.”

They are an equity account, not a bank balance. Cash may already have been spent on assets, operating needs, or debt payments.

“Positive retained earnings prove that a company is financially healthy.”

A positive balance provides useful historical context, but it cannot establish overall health by itself. A company can have accumulated profits and still face weak cash flow or heavy debt.

“Negative retained earnings mean bankruptcy.”

A negative balance, sometimes called an accumulated deficit, means cumulative losses and distributions have exceeded cumulative profits under the account’s calculation. It is a warning sign to investigate, not a complete diagnosis.

“Paying dividends is always worse than retaining profits.”

Neither choice is automatically superior. Retaining profits may help fund worthwhile needs, while distributions may be reasonable when the business lacks attractive uses for additional capital. The decision should be judged in context.

Investor Takeaway and Next Steps

To analyze retained earnings, start with the current and prior balance sheets. Connect the change to net income and dividends. If the figures do not match, check the statement of stockholders’ equity for adjustments. Once the numbers reconcile, examine cash flow, debt, returns on reinvested capital, and management’s use of capital. Do not treat retained earnings as a standalone score or assume that retaining more profit always creates shareholder value.

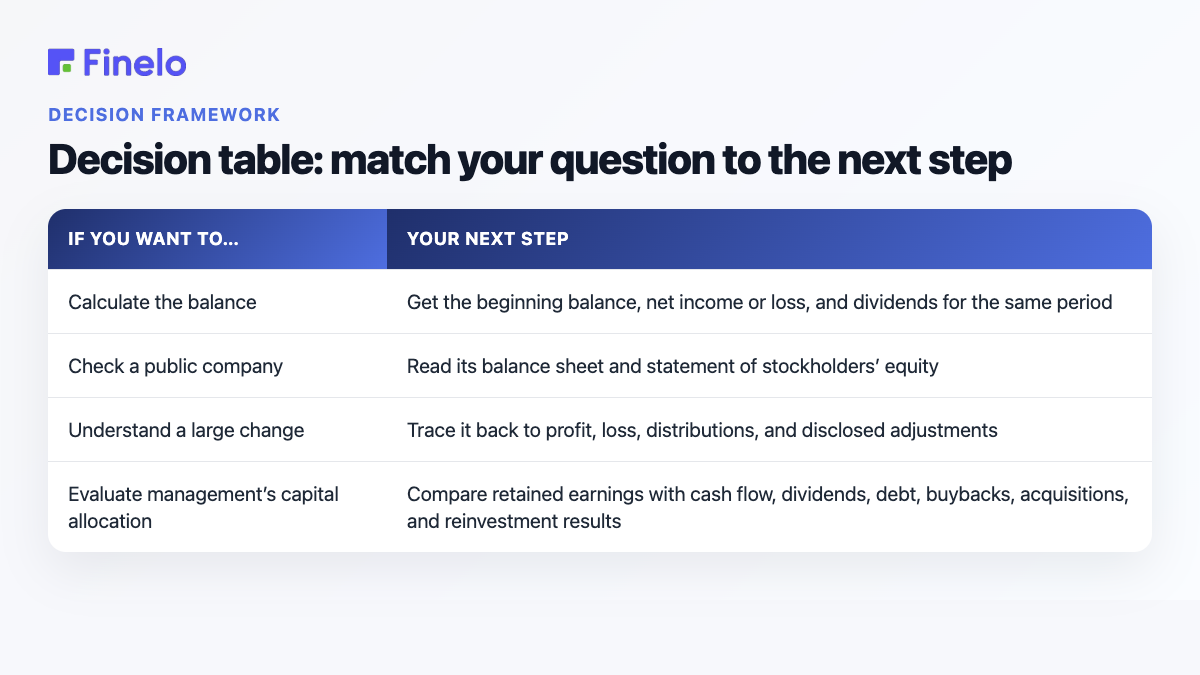

Decision table: match your question to the next step

| If you want to… | Your next step |

|---|---|

| Calculate the balance | Get the beginning balance, net income or loss, and dividends for the same period |

| Check a public company | Read its balance sheet and statement of stockholders’ equity |

| Understand a large change | Trace it back to profit, loss, distributions, and disclosed adjustments |

| Evaluate management’s capital allocation | Compare retained earnings with cash flow, dividends, debt, buybacks, acquisitions, and reinvestment results |

If you’re a beginner building investment literacy, Finelo offers a starting point for learning how financial statements connect to investment questions. Its role here is education: the linked official filings remain the evidence for company-specific facts. Verify current financial statements and remember that this guide does not recommend buying or selling any security.

Frequently asked questions

Can retained earnings be used to pay debt?

A company may use its financial resources to reduce debt, and doing so may be part of its capital-allocation plan. But retained earnings are not a separate pool of cash that can simply be withdrawn. Check the cash position and cash-flow statement to see whether repayment is practical.

What is the difference between retained earnings and revenue?

Revenue is generated during a particular period before expenses are fully deducted. Retained earnings are cumulative and reflect profits kept after losses and shareholder distributions have affected the account.

How do retained earnings affect valuation?

They can provide context about accumulated profitability and distribution decisions, but valuation depends on much more than this one balance. Investors may also consider expected cash flows, risks, debt, assets, growth prospects, and how effectively management allocates capital.

How often should retained earnings be reviewed?

Review the account whenever financial statements are prepared and compare it with the prior period. If it changes unexpectedly, reconcile beginning retained earnings, profit or loss, dividends, and any disclosed adjustments.

InvestingBeginnerFinancial StatementsMarkets

Practice investing with Finelo

Build practical investing skills with guided lessons, simulator practice, and structured challenges.

About the author

Finelo Team

The Finelo Team creates practical investing and trading education designed to help beginners learn faster with structured challenges, simulator practice, and bite-sized lessons.

Keep reading — Related articles

Investing

Working Capital: What It Tells Investors About Liquidity

Working capital is the amount left after subtracting a business’s current liabilities from its current assets. For investors, it is a starting point for examining short-term liquidity and the cash tied up in day-to-day…

Finelo Team

Investing

What is Venture Capital?

Venture capital (VC) is money invested in young businesses in exchange for equity, or an ownership stake. It is generally aimed at startups and early-stage companies that need capital to develop a product, hire people…

Finelo Team

Investing

What Is the S&P 500? A Complete Overview

The S&P 500 is a stock market index designed to show how a broad group of leading large-cap U.S. companies is performing. Rather than checking hundreds of stocks individually, investors can look at the index for a…

Finelo Team